.svg)

When you leave federal service, your Thrift Savings Plan remains accessible with three primary options: keep funds in the TSP indefinitely, execute a direct rollover to an IRA or qualified plan, or take a withdrawal. TSP balances remain invested after separation regardless of whether you retire, resign, or transition to private sector employment. In 2026, federal employees maintain full account access with flexible withdrawal timing, contribution limits of $23,500 (plus $7,500 age 50+ catch-up), and no requirement to move funds immediately.

Key Takeaways

• Your TSP remains fully accessible after leaving federal service—no mandatory timeline to decide on rollovers or withdrawals

• The age 55 exception allows penalty-free TSP withdrawals if you separate in or after the year you turn 55—an advantage lost with IRA rollovers

• Direct rollovers preserve 100% of account value while indirect rollovers trigger 20% mandatory withholding

• Required Minimum Distributions must be calculated separately for TSP and IRAs—they cannot be aggregated across account types

Understanding Your TSP After Federal Service Ends

Separation from federal employment—whether through retirement after decades under the Federal Employees Retirement System (FERS) or Civil Service Retirement System (CSRS), voluntary resignation, or reduction in force—triggers important financial decisions. The Thrift Savings Plan represents one of the largest retirement assets for most federal employees, often containing hundreds of thousands in accumulated contributions and matching funds.

Unlike some employer retirement plans that force immediate decisions upon separation, the TSP permits extended evaluation periods. Federal employees face no deadline to choose between keeping funds in the plan, rolling over to an IRA, or taking distributions. This flexibility allows thoughtful decision-making during what can be a stressful life transition.

Why This Question Keeps Coming Up

Departing federal employees receive information from multiple sources—TSP exit seminars, financial advisors, IRA custodians, and colleagues who've already navigated this transition. Conflicting advice about "the best" option creates confusion. Understanding what actually happens to TSP accounts after separation—and the genuine timeline for making decisions—helps federal employees distinguish between urgent claims and actual requirements.

Your TSP Account Immediately After Separation

The day you separate from federal service, several TSP features change while others remain constant:

What Stays the Same:

- Full account balance remains invested in your selected funds (G, F, C, S, I, or L Funds)

- Existing fund allocations continue unless you change them

- Account access through TSP.gov and the ThriftLine

- Ability to change investment allocations among available funds

- Online withdrawal processing capability

- Beneficiary designations remain in effect

What Changes:

- No additional employee contributions or agency matching

- TSP loan eligibility ends—existing loans must be repaid or declared taxable distributions

- Contribution allocations become irrelevant without payroll deductions

- Certain withdrawal options become available that weren't accessible during employment

Federal employees maintaining TSP accounts after separation continue benefiting from the plan's extraordinarily low administrative costs. TSP expense ratios averaged 0.042% in 2024—among the lowest of any retirement plan available.

