.svg)

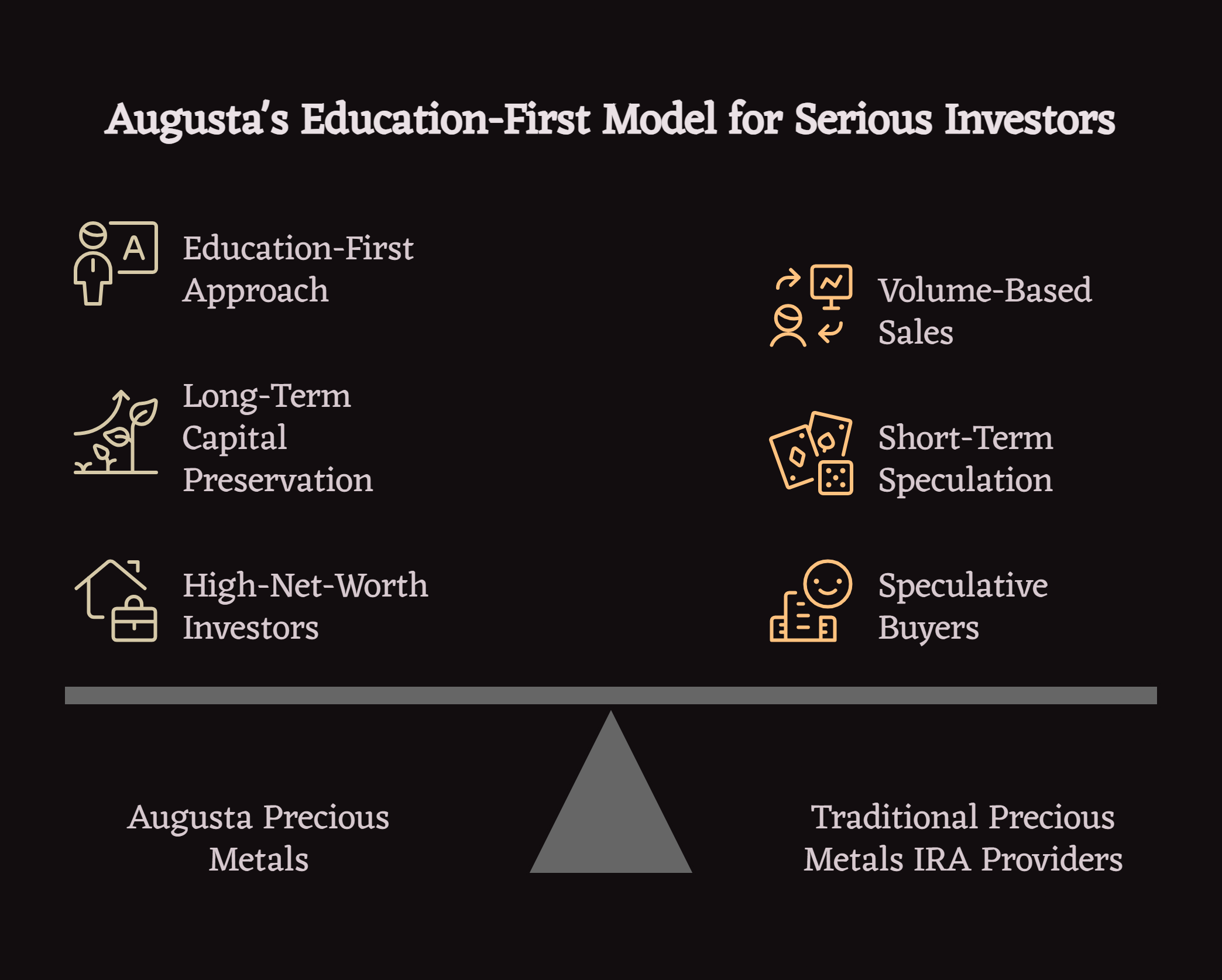

Augusta Precious Metals operates differently from most gold IRA providers by requiring investor education before account setup. Instead of high-pressure sales tactics, Augusta uses a slower, education-first onboarding process designed for investors with larger retirement balances who prioritize long-term capital preservation over short-term speculation.

