.svg)

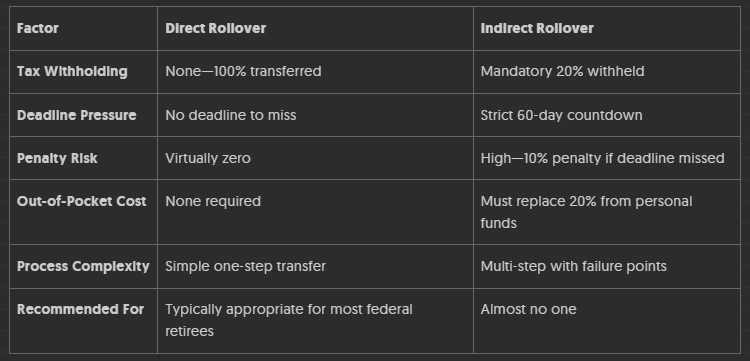

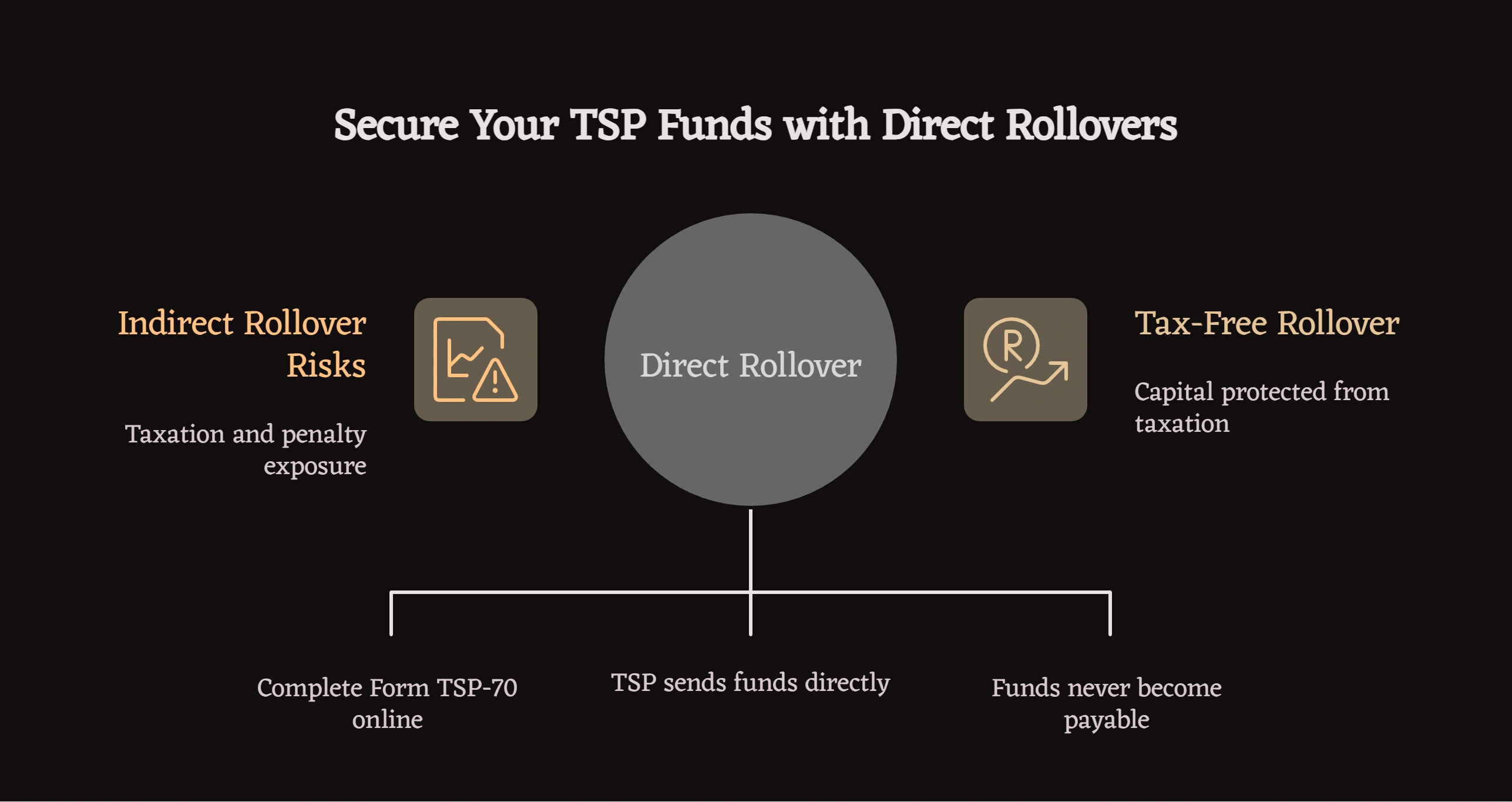

A direct TSP rollover moves your funds trustee-to-trustee with zero tax withholding and no deadlines. An indirect rollover puts a check in your hands, triggering mandatory 20% tax withholding and a strict 60-day deadline that permanently reduces retirement capital through taxes and penalties if missed. For federal employees and military service members protecting decades of contributions, the direct rollover eliminates every major risk.

Last updated: January 2026

Key Takeaways

- Direct rollovers avoid the 20% mandatory tax withholding that makes indirect rollovers financially dangerous

- The 60-day deadline for indirect rollovers creates catastrophic penalties if missed for any reason

- Trustee-to-trustee transfers preserve 100% of your capital without exposure to taxes or penalties

- Federal employees under CSRS and military members under BRS face identical rollover rules and risks

Direct vs Indirect TSP Rollover Comparison

Choosing between rollover methods isn't just a paperwork decision—it affects taxes, penalties, and long-term capital preservation. Federal employees often evaluate rollover mechanics before deciding whether alternative assets, including precious metals IRAs, fit within their retirement strategy.

For a comprehensive decision framework—including benefits, trade-offs, and common mistakes federal employees make—see our in-depth guide on whether federal employees should roll over a TSP into a gold IRA.

Understanding Your TSP Rollover Options

After years of federal service—whether under the Civil Service Retirement System or as a military service member under the Blended Retirement System—your Thrift Savings Plan represents more than account balances. These funds reflect decades of disciplined contributions and matching dollars earned through public service.

The mechanics of moving these assets matter enormously. Two distinct processes exist: direct rollovers and indirect rollovers. While both technically accomplish fund transfers, only one protects your capital from immediate taxation and penalty exposure.

How Do Direct Rollovers Protect Your TSP Capital?

In a direct rollover (also called a trustee-to-trustee transfer), your TSP funds move from the Federal Retirement Thrift Investment Board directly to your new IRA custodian. You never receive a check. The money transfers between institutions without triggering tax consequences.