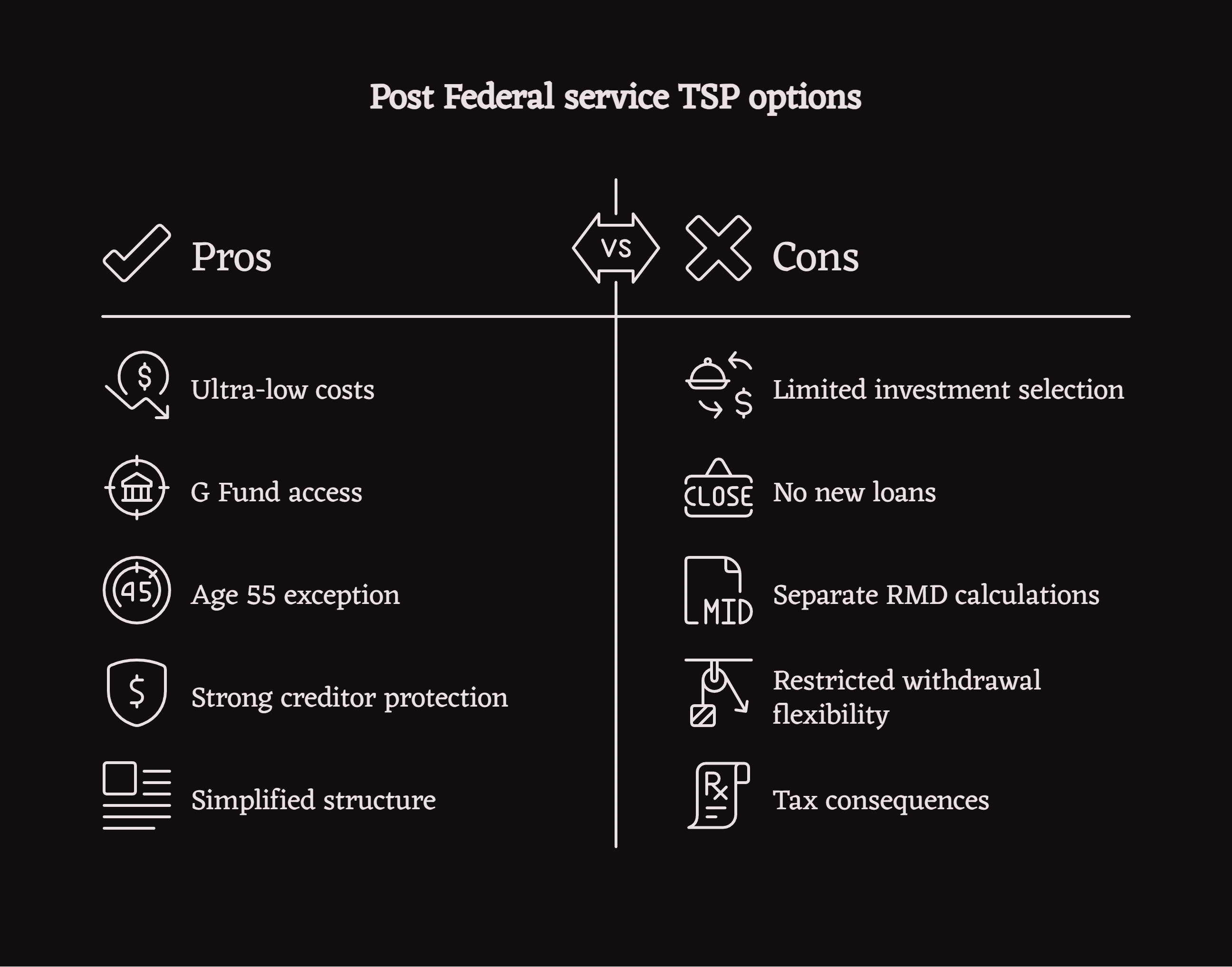

The Three Primary TSP Options After Federal Service

Option 1: Keep Funds in the TSP

Federal employees can maintain TSP accounts indefinitely after separation. No balance minimum exists, no maintenance fees apply, and no deadline forces eventual rollover or withdrawal decisions.

Advantages:

Ultra-low costs: TSP administrative and fund expense ratios remain dramatically lower than most IRA investment options. For a $200,000 account, this cost difference can exceed $1,000 annually compared to average IRA expense ratios.

G Fund access: The Government Securities Investment Fund offers principal protection with Treasury security rates unavailable in private IRAs. No comparable investment exists outside the TSP for this combination of safety and return.

Age 55 penalty exception: Federal employees who separate from service during or after the calendar year they turn 55 can take TSP withdrawals without the standard 10% early withdrawal penalty. This exception does NOT transfer to IRA rollovers—a critical distinction for early retirees.

Strong creditor protection: TSP assets enjoy robust federal law protection from creditors, bankruptcy proceedings, and legal judgments.

Simplified structure: Keeping money in the TSP requires no new account establishment, paperwork, or custodian relationships.

Disadvantages:

Limited investment selection: Despite recent expansion through the Mutual Fund Window, TSP investment options remain far narrower than typical IRA offerings at major brokerages.

No new loans: TSP loan eligibility ends upon separation. Federal employees who valued this liquidity feature lose access permanently.

Separate RMD calculations: Required Minimum Distributions beginning at age 73 must be calculated separately for TSP and any Traditional IRAs. These cannot be aggregated—the calculated TSP RMD must come specifically from the TSP.

Restricted withdrawal flexibility: While improved in recent years, TSP withdrawal options remain less flexible than IRA distribution capabilities for partial withdrawals and systematic payment plans.

Option 2: Roll Over to an IRA or New Employer Plan

Direct rollovers move TSP funds to Individual Retirement Accounts or new employer 401(k) plans without triggering taxation. Federal employees complete Form TSP-70, designating the receiving institution and account details.