Last updated: January 2026

Key Takeaways

• Mandatory educational webinar attendance before account setup filters out speculative buyers

• $50,000 minimum investment targets serious investors with substantial retirement capital

• Lower transaction volume, higher account values compared to competitors chasing quantity

• Education-first model may not suit investors preferring immediate transactions or self-directed research

Understanding the Education-First Precious Metals Model

The precious metals IRA industry typically operates on volume-based sales models. Representatives contact potential investors, present product offerings, and aim to close transactions quickly. Commission structures reward speed and quantity over extended educational engagement.

This model operates under a different framework. The company requires prospective investors to complete educational materials and attend informational sessions before opening accounts. This approach deliberately slows the sales process while filtering prospects based on investment readiness and financial capacity.

Why This Question Keeps Coming Up

Federal employees, engineers, health workers and high-net-worth retirees encounter precious metals investment pitches through multiple channels—retirement seminars, direct mail campaigns, radio advertisements, and online marketing. Understanding why certain firms emphasize education over immediate sales helps investors evaluate which approach aligns with their decision-making preferences and risk tolerance.

The Mandatory Education Requirement

Before opening accounts, prospective investors must attend a comprehensive webinar covering precious metals fundamentals, IRA regulations, market dynamics, and risk factors. This requirement applies universally regardless of investor experience or account size.

The webinar content addresses:

- IRS rules for precious metals in retirement accounts

- Storage and custodianship requirements

- Historical price patterns and volatility

- Fee structures and total cost analysis

- Liquidity considerations and exit strategies

Augusta's education sessions are conducted by an in-house analyst who leads one-on-one web conferences focused on economic context, inflation considerations, and the mechanics of gold and silver within retirement accounts. The emphasis is on explanation and decision clarity, not sales presentation or market predictions. Public materials sometimes note the analyst's academic background; however, Augusta PM is not affiliated with any university and positions these sessions as educational rather than credential-driven.

This educational mandate serves multiple purposes. It ensures investors understand product characteristics before commitment. It establishes realistic expectations about precious metals as long-term holdings rather than short-term trades. It also screens out prospects seeking quick transactions without comprehensive understanding.

Information Delivery vs. Sales Pressure

The educational sessions maintain informational focus rather than promotional emphasis. Presenters explain precious metals characteristics, regulatory frameworks, and market contexts without employing urgency tactics or limited-time offers.

This approach contrasts with high-pressure sales environments where representatives create artificial scarcity or deadline-driven decisions. Investors receive information, then decide independently whether precious metals IRAs align with their retirement strategies.