Federal employees complete Form TSP-70 (Request for Full Withdrawal) or initiate the process through the TSP website. The FRTIB sends funds from your G Fund, F Fund, C Fund, S Fund, and I Fund allocations straight to firms like Fidelity, Charles Schwab, Vanguard, or specialized precious metals IRA custodians.

Because distributions never become payable to you personally, the transfer avoids the two catastrophic problems that plague indirect rollovers: mandatory tax withholding and deadline pressure.

How Indirect Rollovers Create Financial Risk

An indirect rollover follows a different path. The TSP sends you a check directly. You deposit those funds into your personal checking account, then have 60 days to move them into a qualified retirement account.

According to the Code of Federal Regulations, an indirect rollover occurs when a participant receives a distribution from a plan and subsequently requests to roll it over into another account [1]. This seemingly simple process contains multiple failure points that can devastate retirement savings.

The moment you request an indirect rollover from a traditional TSP account, federal law requires 20% mandatory income tax withholding [2]. For a $200,000 distribution, you receive $160,000. The FRTIB sends the remaining $40,000 directly to the IRS as withholding.

This creates an immediate problem: completing a tax-free rollover requires depositing the entire $200,000 into your new IRA within 60 days. You only received $160,000. The missing $40,000 must come from your personal savings, liquidated assets, or borrowed funds.

Veterans transitioning from military service and federal employees entering retirement often lack $40,000 in readily available cash. Failing to replace this withheld amount means permanent taxation of those funds plus potential early withdrawal penalties.

The 60-Day Rollover Deadline Problem

The 60-day requirement for indirect rollovers creates what financial planners call rollover risk. From the date you receive TSP funds, you have exactly 60 days to complete the deposit into another qualified retirement account [3].

Life interferes with financial timelines. Medical emergencies, family crises, administrative delays at receiving institutions, lost documentation, or simple confusion about requirements can cause missed deadlines. The consequences extend far beyond inconvenience.

