.svg)

For high-net-worth investors, the conventional wisdom peddled by popular “best gold IRA” listicles is not just inadequate; it’s a strategic liability. The crucial decision isn’t choosing a dealer with the lowest fees, but forging a specialized custodian-dealer partnership designed for institutional-grade security, dedicated white-glove service, and seamless integration into a comprehensive wealth preservation plan. This guide re-frames the entire process for those with substantial assets to protect.

Executive summary: gold IRAs for larger retirement balances

A gold IRA can play a legitimate role in wealth preservation for investors with $100K+ retirement balances — but only when structured correctly.

Key principles:

- Custodian selection matters more than dealer branding

- Segregated, fully insured storage is non-negotiable at scale

- Dealer markups commonly matter more than annual fees

- Providers designed for small accounts often fail HNW needs

Investors considering allocations above $50K should evaluate providers differently than retail investors. This guide explains the foundational differences between retail-focused gold IRA strategies and approaches designed for substantial wealth preservation.

In this guide, “high-net-worth gold IRA” refers to retirement allocations typically above $100,000, where storage structure, dealer pricing transparency, insurance limits, and service model materially affect outcomes.

Who this guide is designed for

This guide is intended for investors with six- or seven-figure retirement portfolios who prioritize capital preservation, inflation protection, and long-term wealth transfer — not speculative returns or promotional incentives. If you’re evaluating a gold IRA allocation under $50,000, or if your primary goal is maximizing short-term gains, other resources may better serve your needs.

This guide is not designed for investors seeking low-minimum gold IRA accounts, short-term trading exposure, or promotional precious metals offers. Those evaluating allocations under $50,000 may encounter different fee structures, service models, and provider priorities.

Investors allocating substantial retirement capital to a gold IRA often require a different service model than retail-focused providers can offer. Firms such as Augusta Precious Metals are structured around education-first onboarding, transparent pricing, and gold-and-silver-only portfolios designed for long-term wealth preservation rather than short-term trading. To understand whether this approach aligns with your retirement goals, see our in-depth analysis of Augusta Precious Metals for investors with higher-balance retirement accounts.

The Deception of Simplicity: Why Popular Gold IRA Listicles Fail the High-Net-Worth Investor

A quick search for gold IRA information reveals a landscape dominated by affiliate-driven review sites. These platforms rank companies based on metrics that are, for a sophisticated portfolio, entirely irrelevant and often serve as red flags. They champion low minimum investment requirements, beginner-friendly platforms, and promotional offers of "free" silver. For an investor considering a gold IRA rollover for accounts over $100k, or even a seven-figure allocation, these criteria are distractions from what truly matters.

Metrics like a low minimum investment, while appealing to the masses, signal a business model focused on volume, not bespoke service. An investor looking into the benefits of a gold IRA in a recession for a multi-million dollar portfolio has needs that fundamentally differ from someone starting with a small account. The focus on "beginner-friendliness" often translates to a one-size-fits-all approach that cannot accommodate complex estate planning with a self-directed gold IRA or the specific requirements for opening a gold IRA account with intricate trust structures.

Worse, this retail-focused model can obscure significant hidden costs. The emphasis on low setup or storage fees often masks exorbitant dealer markups on the precious metals themselves, a practice known as the IRA precious metals dealer markup. These hidden costs can be devastating.

In one stark example, government regulators documented a case where a dealer and custodian charged a client nearly $150,000 in commissions and fees on a $300,000 retirement account rollover—a 50% haircut on the initial investment before it even had a chance to perform according to the Commodity Futures Trading Commission. This is precisely the kind of pitfall that a high-net-worth retirement strategy with gold must be engineered to avoid.

The Foundational Decision: Prioritizing the Custodian Before the Dealer

The single most critical error in the typical gold IRA setup process is selecting the metal dealer first. The dealer, whose primary role is to sell you physical precious metals, often directs you to their preferred custodian. This creates an inherent conflict of interest. The true foundation of a secure self directed ira for precious metals is the custodian—the institution responsible for the administration and safekeeping of your assets.