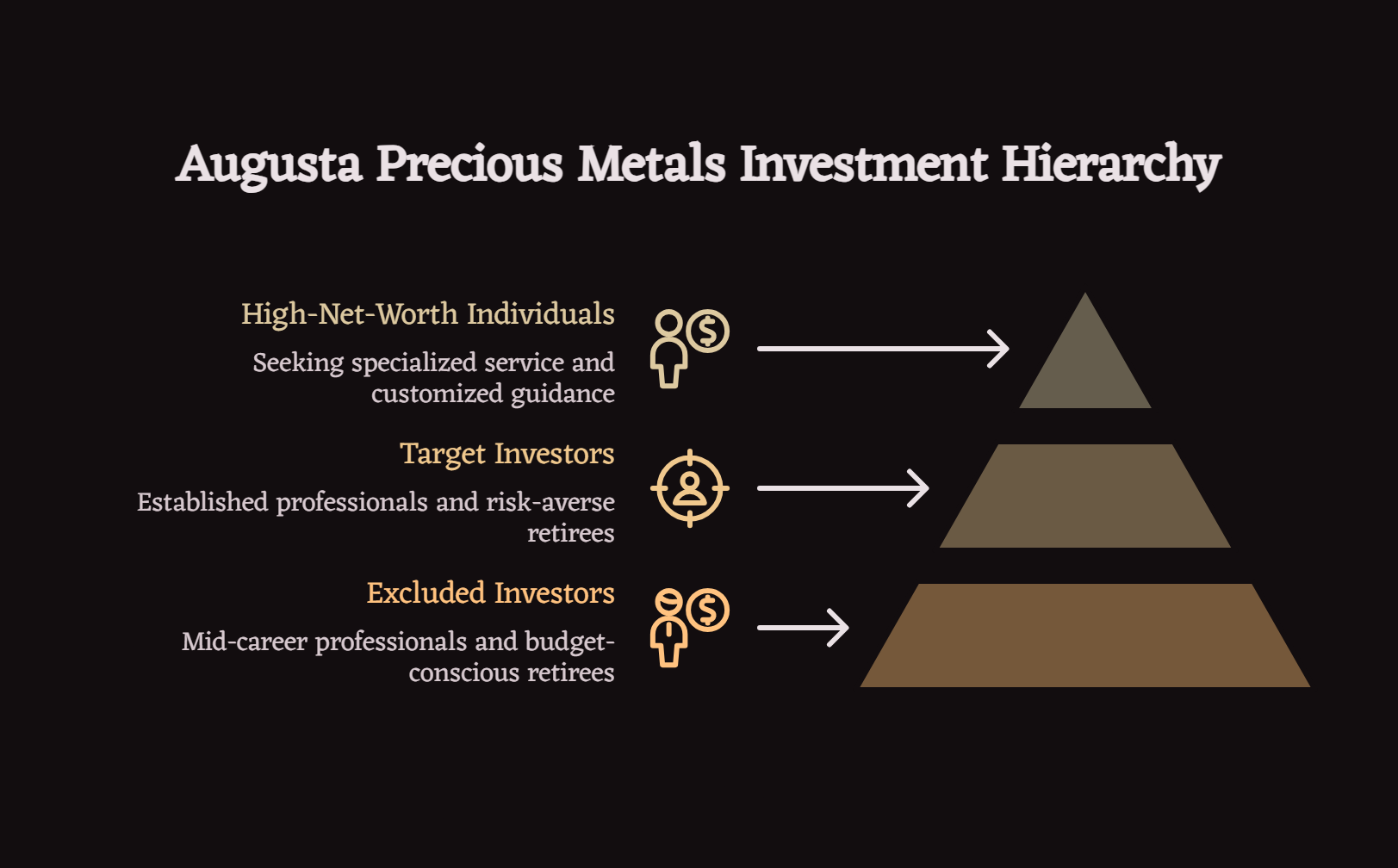

The $50,000 Minimum Investment Threshold

The company establishes a $50,000 minimum for new gold IRA accounts—significantly higher than industry averages ranging from $10,000-$25,000. This threshold targets investors with substantial retirement capital seeking meaningful precious metals allocations.

Economic Rationale Behind Higher Minimums

Higher minimums create specific business dynamics. The education-first model requires significant time investment per prospect—comprehensive webinars, extended consultations, detailed planning sessions. This approach becomes economically viable primarily with larger account values.

Lower-minimum competitors can profitably serve smaller accounts through higher transaction volume and streamlined processes. The education-intensive model requires different economics, supported by fewer, larger accounts rather than numerous smaller ones.

Who Benefits From Higher Entry Points

The $50,000 threshold appeals to specific investor profiles:

Established professionals with substantial retirement savings seeking meaningful portfolio diversification rather than experimental positions. A $50,000 precious metals allocation represents 10% of a $500,000 retirement portfolio or 5% of $1 million in savings—prudent diversification percentages for conservative investors.

Risk-averse retirees prioritizing capital preservation who value extensive education before major financial decisions. These investors appreciate thorough explanation and consultation rather than quick transactions.

High-net-worth individuals seeking specialized service who expect detailed attention and customized guidance commensurate with their investment size.

Who This Threshold Excludes

The minimum requirement automatically excludes several investor categories:

Mid-career professionals with $10,000-$25,000 available for initial precious metals exposure. These investors—whether federal employees with 5-10 years of service or private sector workers building retirement savings—may prefer lower-minimum competitors such as Birch Gold Group and Noble Gold offering entry-level access to gold IRAs.

Investors building positions incrementally through smaller initial investments and regular additions over time. The education model doesn't accommodate gradual accumulation strategies as effectively as transaction-focused competitors.

Budget-conscious retirees seeking minimal precious metals exposure as portfolio insurance. For these investors, $10,000-$15,000 allocations may represent their comfort level, making the $50,000 minimum prohibitive.