Missing the 60-day window converts your entire distribution into taxable income. The IRS treats undeposited funds as ordinary income, potentially pushing you into higher tax brackets. Federal income tax applies to the full amount. State income tax follows in most jurisdictions.

For federal employees under age 59½, the IRS imposes an additional 10% early withdrawal penalty on top of income taxes [3]. A $200,000 distribution can trigger $70,000+ in combined taxes and penalties. This isn't a temporary setback—it's permanent capital destruction that eliminates years of retirement planning progress.

The 20% Withholding Trap Explained

Tax withholding complicates indirect rollovers from the moment you initiate them. Federal law mandates 20% withholding on any taxable eligible rollover distribution paid directly to you from employer-sponsored retirement plans [2].

Federal tax practitioners report that indirect rollover errors cost retirees an average of $12,000-$18,000 in avoidable taxes and penalties per incident.

This rule applies regardless of your intentions. Even if you plan to complete a full rollover within 60 days, the withholding happens automatically. The FRTIB has no discretion to waive it.

Real-World Impact on Federal Retirees

A civil service retirement system employee with a $300,000 traditional TSP balance receives $240,000 after mandatory withholding. To avoid taxation, she must deposit $300,000 into her new IRA within 60 days.

Finding $60,000 in liquid assets often requires:

- Depleting emergency savings accounts

- Selling taxable investment holdings (triggering capital gains)

- Taking personal loans with interest costs

- Liquidating physical assets at unfavorable prices

Engineers and business leaders approaching retirement typically maintain disciplined budgets. Coming up with tens of thousands of dollars on short notice conflicts with sound financial planning. The system effectively forces a partial withdrawal through the withholding mechanism.

Roth TSP Complications

Indirect rollovers from Roth TSP accounts face similar withholding issues. For non-qualified distributions, the TSP withholds 20% of the earnings portion for federal income taxes [4]. While Roth contributions move tax-free, earnings remain subject to withholding if distribution timing doesn't meet IRS qualification requirements.

This creates confusion for military service members and federal employees who assumed their Roth accounts provided complete tax protection. The withholding rule applies regardless of Roth status for certain distribution types.

Why Direct Rollovers Eliminate These Risks

Trustee-to-trustee transfers avoid every complication associated with indirect rollovers. When TSP funds move directly to your new IRA custodian, federal law treats the transaction differently.

No mandatory withholding applies because you never receive a distribution check [2]. Your full account balance transfers intact. A $200,000 rollover results in $200,000 arriving at your new institution.

The 60-day deadline disappears entirely. Direct rollovers operate on administrative timelines between the FRTIB and receiving custodians. Processing typically takes 1-2 weeks, but deadline pressure doesn't exist. Missing dates becomes impossible because you're not responsible for deposit timing.

Early withdrawal penalties cannot be accidentally triggered. The transfer codes properly on IRS Form 1099-R as a non-taxable rollover. Your new custodian issues Form 5498 confirming receipt. The paper trail documents a clean, penalty-free transfer.

The Direct Rollover Process

Federal employees initiate direct rollovers through straightforward steps:

- Choose your new IRA custodian and obtain their receiving information

- Complete Form TSP-70 or use the TSP online rollover system

- Specify direct rollover to your new custodian's account

- Provide routing numbers, account details, and custodian contact information

- Submit the completed forms to the FRTIB

The TSP handles everything from that point. Funds move from your G Fund, F Fund, C Fund, S Fund, and I Fund allocations directly to your designated account. You receive confirmation documentation but never touch the money personally.

The Myth of Using Indirect Rollovers as Short-Term Loans

Some financial commentary suggests treating indirect rollovers as interest-free 60-day loans. The idea involves taking the distribution, using funds for immediate needs like down payments or business investments, then replacing everything within the deadline.

This strategy represents extremely poor risk management for federal retirees. You're gambling your life savings against a calendar, betting that replacement funding materializes exactly on time with no complications.

The 20% withholding problem undermines this approach immediately. You only access 80% of your funds while remaining responsible for returning 100%. A $200,000 indirect rollover provides $160,000 in usable cash but requires $200,000 in deposits within 60 days.

Engineers and STEM professionals recognize the flawed risk-reward calculation. Minimal upside (temporary access to 80% of funds) versus catastrophic downside (permanent taxation and penalties on the full amount). No prudent financial analysis supports this use case.