Legally, setting up a Gold IRA requires a specialty custodian, and the physical gold must be stored in an IRS-approved facility as mandated by regulations. The entire process involves finding a qualified trustee, selecting an approved depository for storage, purchasing the approved physical gold or silver, and ensuring it is transferred accountably. This is not merely paperwork; it’s the bedrock of your asset’s security.

A critical point to understand is that self-directed IRA custodians do not—and legally cannot—offer investment advice or vet the legitimacy of the assets in the account as stated by the SEC’s Office of Investor Education and Advocacy. Their job is to hold and administer. Therefore, finding a trustworthy gold IRA custodian that specializes in handling seven- and eight-figure accounts is the first priority. These specialized custodians have established relationships with multiple top-tier dealers and depositories, offering you choice and a layer of institutional due diligence that a standalone retail dealer cannot provide. They understand the complexities of a SEP gold IRA for business owners or a Roth gold IRA contribution for high earners and can work directly with your existing financial advisor on gold IRAs.

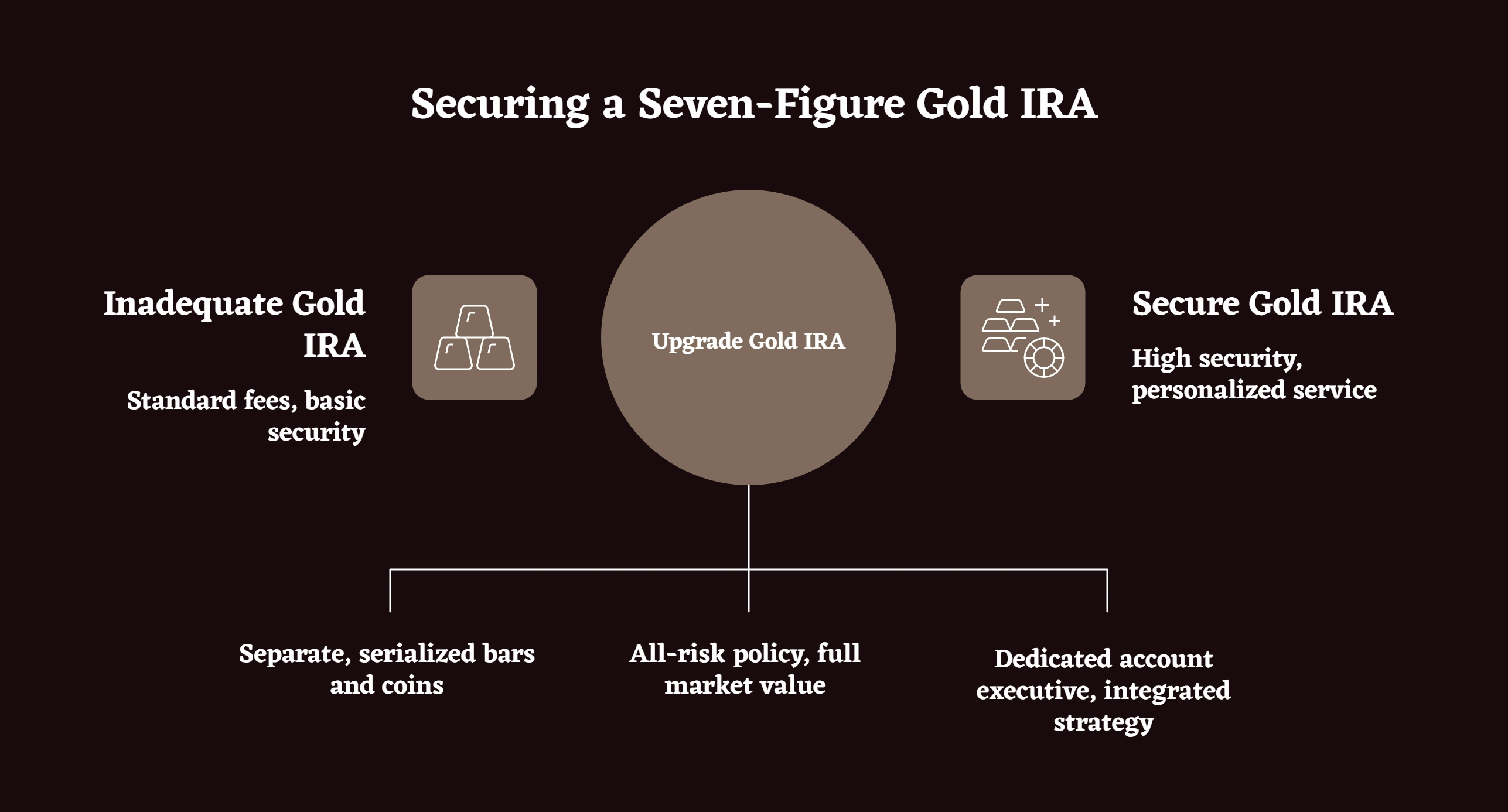

Beyond the Price Tag: The True Economics of Securing a Seven-Figure Gold IRA

For a substantial portfolio, standard fees are a minor detail compared to the non-negotiable value of security and service. The conversation must shift from “What are the fees for a $250,000 gold IRA?” to “What is the security protocol for a multi-million dollar precious metals investment?”

Segregated Storage vs. Commingled Storage