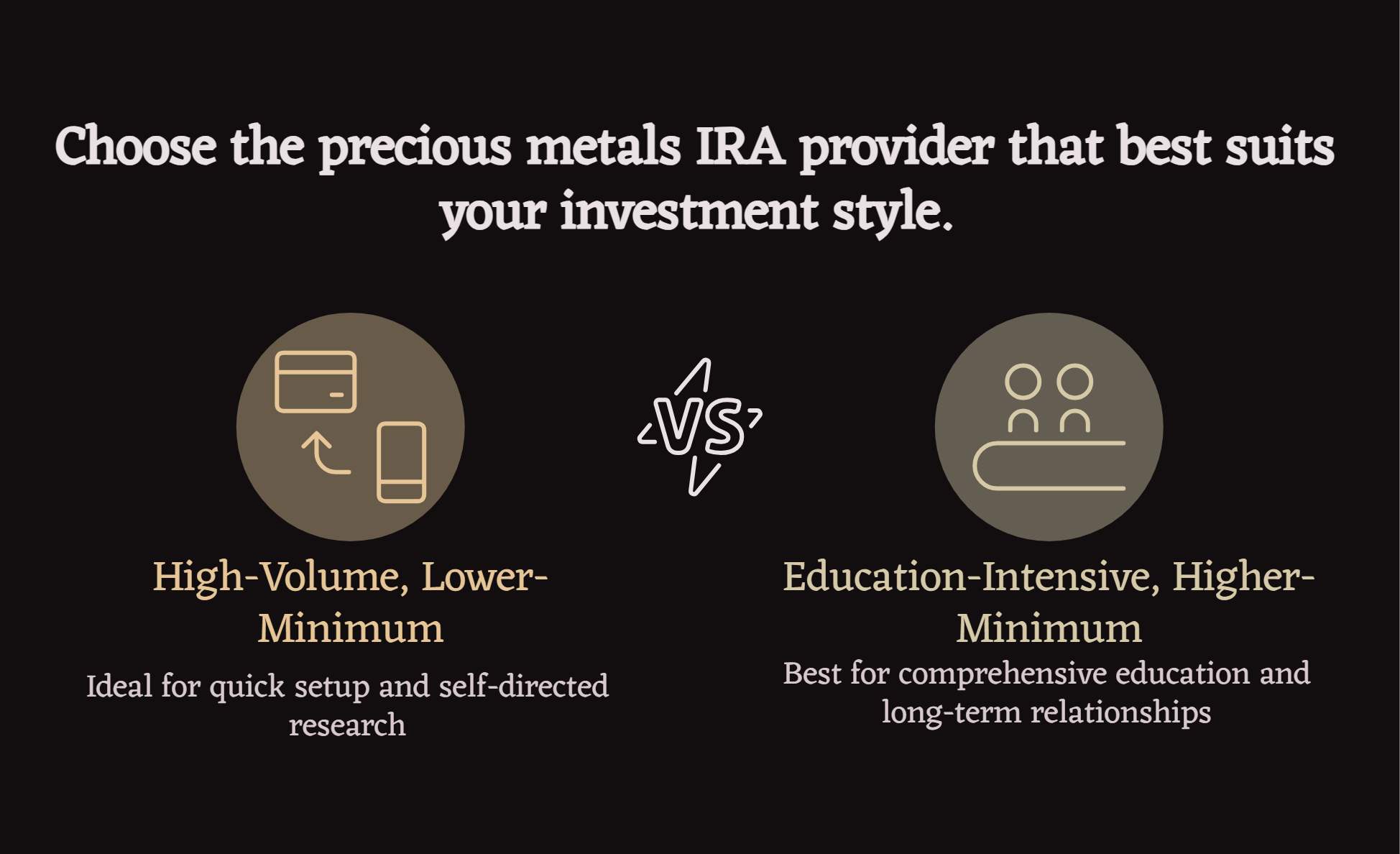

Volume vs. Value: Comparing Business Models

The precious metals IRA industry contains providers operating under fundamentally different business philosophies. Understanding these distinctions helps investors select firms matching their preferences.