Federal employees needing short-term liquidity while still employed can explore TSP loans with clear repayment terms. These structured borrowing options carry far less risk than treating retirement distributions as temporary funding sources.

When Each Rollover Type Makes Sense

For Risk-Averse Federal Retirees

You spent a career earning these retirement benefits through consistent service. You're influenced by peer recommendations from colleagues who've already retired and prefer straightforward yes/no guidance over complex technical analysis. Your priority centers on preservation rather than speculation.

The direct rollover eliminates every risk associated with fund transfers.

This approach suits federal employees and military veterans who value straightforward processes with minimal failure points. You want certainty that 100% of your capital reaches its destination safely, ready for whatever investment strategy you choose—whether traditional securities, precious metals IRAs, or diversified alternatives.

For Hands-On Investors

Financial confidence doesn't change IRS regulations. The 20% mandatory withholding applies regardless of your investment experience. The 60-day deadline remains absolute even for sophisticated investors.

Direct rollovers provide a different kind of control: elimination of rollover-specific risks. You maintain complete flexibility in investment selection once funds reach your new IRA. The transfer method simply ensures your full capital base arrives intact for deployment according to your strategy.

For Those Leaving Federal Service

Separation from federal employment brings extensive paperwork and numerous financial decisions. TSP rollover choices rank among the most consequential.

New federal retirees face the greatest vulnerability to indirect rollover problems. Without clear understanding of withholding mechanics and deadline requirements, seemingly simple options can trigger devastating tax consequences.

Indirect rollovers are occasionally used in limited scenarios under professional supervision, but they introduce timing and withholding risks that require precise execution. The direct rollover provides the secure path regardless of your financial knowledge level.

Tax Reporting and Documentation

Direct rollovers generate specific tax documentation that confirms the non-taxable transfer:

IRS Form 1099-R: The FRTIB issues this form showing your distribution. Box 7 contains code "G" indicating a direct rollover to an IRA. This signals to the IRS that the transaction wasn't a taxable event.

IRS Form 5498: Your new IRA custodian issues this form by May 31st of the following year. It reports the rollover contribution amount, confirming the receiving institution accepted your funds properly.

These forms work together to document the complete transfer. You report the 1099-R on your tax return, but the rollover code prevents taxation. The 5498 provides verification that funds arrived at your new retirement account.

Indirect rollovers create more complex reporting. The 1099-R shows a regular distribution without special coding. You must manually report the rollover on Form 1040, explaining that you completed the 60-day deposit requirement. Missing this reporting or failing to complete the deposit correctly results in full taxation.

Special Considerations for Different Account Types

Traditional TSP to Traditional IRA

This represents the most straightforward direct rollover scenario. Pre-tax contributions and earnings move from your TSP to a traditional IRA without tax consequences. The funds maintain their tax-deferred status.

Federal employees can then manage investments according to personal strategies. Some choose to maintain traditional securities allocations. Others redirect portions into alternative assets like precious metals IRAs for inflation protection.

Roth TSP to Roth IRA

Roth-to-Roth direct rollovers preserve the tax-free status of your contributions and earnings. These transfers avoid the withholding complications that affect non-qualified Roth distributions in indirect rollovers.

Military service members under the Blended Retirement System often maintain substantial Roth TSP balances. Direct rollovers to Roth IRAs provide continued tax-free growth potential without distribution timing restrictions.

Partial Rollovers

Federal employees can roll over portions of TSP balances while leaving other amounts in the plan. This flexibility supports various retirement income strategies.

A veteran might roll 30% of his TSP into a precious metals IRA for inflation hedging while keeping 70% in the TSP's low-cost index funds. Direct rollovers work for partial transfers just as effectively as full account movements.