Many low-cost providers use commingled, or allocated, storage. This means your metals are stored alongside those of other clients. While it meets the basic requirements, it falls short for large accounts. Segregated storage, often available at private vault storage facilities, means your specific, serialized bars and coins are held separately in your name. When comparing gold IRA storage facilities, this is a paramount distinction. For estate planning purposes and absolute clarity of ownership, segregated storage is the only prudent choice. It ensures that the exact assets you purchased are the ones held for you, which is critical when liquidating a gold IRA account or passing it to heirs.

Comprehensive, All-Risk Insurance

Standard insurance policies may have coverage limits that are inadequate for a sizable holding. A high-net-worth custodian-dealer partnership will ensure your assets are protected by a comprehensive, all-risk insurance policy, often from specialized underwriters like Lloyd’s of London, that covers theft, damage, and loss up to the full market value of your holdings. This goes far beyond the basic coverage offered by many retail-focused firms and is a key component of fully insured gold IRA storage solutions.

White-Glove Service and Advisory Integration

A seven-figure account should never be managed through a call center. A top-tier service provides a dedicated account executive—a single point of contact who understands your entire financial picture. This person can coordinate with your wealth manager, CPA, and estate attorney to ensure the gold IRA functions as an integrated part of your overall strategy for wealth preservation. They assist with understanding gold IRA paperwork and setup, facilitate smooth transactions when you transfer an existing IRA to a gold IRA company, and provide clear information on precious metals IRA performance tracking. This level of service is simply not available from providers focused on the mass market, even those like American Hartford Gold or when doing an Augusta Precious Metals review for HNW investors; their model is built for a different client.