High-Volume, Lower-Minimum Providers

Many industry participants pursue volume-based strategies:

- Minimum investments: $10,000-$25,000

- Streamlined onboarding processes

- Limited educational requirements

- Higher transaction frequency per representative

- Broader market reach across investor demographics

This model serves investors preferring:

- Quick account setup

- Self-directed research and decision-making

- Lower entry thresholds for testing precious metals

- Minimal consultation and advisory interaction

Education-Intensive, Higher-Minimum Model

The alternative approach emphasizes depth over breadth:

- Minimum investments: $50,000+

- Mandatory educational participation

- Extended consultation periods

- Lower transaction volume per representative

- Narrower focus on high-net-worth investors

This model serves investors valuing:

- Comprehensive pre-purchase education

- Extensive consultation and planning

- Detailed risk disclosure and expectation setting

- Longer-term relationship development

Neither model is inherently superior. They serve different investor preferences, risk tolerances, and decision-making styles.

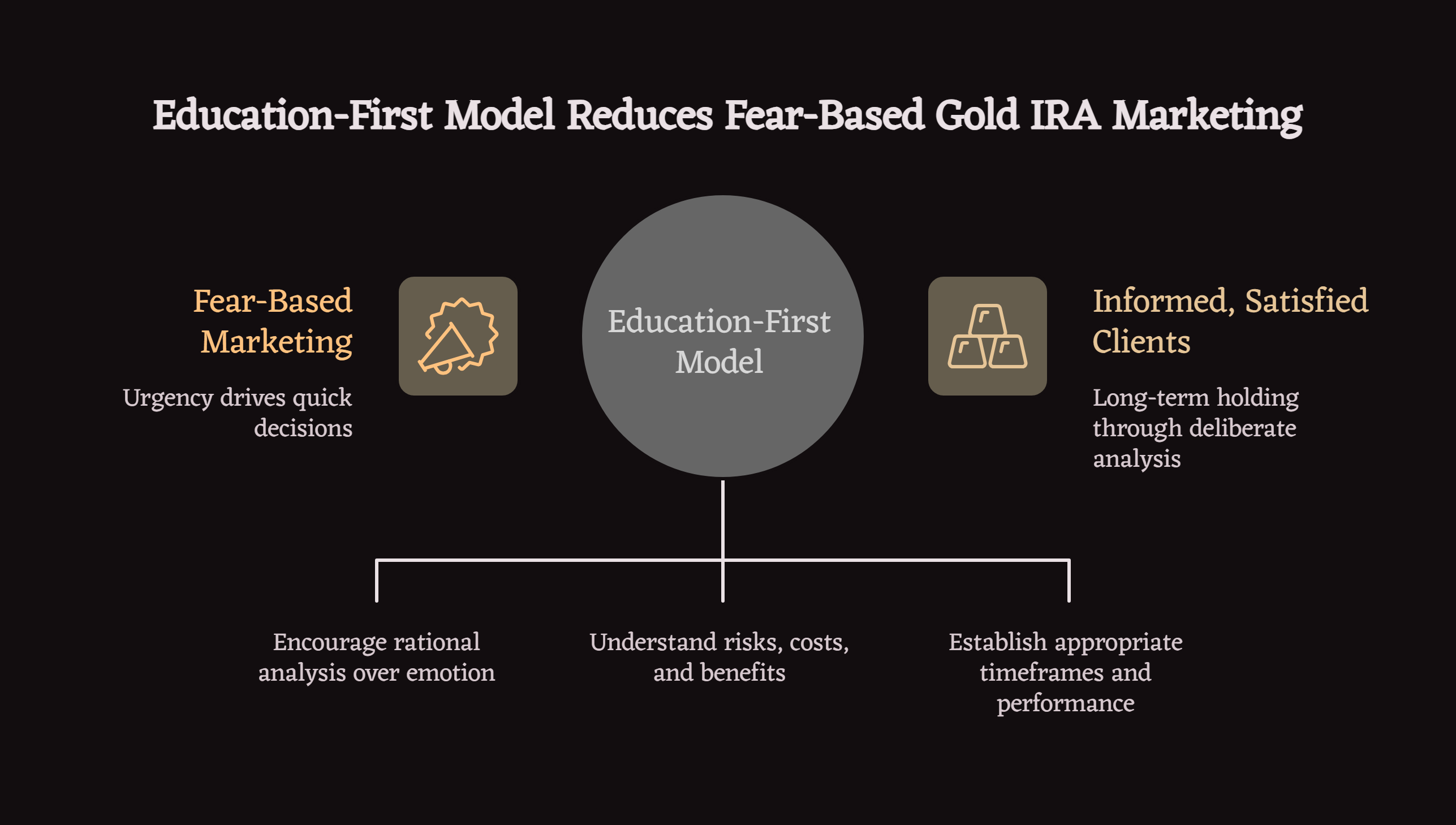

The "Fear Funnel" Problem in Precious Metals Marketing

Many precious metals firms employ fear-based marketing emphasizing economic collapse, currency devaluation, and market crashes. These messages create urgency driving quick purchasing decisions before thorough analysis.

This marketing approach—often called the "fear funnel"—works effectively for volume generation. Frightened investors make faster decisions with less price sensitivity. However, this strategy often produces buyer's remorse, customer dissatisfaction, and high complaint rates when emotional urgency fades post-purchase.

Education as Fear Antidote

The education-first model attempts counteracting fear-driven decision-making. By requiring investors to complete educational programs before purchasing, the approach encourages rational analysis over emotional reactions.

Educated investors understand:

- Precious metals serve as portfolio diversification, not panic responses

- Historical price patterns include both appreciation and depreciation

- Physical metals lack yield or dividends, offering different benefits than income-producing assets

- Reasonable allocation percentages for different risk profiles

This educational grounding theoretically produces more satisfied long-term clients who entered positions through informed analysis rather than fear-based impulses.

Trade-Offs of the Education-First Approach

Advantages

Informed decision-making: Investors understand product characteristics, risks, and costs before commitment.

Realistic expectations: Education establishes appropriate timeframes and performance expectations, reducing disappointment.

Lower complaint rates: Thoroughly educated investors less frequently express dissatisfaction with purchases they comprehensively understood beforehand.