Advantages:

Extensive investment choices: IRAs at Fidelity, Vanguard, Charles Schwab, or specialized custodians provide access to thousands of mutual funds, ETFs, individual stocks and bonds, real estate investment trusts, and alternative assets including precious metals IRAs for inflation protection.

Account consolidation: Federal employees with multiple retirement accounts from previous private sector employment can combine everything into a single Rollover IRA, simplifying management and oversight.

Roth conversion opportunities: IRAs permit strategic conversions from Traditional (pre-tax) to Roth (after-tax) status, potentially valuable for tax planning during low-income years between jobs.

Professional management access: IRAs enable direct relationships with financial advisors who manage investments according to personalized strategies.

Flexible beneficiary options: IRAs may offer more sophisticated estate planning tools for non-spouse beneficiaries than TSP Beneficiary Participant Accounts.

Disadvantages:

Higher expenses: IRA fund expense ratios typically exceed TSP costs. Annual IRA custodian fees, trading commissions, and advisor fees can significantly impact long-term returns.

Loss of G Fund: No IRA investment replicates the G Fund's government-guaranteed principal protection with market-based returns.

Loss of age 55 exception: The penalty-free early withdrawal benefit for federal employees separating at 55+ does not apply to IRA distributions. The standard 59½ age requirement applies instead.

Variable creditor protection: IRA creditor protections depend on state law and generally provide less comprehensive coverage than federal TSP protections.

Increased complexity: IRAs require active custodian selection, investment management, and ongoing oversight compared to TSP's simplified structure.

Federal employees weighing whether a precious metals IRA belongs in their rollover strategy may benefit from reviewing a comprehensive analysis of whether rolling a TSP into a gold IRA makes sense, including pros, cons, and common execution mistakes federal workers make.

Option 3: Withdraw TSP Funds as Cash

Federal employees can request full or partial TSP withdrawals, receiving funds as direct payments or periodic installments.

Advantages:

Immediate liquidity: Withdrawals provide cash access for urgent financial needs, business startup capital, major purchases, or debt elimination.

No ongoing account management: Complete withdrawals close TSP accounts, eliminating future Required Minimum Distribution calculations and administrative requirements.

Disadvantages:

Severe tax consequences: Withdrawals constitute taxable income at ordinary rates. The TSP withholds 20% for federal taxes automatically, with additional state tax withholding where applicable. Full distributions can push federal employees into higher tax brackets, dramatically increasing effective tax rates.

Early withdrawal penalties: Federal employees under 59½ face 10% IRS penalties on withdrawn amounts unless qualifying for specific exceptions (age 55 separation rule, disability, substantially equal periodic payments).

Permanent retirement savings loss: Withdrawn funds forfeit decades of potential tax-deferred growth. A $100,000 withdrawal at age 50 eliminates potentially $400,000-$500,000 in retirement value by age 70 assuming 7% annual returns.

No reversal: Unlike rollovers which can be reversed within 60 days, cash withdrawals are permanent. Once taxes and penalties are paid, that capital can never return to tax-advantaged status.

Direct vs. Indirect Rollover Mechanics

Federal employees executing TSP rollovers choose between two distinct processes with dramatically different risk profiles.

Direct Rollovers (Recommended)

Direct rollovers transfer funds from the TSP directly to the receiving IRA custodian or 401(k) plan administrator. Federal employees never receive checks or take personal possession of funds.

Process:

- Establish IRA at receiving institution (Fidelity, Vanguard, Schwab, precious metals IRA custodian, etc.)

- Obtain receiving institution's exact transfer instructions (routing numbers, account details)

- Complete Form TSP-70, specifying direct rollover to the new custodian

- Submit form through TSP.gov or mail to FRTIB

- Funds transfer within 2-3 weeks directly between institutions

Benefits:

- Zero tax withholding

- No 60-day deadline to track

- Clean tax reporting (Form 1099-R coded as non-taxable transfer)

- Eliminates all rollover mistake risks

Indirect Rollovers (High Risk)

Indirect rollovers involve the TSP sending distribution checks directly to federal employees, who must then deposit funds into qualified accounts within 60 days.