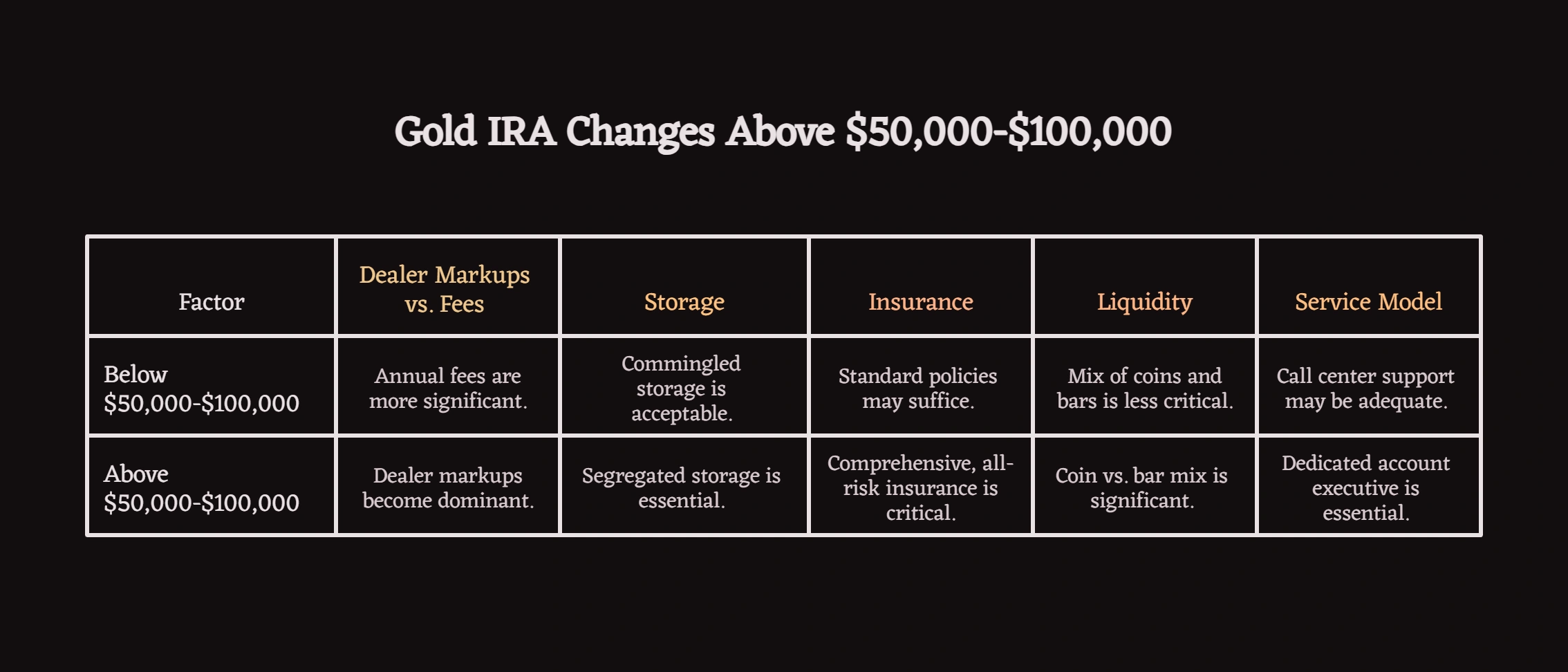

What changes when a gold IRA exceeds $50,000–$100,000

As a gold IRA portfolio reaches and exceeds six figures, several operational and strategic factors shift in importance:

- Dealer markups outweigh annual fees: On a $250,000 purchase, a 5% dealer markup costs $12,500—far more than the difference between a $200 and $400 annual storage fee. At scale, negotiating transparent, competitive pricing on precious metals becomes the dominant economic consideration.

- Storage segregation becomes non-negotiable: With commingled storage, your assets are stored with other clients’ holdings. While this meets IRS requirements, it creates ambiguity around ownership during estate settlement and limits your control. Segregated storage—where your specific, serialized bars and coins are held separately—provides the clarity essential for large balances.

- Insurance limits matter: Many standard policies cap coverage at levels inadequate for substantial holdings. Ensuring comprehensive, all-risk insurance from specialized underwriters that covers the full market value of your assets is critical.

- Liquidity mechanics change: The mix of sovereign coins versus bars takes on new significance. Coins offer superior liquidity for distributions or emergency capital needs, while bars provide more efficient bulk acquisition for core holdings.

- Service model becomes critical: Call center support is unsuitable for complex, high-value accounts. A dedicated account executive who coordinates with your broader advisory team—wealth managers, CPAs, estate attorneys—becomes essential infrastructure.

Strategic Allocation: Structuring Your Physical Assets for a Volatile Future

Once the custodian and security infrastructure are in place, the focus turns to the assets themselves. This isn’t just about buying gold; it’s about strategic acquisition. The debate over buying gold bars vs coins for an IRA takes on new meaning for the high-net-worth investor.

