.svg)

Yes, you can roll over your Thrift Savings Plan (TSP) to a Gold IRA. The process involves opening a Self-Directed IRA with an approved custodian, initiating a direct rollover from the TSP to avoid tax penalties, and then using those funds to purchase IRS-approved physical precious metals for storage in a secure depository.

Who this guide is designed for

This guide is designed for federal employees and members of the uniformed services with accumulated TSP balances who are evaluating partial rollovers to precious metals IRAs as part of a long-term retirement planning strategy. It focuses on understanding rollover mechanics, custody requirements, and fee trade-offs—not market timing or return predictions.

The Critical Decision Facing Federal Employees

For decades, you have diligently contributed to your Thrift Savings Plan, trusting in a system designed for stability and simplicity. It has served you well. But the financial landscape is shifting beneath our feet. Persistent inflation concerns, market volatility, and broader economic uncertainty now compel prudent federal employees and members of the uniformed services to ask a critical question: Is my retirement savings truly protected?

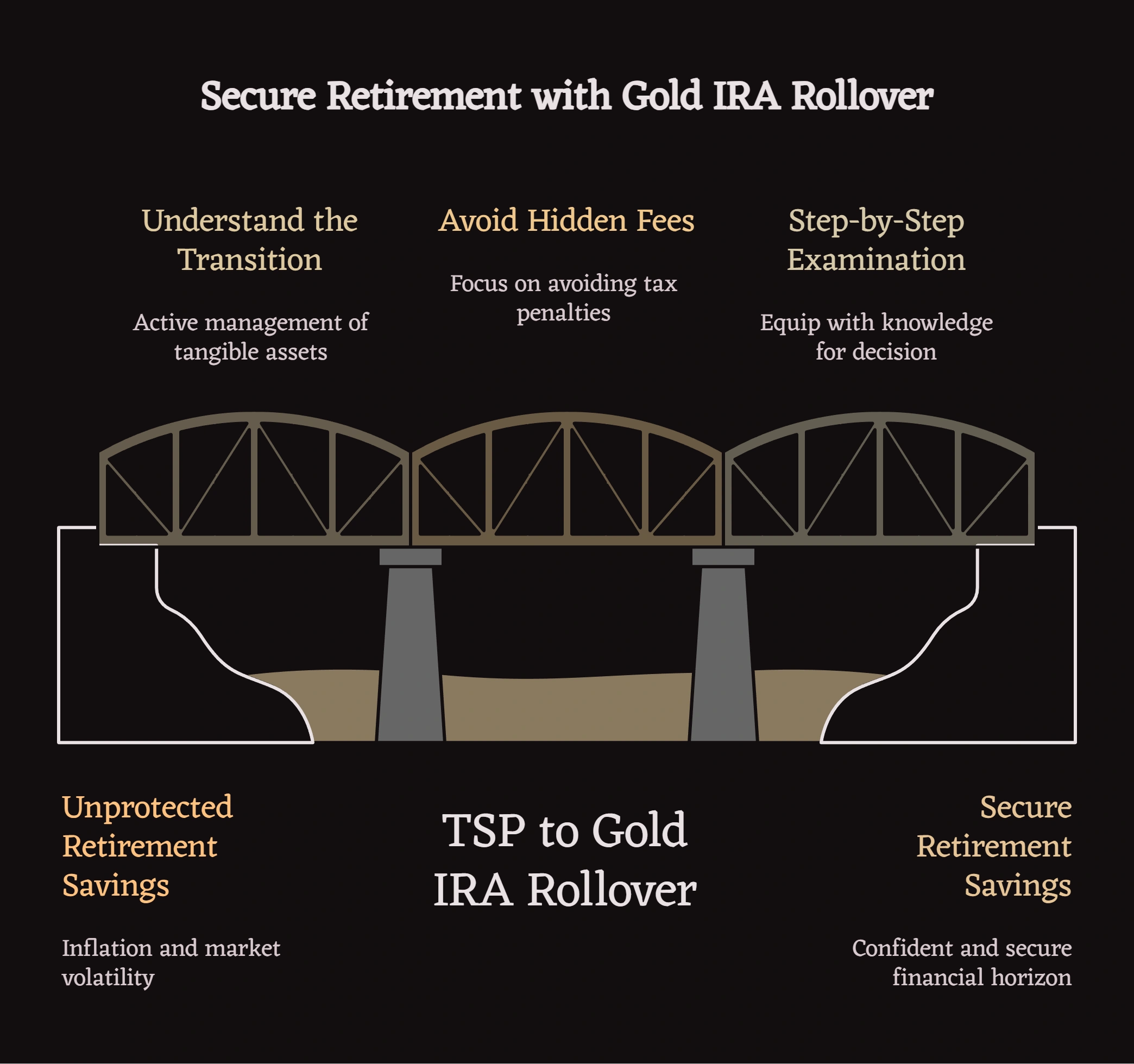

This has led many to consider a powerful diversification strategy: rolling over a portion of their TSP into a Gold IRA. This isn’t merely a change of investment; it is a fundamental shift in your retirement planning philosophy—from a passive participant in government-managed funds to an active manager of tangible assets. However, this path is fraught with potential pitfalls that glossy advertisements conveniently omit. The core thesis you must grasp is this: a successful TSP to Gold IRA rollover isn’t about the transactional steps, but about navigating the critical transition from a low-cost, government-backed system to a high-responsibility, specialist investment, focusing on avoiding the hidden fees and tax penalties that can decimate your hard-earned money.

This guide provides a sober, step-by-step examination of the process, designed to equip you with the knowledge to make a confident and secure decision for your financial horizon.

The Direct Rollover Imperative: Your First Line of Defense Against Tax Penalties

Before you even think about gold coins or storage vaults, you must understand the single most critical step in this entire process: how you move your money. There are two ways to execute rollovers, but only one is acceptable for a TSP account holder seeking to avoid immediate and severe financial consequences.

The Dangers of an Indirect Rollover