Process:

- Request TSP distribution without direct rollover designation

- Receive check for 80% of account value (20% withheld for taxes)

- Deposit full original amount into IRA within 60 calendar days

- Replace withheld 20% from personal funds

- Claim withholding refund on next year's tax return

Risks:

- Mandatory 20% withholding creates out-of-pocket funding requirement

- 60-day deadline converts entire distribution to taxable income if missed

- Life events (illness, family emergencies, administrative delays) cause deadline failures

- Requires tens of thousands in liquid reserves to replace withheld amounts

According to federal retirement specialists, over 15% of indirect rollovers fail to meet the 60-day deadline, triggering unintended taxes and penalties averaging $8,000-$15,000 per incident.

The Age 55 Early Withdrawal Exception

One of the TSP's most valuable features for early-retiring federal employees is penalty-free withdrawal access starting at age 55.

How the Exception Works

IRS regulations impose 10% penalties on retirement account distributions before age 59½. However, an exception exists for participants who separate from service during or after the calendar year they reach age 55 (age 50 for public safety employees including federal law enforcement and firefighters).

Example: A federal employee born June 1970 separates from service in December 2025 at age 55. Beginning immediately, she can take TSP withdrawals without 10% penalties (though distributions remain subject to ordinary income tax).

Critical limitation: This exception applies ONLY to the TSP (and other employer plans). It does NOT transfer to IRAs. If this employee rolls her TSP to an IRA, any distributions before 59½ face the full 10% penalty.

For federal employees retiring between 55-59, this represents a powerful liquidity advantage worth preserving by keeping funds in the TSP rather than rolling to an IRA.

Required Minimum Distribution Considerations

Federal law requires retirement account distributions beginning at age 73 (for those reaching 72 after December 31, 2022). Understanding RMD mechanics helps federal employees with both TSP accounts and IRAs avoid costly mistakes.

TSP-Specific RMD Rules

The TSP calculates Required Minimum Distributions based on account balances and IRS life expectancy tables. Federal employees must withdraw the calculated amount from their TSP specifically—this requirement cannot be satisfied through IRA withdrawals.

Complication for mixed accounts: A federal employee with $200,000 in TSP and $300,000 across three Traditional IRAs faces:

- TSP RMD of approximately $7,300 (must come from TSP)

- Combined IRA RMD of approximately $10,900 (can come from any single IRA or combination)

The TSP RMD must be withdrawn from the TSP itself. Federal employees cannot aggregate TSP and IRA RMDs the way multiple IRA RMDs can be aggregated.

Penalty for failure: Missing RMD deadlines triggers 25% excise penalties on amounts not withdrawn (reduced to 10% if corrected within two years).

TSP Loan Status After Separation

Federal employees with outstanding TSP loans at separation face specific repayment requirements.

General purpose loans ($50,000 maximum, 1-5 year terms) and residential loans ($50,000 maximum, 1-15 year terms) must be repaid in full within 90 days of separation. Failure to repay results in:

- Outstanding balance declared as taxable distribution

- 10% early withdrawal penalty if under 59½

- Permanent loss of that retirement capital

Federal employees planning separation should either:

- Repay TSP loans fully before final separation date

- Prepare to repay within the 90-day window

- Accept the tax consequences of defaulted loan treatment

No option exists to continue loan repayments after separation. New employers' 401(k) plans cannot assume existing TSP loans.