- Sovereign Coins: IRA approved gold coins, such as American Eagles or Canadian Maple Leafs, offer superior liquidity. Their recognizability and government backing make them easier to sell quickly without significant disputes over authenticity or weight. This is vital for RMDs (Required Minimum Distributions) or if a sudden need for capital arises.

- Bars: Larger gold bars typically carry a lower premium over the spot price, making them a more efficient way to acquire sheer weight of gold. For a large-scale gold investment focused purely on long-term wealth preservation and as an inflation hedge for a multi-million dollar portfolio, bars can be the most cost-effective option for the core of the holding.

- Platinum and Palladium: For further diversification within tangible assets, a self-directed IRA can also hold platinum and palladium IRA options. These metals have significant industrial use cases, giving them a different risk and reward profile compared to gold’s monetary safe-haven status.

The optimal strategy often involves a mix: a foundation of low-premium bars for core wealth preservation, supplemented by a tranche of sovereign coins for liquidity and transactional ease. This structured approach, a hallmark of high-net-worth retirement strategies with gold, transforms a simple purchase into a sophisticated component of legacy planning. Not all providers support platinum and palladium IRAs, which may influence diversification options for certain portfolios.

A Tale of Two Strategies: The Retail Approach vs. The HNW Fortress

The path you choose has profound implications for the security and efficacy of your precious metals investment. Here is a direct comparison of the two divergent philosophies.

Retail-Focused Gold IRA Selection

Driven by listicles, low advertised fees, and promotional offers. This is the common path for the mainstream retiree.

Key Decision Driver: Lowest initial cost and ease of setup.

Pros: - Low barrier to entry, often with minimums well below $50,000. - Simple, streamlined process designed for mass-market appeal.

Cons: - High potential for hidden costs via excessive dealer markups. - Often uses commingled storage, reducing individual asset control. - Impersonal, call-center-level customer service. - Lacks integration with broader, sophisticated wealth management strategies. - Inadequate insurance coverage for substantial seven-figure accounts.

High-Net-Worth Gold IRA Strategy

Driven by a custodian-first approach, institutional security, and seamless integration with a comprehensive wealth plan.

Key Decision Driver: Maximum security, bespoke service, and strategic asset preservation.

Pros: - Prioritizes institutional-grade, segregated storage in high-security private vaults. - Provides a dedicated account executive for white-glove, personalized service. - Offers transparent, competitive pricing on metals appropriate for large-volume purchases. - Ensures comprehensive, all-risk insurance suitable for high-value holdings. - Facilitates seamless coordination with your existing team of financial advisors, attorneys, and accountants.

Cons: - Higher minimum investment requirements, commonly structured for balances of $100,000 or more. - Annual fees for segregated storage and enhanced insurance may be higher in absolute terms (but offer far greater value).

Addressing Common Objections from Financial Traditionalists

Even with a sound strategy, investors often encounter resistance based on outdated or incomplete information. It’s important to understand these arguments and their context.

What is the downside of a gold IRA?

The primary downsides are illiquidity and cost. Unlike stocks or ETFs, physical gold isn’t instantly saleable. The process of liquidating a gold IRA account takes time. Additionally, there are costs for storage, insurance, and custodian administration that do not exist with paper assets. There are also tax implications of a precious metals IRA; while gains are tax-deferred, distributions are taxed as ordinary income, and there are consequences of early withdrawal just like with a traditional IRA.

Why don’t Warren Buffett buy gold?

Warren Buffett’s investment philosophy is rooted in value creation. He invests in productive businesses that generate cash flow, earnings, and dividends. Gold, in his view, is a non-productive asset. It sits in a vault and does not create anything. His argument is that an ounce of gold will always be just an ounce of gold, whereas an investment in a great business can grow exponentially. He is betting on the continued productivity and stability of the economic system, a premise that many who seek gold as a hedge are beginning to question.

Why does Dave Ramsey say not to invest in gold?