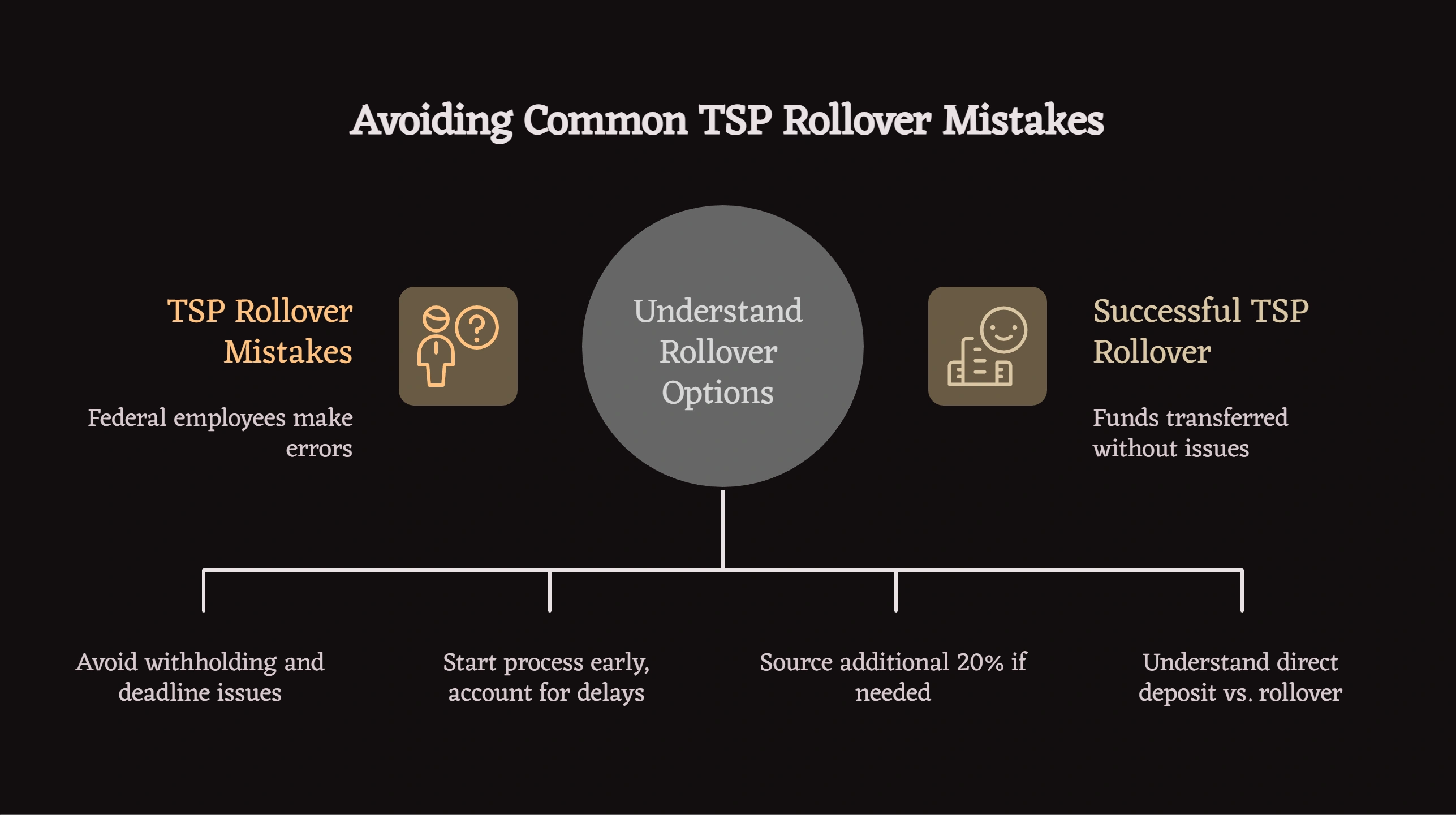

Common Mistakes Federal Employees Make

Assuming All Rollovers Work the Same Way

The term "rollover" covers both direct and indirect processes. Many federal retirees don't realize these methods carry dramatically different risks until after they've initiated an indirect transfer and received a check for 80% of their expected amount.

Underestimating the 60-Day Deadline

Two months sounds like ample time to complete a financial transaction. Real-world experience shows otherwise. Receiving institutions may require 7-10 days to establish new accounts. Documentation errors cause processing delays. Weekend and holiday calendar quirks compress actual business days available.

Failing to Account for Withholding

Federal employees often calculate rollover amounts based on their account balances without considering mandatory withholding. Discovering you need to source an additional 20% after the distribution arrives creates immediate financial stress.

Mixing Up Direct Deposit and Direct Rollover

Some federal retirees confuse direct deposit of TSP distributions into personal checking accounts with direct rollovers to retirement accounts. These are entirely different transactions. Direct deposit to checking accounts triggers the same withholding and deadline problems as checks mailed to your home.