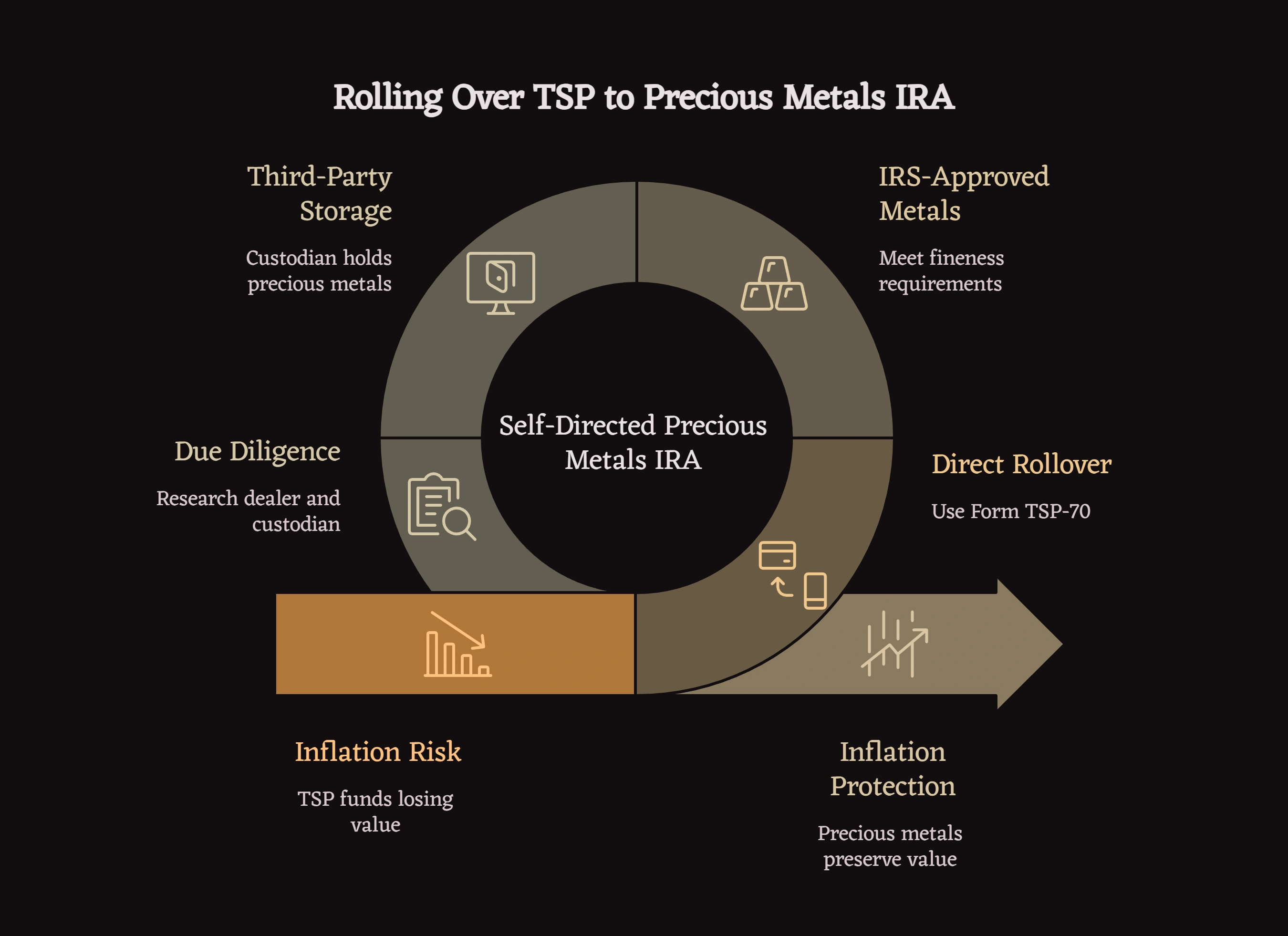

Precious Metals IRAs as TSP Rollover Destinations

Federal employees seeking inflation protection through alternative assets can roll TSP funds into self-directed IRAs permitting precious metals holdings.

Mechanics and Requirements

Self-directed precious metals IRAs accept direct rollovers from TSP accounts following the same Form TSP-70 process used for traditional IRA rollovers. However, these specialized accounts involve additional compliance requirements:

IRS-approved metals only: Gold must meet .995 fineness; silver requires .999 fineness. Approved products include American Gold Eagles, Canadian Gold Maple Leafs, and specific bullion bars from qualified refiners.

Mandatory third-party storage: IRA-owned precious metals must remain with IRS-approved custodians at qualified depositories. Personal possession triggers immediate taxation and penalties.

Higher fee structures: Precious metals IRAs typically involve setup fees ($50-$300), annual custodial fees ($75-$300), storage fees ($100-$300), and dealer spreads over spot prices (4-15% for legitimate dealers, potentially 30-50% for predatory firms).

Specialized custodians: Firms like Noble Gold, Goldco, Augusta Precious Metals, Patriot Gold Group, Birch Gold Group, and others specialize in precious metals IRA administration, handling both custodianship and depository relationships.

Federal employees considering this strategy should conduct extensive due diligence on dealer pricing transparency, custodian track records, and total fee structures. CFTC enforcement data shows precious metals fraud cases involving dealer markups averaging 47% over spot price—compared to legitimate spreads of 4-8%.