Dave Ramsey’s advice is geared toward the average person working to get out of debt and build wealth through conventional, mainstream methods like mutual funds. His perspective is that gold’s long-term returns have historically underperformed the stock market. For his audience, which is not typically composed of high-net-worth individuals worried about systemic risk and currency devaluation, the simplicity and historical growth of the broad market is a more straightforward path. His advice, like the listicles, is not tailored for wealth preservation on a grand scale.

When a provider like Augusta Precious Metals makes sense

Investors with retirement balances above $50,000 who value education, onboarding depth, and long-term gold and silver exposure — without interest in platinum or palladium — often gravitate toward providers like Augusta Precious Metals.

Augusta’s model reflects a deliberate departure from the mass-market approach. Their higher minimum investment threshold, educational focus, and limitation to gold and silver only creates a service structure aligned with investors who prioritize understanding over volume. The question isn’t whether Augusta is “the best” provider, but whether their specific structure, minimums, and service model align with your portfolio size, goals, and preference for a more consultative relationship.

We break down if Augusta’s structure, minimums, and service model align with your retirement strategy in our detailed analysis of whether Augusta Precious Metals is the right fit for larger retirement portfolios.

Choosing a gold IRA strategy based on portfolio size and goals

The "best" strategy is entirely dependent on your financial stature, goals, and worldview. Declaring a single winner would be a disservice. Instead, identify which profile best describes your situation.

The High-Net-Worth (HNW) Investor — complex portfolios, advisory teams, capital preservation focus

You possess a complex, multi-asset portfolio and likely work with a team of wealth managers and advisors. Your primary goal with a gold IRA is not speculative growth, but long-term wealth preservation, an inflation hedge, and a bulwark against geopolitical or currency crises. For you, the HNW strategy is the only logical path. You must prioritize the quality of the custodian-dealer partnership, demand segregated storage and institutional-grade security, and insist on a level of white-glove service that integrates seamlessly with your existing financial plan. The slightly higher fees are an insignificant cost for securing a meaningful portion of your legacy.

The Mainstream Retiree — standard retirement accounts, fee-sensitive, retail providers

Your focus is on protecting a standard retirement account, like a 401(k) or TSP, valued in the low-to-mid six figures. You are sensitive to fees and are the primary audience for the well-known brands like Goldco, Noble Gold, and others found on typical review sites. For you, the retail-focused approach can be appropriate, provided you do your due diligence. It is imperative to ask direct questions about dealer markups, understand the difference between commingled and segregated storage, and be aware of the potential for high-pressure sales tactics. Some providers in this space, like Augusta Precious Metals, have a higher minimum investment of $50,000 according to industry analysis, indicating a move toward a more serious client base, which may be a better fit.

The Conservative 'Prepper' — system distrust, tangible asset focus, private storage priority

Your motivation is driven primarily by a deep distrust of financial systems, concern over national debt, and the potential for systemic collapse. You value tangible assets above all else. For you, a gold IRA is a good step, but the question of "gold IRA vs physical gold" held directly is central. While an IRA offers significant tax advantages, it also means your metal is held by a third-party custodian. You may find that a hybrid approach is best: a self-directed gold IRA for tax-advantaged savings, supplemented by a significant holding of physical gold and silver stored securely and privately, outside the financial system entirely. The ability to take physical delivery from my gold IRA upon retirement is a key feature you should confirm with any provider.

Making the right choice for your needs

The landscape of our national economy and its place in the world is shifting. For those who have built substantial wealth, protecting it is not a passive activity. It requires a deliberate, strategic approach that looks beyond simplistic advice and focuses on the foundational principles of security, service, and sovereign value.

Different providers serve different investor profiles:

- Augusta Precious Metals tends to attract larger, education-focused accounts seeking a consultative relationship.

- Birch Gold Group often appeals to investors seeking flexibility across metals with established institutional relationships.

- Noble Gold fits smaller to mid-size accounts, particularly TSP-focused rollovers for federal and military members, as well as younger investors seeking diversification beyond traditional index funds and crypto exposure.

Understanding which structure aligns with your balance size and goals matters more than choosing a brand name. The right precious metals strategy is a critical component in ensuring your wealth endures for generations to come.