Protection Strategies for Your Federal Retirement

Verify Receiving Institution Details

Before initiating any rollover, confirm your new IRA custodian's exact receiving information. Obtain routing numbers, account details, and proper mailing addresses directly from the institution. Errors in recipient information can delay transfers and create complications.

Document Everything

Maintain copies of all rollover paperwork, including Form TSP-70, receiving institution confirmations, and subsequent tax forms. This documentation proves compliance with IRS rules and protects against processing errors.

Consider Rollover Timing

Federal employees leaving service face multiple financial decisions simultaneously. TSP rollovers don't require immediate action. You can leave funds in the TSP temporarily while researching receiving institutions and planning your investment strategy.

This breathing room prevents rushed decisions under pressure. Direct rollovers remain available whenever you're ready to initiate them.

Consult Before Acting

Complex financial transactions benefit from professional guidance. Federal employee-focused financial advisors understand TSP-specific rules and can explain options clearly. This consultation occurs before you initiate any paperwork, while all options remain available.

FAQs

What's the main difference between direct and indirect TSP rollovers?

Direct rollovers move funds trustee-to-trustee without you receiving the money, avoiding withholding and deadlines. Indirect rollovers send you a check with 20% withheld, requiring you to deposit the full amount within 60 days.

Can I avoid the 20% withholding on an indirect rollover?

No. Federal law mandates 20% withholding on taxable distributions paid directly to you. The only way to avoid withholding is through a direct rollover where funds transfer between institutions.

What happens if I miss the 60-day deadline?

The undistributed funds become taxable income for that year. If you're under 59½, a 10% early withdrawal penalty applies on top of income taxes. This typically results in losing 30-40% of the affected amount.

How long does a direct TSP rollover take?

Processing typically requires 1-2 weeks from submission of complete paperwork. Complex transfers or documentation issues may extend this timeline, but you face no personal deadline pressure.

Can I roll over just part of my TSP balance?

Yes. Federal employees can execute partial rollovers while leaving remaining funds in the TSP. Both full and partial transfers work through the direct rollover process.

Do military members under BRS follow the same rules?

Yes. Military service members under the Blended Retirement System face identical rollover rules, withholding requirements, and deadline constraints as civilian federal employees.

Can I roll my TSP into a precious metals IRA?

Yes. Direct rollovers work for transfers to precious metals IRAs just like traditional IRA transfers. The trustee-to-trustee process remains the same regardless of your new IRA's investment focus.

What forms do I need for a direct TSP rollover?

Federal employees typically use Form TSP-70 (Request for Full Withdrawal) or the TSP online system. You'll need your new IRA custodian's receiving information including routing numbers and account details.

Protecting Decades of Federal Service

Your Thrift Savings Plan represents years of dedicated contributions and disciplined savings. Whether you served under the Civil Service Retirement System, contributed through federal employment, or earned these benefits as a military service member under the Blended Retirement System, these funds form the foundation of your retirement security.

The distinction between direct and indirect rollovers is not about investment choice, but about execution risk. Understanding how withholding, deadlines, and IRS treatment differ allows federal employees to preserve retirement capital during transitions. Direct rollovers eliminate the risks inherent in indirect transfers—mandatory withholding, strict deadlines, and potential penalties—making them the appropriate choice for most federal retirees protecting decades of service contributions.

Disclaimer: This article provides educational information about TSP rollover processes and does not constitute financial advice. Federal employees and military service members should consult qualified financial professionals before making retirement account decisions. Rollover choices involve individual circumstances including tax situations, investment objectives, and retirement timing.

References

[1] Code of Federal Regulations. "5 CFR § 1600.31 - Rollover Distributions." Cornell Law School Legal Information Institute.

[2] Internal Revenue Service. "Topic No. 413, Rollovers from Retirement Plans." IRS.gov.

[3] Investopedia. "How to Roll Over a Traditional Thrift Savings Plan to a Roth IRA." Updated 2025.

[4] Investopedia. "How to Roll Over a Roth Thrift Savings Plan to a Roth IRA." Updated 2025.

[5] Federal Retirement Thrift Investment Board. "Withdrawals in Retirement." TSP.gov.

[6] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition.

[7] U.S. Office of Personnel Management. "CSRS and FERS Handbook: Retirement Benefits." OPM.gov.