Federal employees evaluating whether precious metals fit within broader retirement strategies may benefit from reviewing comprehensive analyses of whether rolling over a TSP into a gold IRA makes sense for their situation, including benefits, trade-offs, and common execution mistakes.

Timeline Flexibility: No Rush Required

Unlike some employer retirement plans that force distributions within specific timeframes after separation, the TSP imposes no such requirements.

What this means practically:

A federal employee separating in January 2026 can:

- Leave funds in TSP through 2026, 2027, and beyond

- Maintain existing fund allocations or adjust them through TSP.gov

- Initiate rollovers in 2028 if that timing suits their circumstances better

- Take withdrawals whenever needed (subject to age-based penalty rules)

This extended timeline permits federal employees to:

- Settle into new employment before making major financial decisions

- Allow dust to settle from stressful separation circumstances

- Research IRA options thoroughly without artificial deadline pressure

- Consult financial advisors and tax professionals during less chaotic periods

The only mandatory timeline involves Required Minimum Distributions beginning at age 73. Before that age, federal employees control all withdrawal and rollover timing.

Making the Right Decision for Your Circumstances

No universal "best" option exists for TSP accounts after federal service. The optimal choice depends on individual circumstances, financial objectives, and personal priorities.

When Keeping TSP Makes Sense

Consider leaving funds in the TSP if you:

- Value the G Fund's safety and guaranteed returns

- Separated between ages 55-59 and may need penalty-free access before 59½

- Appreciate ultra-low administrative costs

- Prefer simplified investment management

- Face uncertainty about next career steps and want to defer decisions

- Have modest balances making IRA fees proportionally expensive

When IRA Rollovers Make Sense

Consider rolling to an IRA if you:

- Want investment options beyond TSP's core funds

- Plan to work with a financial advisor on personalized strategies

- Need to consolidate multiple retirement accounts for simplified management

- Seek alternative assets like real estate or precious metals for diversification

- Value flexible withdrawal options for retirement income planning

- Have substantial balances justifying IRA custodian relationships

When Withdrawals Make Sense (Rare)

Consider withdrawals only if you:

- Face genuine financial emergencies with no other funding sources

- Need to eliminate high-interest debt after exhausting all alternatives

- Have calculated full tax consequences and accept permanent retirement capital loss

- Understand withdrawal irreversibility and long-term growth forfeiture

For most federal employees, withdrawals represent the least attractive option due to severe tax consequences and permanent loss of tax-advantaged growth potential.

Protection Strategies During Transition

Document Your Status

Maintain comprehensive records of:

- Final leave and earnings statements showing separation date

- TSP account statements at separation

- Beneficiary designation forms

- Any rollover or withdrawal paperwork

- Tax forms (1099-R from TSP, 5498 from receiving IRAs)

Verify Beneficiary Designations

Separation often coincides with life changes (divorce, remarriage, new children) affecting beneficiary preferences. Review and update TSP beneficiary forms to reflect current intentions.

Coordinate with FERS Pension Decisions

TSP decisions operate independently from FERS pension elections, but both affect overall retirement income. Federal employees should coordinate TSP strategies with:

- FERS annuity timing and survivor benefit elections

- Social Security claiming strategies

- Federal Employees Health Benefits continuation

- Federal Employees Group Life Insurance decisions

Consult Before Acting

Complex financial transitions benefit from professional guidance. Federal employees should consider consulting:

- Fee-only fiduciary financial advisors specializing in federal benefits

- Qualified tax professionals familiar with TSP and IRA regulations

- Estate planning attorneys for beneficiary and wealth transfer strategies

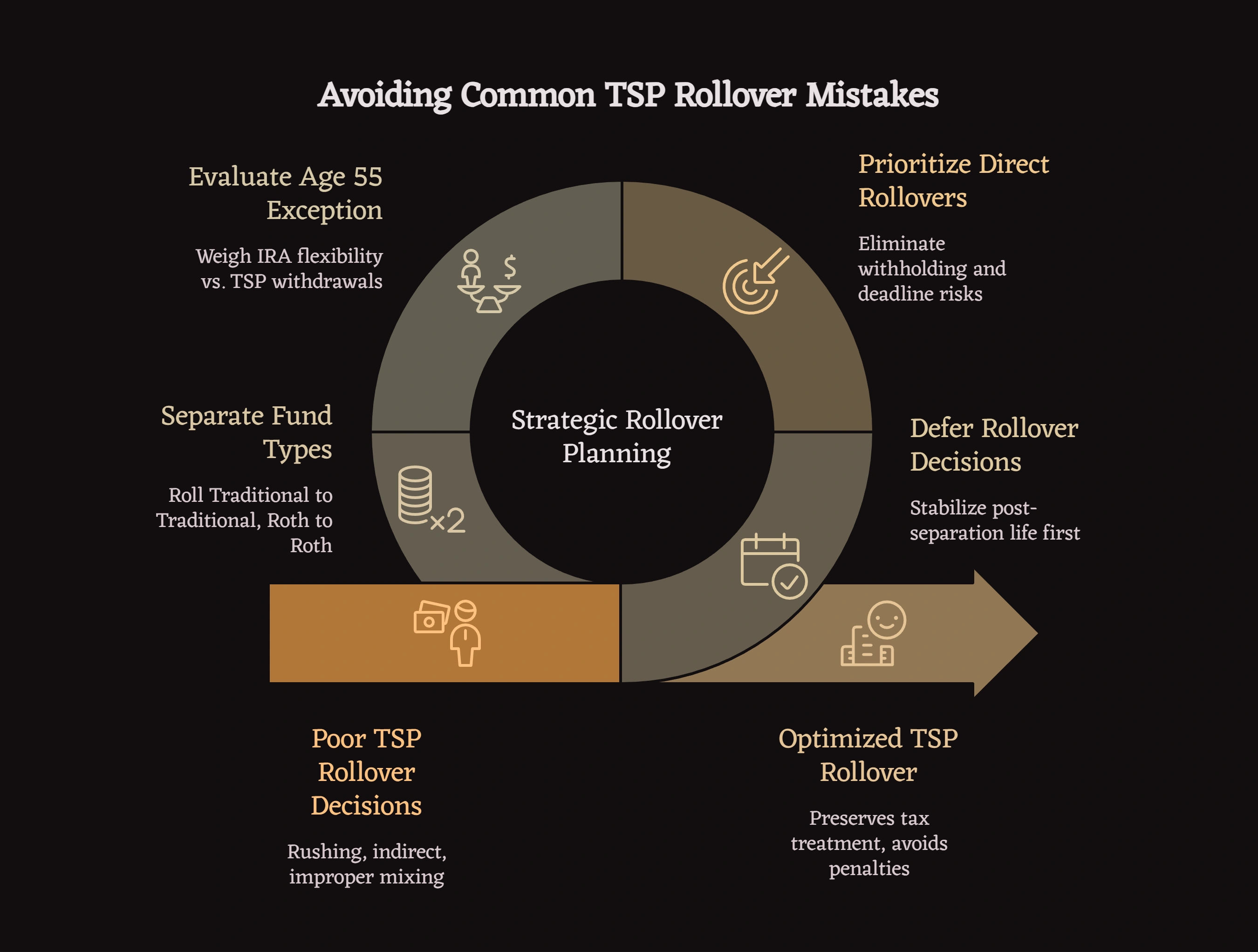

Common Mistakes Federal Employees Make

Rushing Into Rollovers

Separation stress creates urgency around financial decisions. Many federal employees initiate rollovers immediately upon separation without thoroughly evaluating whether leaving funds in TSP better serves their circumstances.

Better approach: Unless specific circumstances require immediate rollovers (like consolidating accounts to simplify RMDs for elderly retirees), federal employees benefit from deferring rollover decisions until post-separation life stabilizes.

Choosing Indirect Over Direct Rollovers

Despite clear advantages of direct rollovers, some federal employees request indirect distributions, believing they need to "see" the money or wanting temporary access to funds.

Reality: The 20% withholding and 60-day deadline create significant failure risks. Direct rollovers eliminate these entirely while accomplishing the same objective.

Ignoring Age 55 Exception Value

Federal employees separating at 55-59 who roll TSP funds to IRAs forfeit penalty-free early withdrawal access—often without realizing this consequence until they need distributions.

Better approach: Federal employees planning early retirement should carefully evaluate whether IRA investment flexibility outweighs the value of penalty-free TSP withdrawals during the 55-59 age window.