An indirect rollover is where you request a check from your TSP, made out to you personally. You then have 60 days to deposit that money into your new Gold IRA. This method is a trap for the unwary. When you take a distribution from a plan like a 401(k) or TSP, the administrator is often required to withhold a significant portion for taxes. Specifically, during an indirect rollover from a Roth TSP, if the distribution is ‘non-qualified,’ the TSP will withhold 20% of the earnings portion for federal income taxes according to industry analysis. To complete the full rollover, you would have to make up that 20% out of your own pocket and then wait to reclaim the withheld amount when you file your taxes.

Furthermore, the clock is ticking. The Internal Revenue Service (IRS) is strict: the funds must be deposited into the new account within 60 days. If you miss that deadline for any reason, the entire distribution is considered a taxable withdrawal. For those under age 59 ½, this could mean not only income tax on the full amount but also a crushing 10% early withdrawal penalty as outlined in rollover guidelines.

The Safe Harbor: A Direct Rollover (Trustee-to-Trustee Transfer)

The only prudent method is a Direct Rollover, also known as a trustee-to-trustee transfer. In this scenario, you instruct the Federal Retirement Thrift Investment Board (FRTIB), the body that administers the TSP, to send your funds directly to the custodian of your new Self-Directed IRA. The money never touches your personal bank account. This simple distinction allows you to bypass the 20% mandatory withholding and eliminates the risk of missing the 60-day deadline. It is a clean, secure transfer of assets that preserves the tax-deferred or tax-free status of your retirement account.

For a comprehensive evaluation of whether a TSP rollover aligns with your specific situation, including pros, cons, and common TSP rollover mistakes, federal employees should understand the broader strategic considerations beyond the mechanics of the transfer itself.

A Sober Cost-Benefit Analysis: Calculating the True Price of the Transition

Leaving the TSP ecosystem means leaving behind its greatest advantages: simplicity and incredibly low costs. A Gold IRA offers tangible portfolio protection but comes with a more complex and expensive fee structure. A clear-eyed comparison is essential.

Thrift Savings Plan (TSP)

- Pros: The TSP boasts some of the lowest expense ratios in the entire retirement industry. It offers a straightforward set of investment options, including the C, S, and I Funds, which track broad market indexes. Its most unique feature is the G Fund, which invests in non-marketable government securities, offering principal protection and a guaranteed rate of return. It is a passive, “set it and forget it” system.

- Cons: The investment options are extremely limited. You cannot invest in alternative assets like real estate or physical precious metals. Your portfolio is entirely composed of paper assets, leaving you exposed to systematic market risk and the erosive effects of inflation on currency.

Gold IRA

- Pros: A Gold IRA allows you to hold physical gold, silver, platinum, or palladium as a tangible asset within your retirement account. This provides a historically discussed hedge against inflation and currency debasement. It offers diversification away from stocks and bonds, potentially providing stability during periods of market volatility and economic uncertainty. You have direct control over a real, physical asset.

- Cons: This control comes at a price. Gold IRAs involve multiple layers of fees that TSP participants are unaccustomed to. These typically include a one-time setup fee, annual administrative fees paid to the IRA custodian (such as Equity Trust, among others), and annual storage fees paid to the IRS-approved depository (such as the Delaware Depository). Furthermore, there are transaction costs and dealer markups when you buy and sell the metals. For smaller balances, these fixed annual costs can represent a materially higher percentage drag compared to the TSP’s expense ratios.

The Rollover Process

- Pros: A properly executed direct rollover is a tax-free event that allows you to move your retirement savings from one qualified account to another without penalty. It unlocks the ability to significantly diversify your retirement portfolio into assets not available in the TSP.

- Cons: An improperly executed indirect rollover can trigger immediate and substantial tax liabilities and penalties. The process requires careful selection of a reputable custodian, precious metals dealer, and depository, placing a significant due diligence burden on you, the account holder. A wrong choice can lead to excessive fees or poor service.