Mixing Traditional and Roth Funds Improperly

TSP accounts can contain both Traditional (pre-tax) and Roth (after-tax) balances. Rolling these to a single destination account creates tax reporting complications.

Correct approach: Traditional TSP funds should roll to Traditional IRAs; Roth TSP funds should roll to Roth IRAs. Maintain separate account types to preserve proper tax treatment.

FAQs

How long can I keep my money in the TSP after leaving federal service?

Indefinitely. The TSP imposes no deadline for rollovers or withdrawals after separation. Federal employees can maintain TSP accounts for decades if desired, subject only to Required Minimum Distribution rules beginning at age 73.

Can I contribute to my TSP after leaving federal employment?

No. TSP contributions require active federal employment with payroll deductions. Once separated, no additional contributions are possible regardless of account status.

What happens to my TSP if I'm rehired by the federal government?

Your existing TSP account reactivates. Contributions resume through payroll deductions, and your previous balance continues growing with new deposits and any employer matching.

Can I take a TSP loan after separation?

No. TSP loan eligibility ends upon separation from federal service. Outstanding loans must be repaid within 90 days or they become taxable distributions.

Do I have to pay taxes on my TSP when I leave federal service?

Not automatically. TSP accounts remain tax-deferred after separation until you take distributions. Direct rollovers to IRAs continue tax-deferred status. Only withdrawals trigger taxation.

What is the difference between leaving my TSP and rolling it over?

Leaving your TSP means keeping funds in the plan with continued access to TSP investment options and features. Rolling over means moving funds to an IRA or new employer plan, changing investment options and plan rules but maintaining tax-deferred status.

Can I roll my TSP into my new employer's 401(k)?

Yes, if the new employer's plan accepts rollovers. Not all 401(k) plans permit incoming transfers. Check with your new employer's plan administrator before initiating the rollover.

What happens to my TSP if I die?

TSP funds pass to your designated beneficiaries according to beneficiary forms on file with the FRTIB. Spousal beneficiaries can roll inherited TSP funds to their own IRAs or inherited IRAs. Non-spouse beneficiaries receive distributions according to specific IRS rules for inherited retirement accounts.

Protecting Decades of Federal Service

Your Thrift Savings Plan represents years of disciplined contributions and employer matching earned through federal service. Whether you served under FERS, CSRS, or as a uniformed service member, these funds form a critical component of retirement security.

The decision of what to do with your TSP after separation affects long-term financial outcomes through investment returns, tax consequences, and withdrawal flexibility. Understanding your actual options—and the genuine timeline for making decisions—helps federal employees navigate this transition thoughtfully rather than reactively.

For most federal employees, the optimal approach involves deferring major TSP decisions until post-separation circumstances stabilize, carefully evaluating whether the TSP's low costs and unique features outweigh IRA flexibility, and prioritizing direct rollovers over indirect transfers when rollovers make sense.

Disclaimer: This article provides educational information about TSP options after federal service and does not constitute financial, tax, or legal advice. Federal employees and military service members should consult qualified financial advisors, tax professionals, and legal counsel before making retirement account decisions. TSP decisions involve individual circumstances including tax situations, investment objectives, retirement timing, and risk tolerance. The Federal Retirement Thrift Investment Board provides official TSP guidance through TSP.gov, which should be reviewed for authoritative plan information.

References

[1] Federal Retirement Thrift Investment Board. "Withdrawals in Retirement." TSP.gov.

[2] Internal Revenue Service. "Publication 575: Pension and Annuity Income." 2025 Edition. IRS.gov.

[3] Internal Revenue Service. "Topic No. 558: Additional Tax on Early Distributions from Retirement Plans." IRS.gov.

[4] Federal Retirement Thrift Investment Board. "Form TSP-70: Request for Full Withdrawal." TSP.gov.

[5] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[6] U.S. Office of Personnel Management. "FERS Information." OPM.gov.

[7] Internal Revenue Service. "Retirement Topics - Required Minimum Distributions (RMDs)." IRS.gov.

[8] Federal Retirement Thrift Investment Board. "TSP Loan Program." TSP.gov.

[9] Internal Revenue Service. "IRC Section 408(m): Treatment of Collectibles in IRAs." IRS.gov.

[10] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020-2024." CFTC.gov.