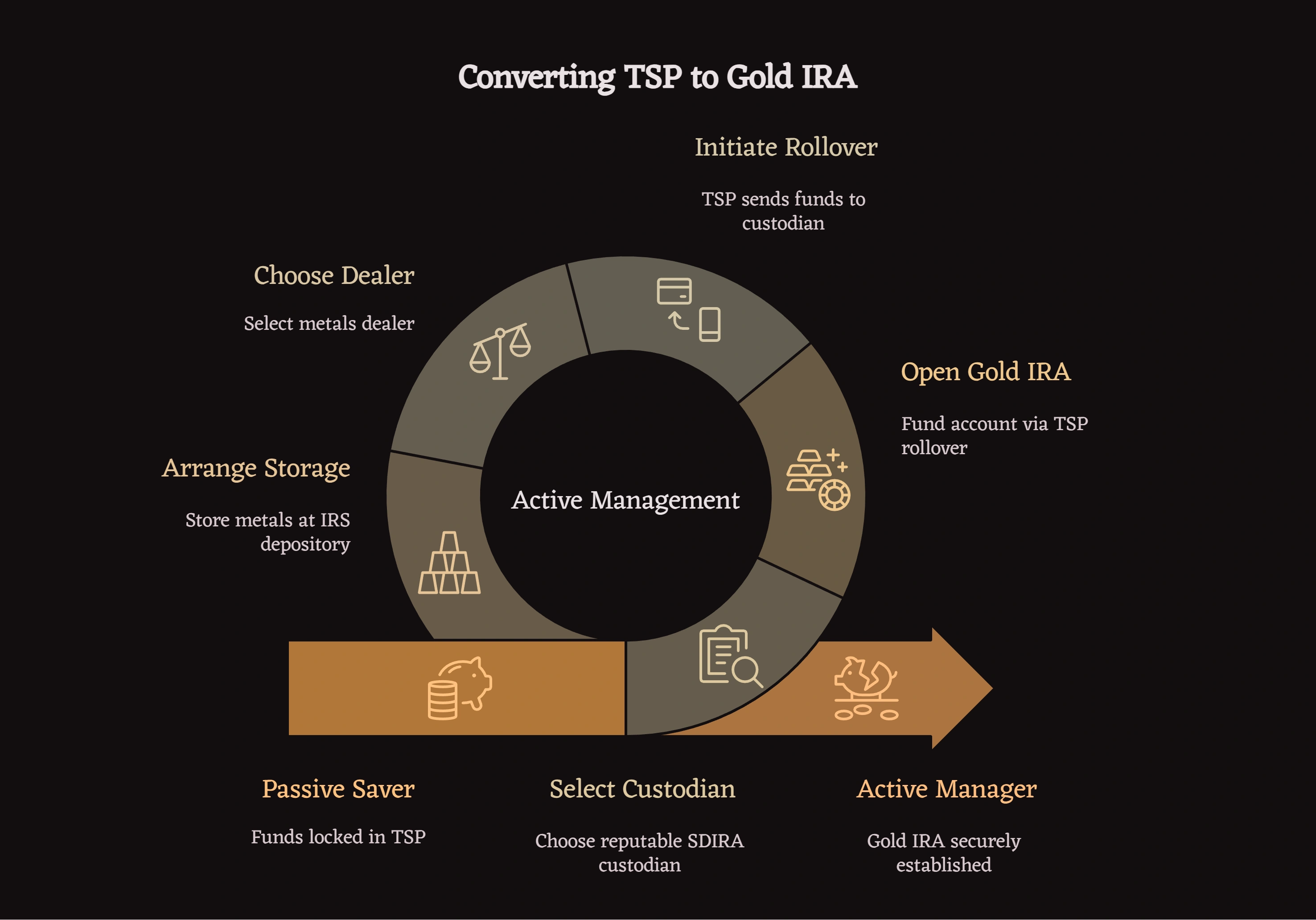

Your Step-by-Step Guide: From Passive Saver to Active Manager

Once you have weighed the costs and benefits and decided to proceed, the process follows a clear sequence. Remember, each step requires your active involvement and careful consideration. So, how to change TSP to gold? You must follow these five critical steps.

Step 1: Select a Reputable Self-Directed IRA Custodian

Your first and most important choice is your Self-Directed IRA (SDIRA) custodian. A standard IRA provider cannot hold physical precious metals. You need a specialist firm that is approved by the IRS to manage these tangible assets. The custodian is responsible for administering your account, executing transactions on your behalf, and handling all IRS reporting. Conduct thorough research on companies (such as Horizon Trust, for illustration) specializing in precious metals. Look for transparent fee structures, a long track record, and positive client reviews.

Step 2: Open and Fund Your New Gold IRA Account

After selecting a custodian, you will complete their account application. This is similar to opening any other financial account. The key part of this step is funding the account via your TSP rollover. You will provide the custodian with your TSP account information and sign the necessary forms authorizing the transfer. At this stage, you must be absolutely clear that you are requesting a Direct Rollover.

Step 3: Initiate the TSP Withdrawal and Direct Rollover

With your new IRA account open, you or your new custodian will contact the TSP to initiate the withdrawal. The TSP will process the request and send the funds directly to your new SDIRA custodian. This trustee-to-trustee transfer can take several weeks, so patience is required. You can monitor the status of the transfer through your TSP account portal.

Step 4: Choose Your Precious Metals Dealer and Select Your Bullion

Once the funds arrive in your new IRA, you are ready to purchase your precious metals. Your custodian can provide a list of dealers they have worked with (such as Augusta Precious Metals or Goldco, among others), but the final choice is yours. The IRS has strict purity standards for the metals held in a retirement account. For example, gold bullion and coins must be at least .995 fine. Popular IRS-approved options include the American Gold Eagle and the Canadian Gold Maple Leaf coins. You will work with the dealer to select your metals and direct your IRA custodian to purchase them using the funds in your account.

Step 5: Arrange for Storage at an IRS-Approved Depository

The final step is securing your assets. The physical gold, silver, or platinum you purchase cannot be stored in your home or a personal safe deposit box. The law requires it to be held by a third-party, IRS-approved depository. These are high-security facilities like Brinks Global Services that specialize in safeguarding precious metals. The dealer will typically coordinate the shipment of your metals directly from their inventory to your chosen depository, where they will be held in your name under your IRA account.

Beyond the Rollover: Avoiding Prohibited Transactions

Your responsibility does not end once the gold is in the vault. As the manager of a Self-Directed IRA, you must adhere to a strict set of IRS rules regarding prohibited transactions. A violation can have catastrophic consequences, potentially causing the IRS to deem your entire IRA distributed, triggering full taxation and penalties.

The most common and dangerous prohibited transaction for Gold IRA owners is taking personal possession of the metals. You cannot have the gold shipped to your home. You cannot borrow against it. The metals must remain with the depository until you take a legitimate distribution, typically in retirement. A rollover is a reportable transaction, and there is a time limit of 60 days to complete a rollover contribution as stipulated by the IRS. Attempting to circumvent these rules is a direct path to financial disaster. Likewise, a distribution from an IRA may be subject to a 10% additional tax if you are under age 59 1/2 unless you qualify for an exception.

Frequently Asked Questions

Is a TSP to gold IRA rollover taxable?

A properly executed direct rollover (trustee-to-trustee transfer) is not a taxable event. The funds move directly from your TSP to your new Self-Directed IRA custodian without triggering taxes or penalties. However, an indirect rollover—where you receive the funds personally—triggers mandatory 20% withholding and creates a 60-day deadline to complete the transfer, or the entire distribution becomes taxable.

Can I roll over part of my TSP instead of the full balance?

Yes. Federal employees can execute partial TSP rollovers, allowing you to diversify a portion of your retirement savings into precious metals while maintaining the majority of your balance in the low-cost TSP system. This strategy is common among those seeking diversification without abandoning the TSP’s expense advantages entirely.

What happens if I miss the 60-day rollover window?

If you miss the 60-day deadline in an indirect rollover, the IRS treats the entire distribution as a taxable withdrawal. This means you’ll owe income tax on the full amount, and if you’re under age 59½, you’ll also face a 10% early withdrawal penalty. This is why direct rollovers are strongly recommended—they eliminate this risk entirely.

Why does a gold IRA cost more than a TSP?

The TSP’s ultra-low fees are possible because it’s a government-administered program offering limited investment options with massive economies of scale. A Gold IRA requires specialized custodial services, IRS-approved depository storage, insurance, and dealer transaction costs for physical precious metals. These are fixed costs that apply regardless of account size, which is why gold IRAs are typically more suitable for larger balances where the percentage impact of these fees is smaller.

Making the Right Choice for Your Needs

So, what is the best thing to do with your TSP when you retire or as you plan for it? The answer is not universal. The decision to execute a TSP to Gold IRA rollover depends entirely on your personal financial situation, risk tolerance, and retirement goals.

For The Cautious Federal Retiree

You have a substantial TSP balance and your primary concern is wealth preservation. For you, the complexity and fees of a Gold IRA must be carefully weighed. Consider allocating only a smaller portion of your TSP to a precious metals IRA. Your priority must be executing a flawless Direct Rollover to avoid any tax surprises. Scrutinize every line item of the fee schedule from potential custodians and dealers before committing. Your goal is stability, not speculation.

For The High-Net-Worth Federal Employee

You are looking to diversify a large portfolio away from an over-concentration in paper assets. You understand that a Gold IRA is not for generating income but for providing an anchor of stability against economic storms. Your focus should be on deep due diligence into the long-term viability and security of your chosen custodian and depository. The higher fees are a known cost of securing tangible assets, but you must compare multiple providers to ensure you are not overpaying for the service.

For The Skeptical Mid-Career Employee

You are concerned about long-term market trends but are rightly sensitive to the high-responsibility nature of a Gold IRA. Before leaving the ultra-low-cost TSP structure, calculate the potential long-term drag of annual storage and administrative fees on your portfolio’s growth. A Gold IRA is an active, not passive, investment. You must be prepared to take on the role of an active manager. For many in this position, the best first step might be to educate yourself thoroughly and wait until you are closer to retirement before making such a significant move.

For federal employees and military investors considering specific provider options, understanding the step-by-step Noble Gold TSP rollover process can provide additional clarity on how custodian selection and onboarding procedures differ across companies.

Final Considerations

For federal employees, the decision to roll over a portion of a TSP into a gold IRA is less about predicting markets and more about understanding structure, costs, and long-term responsibilities. A clear understanding of rollover mechanics, custody rules, and fee trade-offs is essential before making any allocation decision.

Ultimately, moving funds from the familiar territory of the Thrift Savings Plan to a Gold IRA is a significant strategic maneuver. It requires a clear understanding of the process, a sober assessment of the costs, and a commitment to active oversight. This is not a decision to be taken lightly or based on a fear-driven sales pitch. It is a calculated choice for those seeking to secure their wealth with the timeless value of physical precious metals.