Better client retention: Investors who chose precious metals through deliberate analysis rather than emotional urgency tend toward longer holding periods.

Regulatory compliance: Extensive documentation of educational delivery and informed consent provides protection against regulatory scrutiny.

Disadvantages

Time requirements: Mandatory education extends the purchasing process from days to weeks.

Higher minimums: The $50,000 threshold excludes investors with smaller available capital.

Limited flexibility: Investors preferring quick transactions find the mandatory education process frustrating.

Paternalistic approach: Some sophisticated investors resent required education, viewing it as unnecessary hand-holding.

Reduced market size: Filtering prospects through education and high minimums dramatically shrinks the addressable customer base compared to volume-focused competitors.

Who This Model Serves Best

Ideal Investor Profiles

Pre-retirees with $500K-$2M in retirement savings seeking to diversify 5-15% into precious metals. These investors have sufficient capital to meet minimums while maintaining diversified portfolios.

Risk-averse professionals valuing thorough analysis before major financial decisions. Engineers, physicians, and business executives often appreciate comprehensive education matching their analytical decision-making styles.

Investors burned by high-pressure sales in other contexts. Those with negative experiences from aggressive timeshare presentations or financial product sales particularly value low-pressure, education-focused approaches.

Retirement investors prioritizing capital preservation over growth. Individuals approaching or in retirement, focused on protecting accumulated wealth rather than aggressive appreciation, align well with precious metals' preservation characteristics.

Investors evaluating where precious metals fit within a broader six- or seven-figure portfolio may benefit from reviewing a full breakdown of gold IRAs for high-net-worth retirement portfolios, including allocation ranges, risk trade-offs, and structural considerations.

Poor-Fit Investor Profiles

Younger investors building positions gradually through smaller regular investments. The high minimum and comprehensive education don't accommodate incremental accumulation strategies.

Experienced precious metals investors seeking efficient transactions without mandatory educational programs. These investors view required webinars as unnecessary obstacles.

Budget-conscious investors seeking minimal exposure to test precious metals before larger commitments. The $50,000 minimum prevents experimental small-position entries.

Action-oriented investors preferring quick decisions without extended educational requirements. Some investors research independently and want immediate transaction capability.

Regulatory Considerations and Consumer Protection

CFTC and FTC Oversight

The Commodity Futures Trading Commission and Federal Trade Commission actively monitor precious metals industry practices. Both agencies have prosecuted firms for:

- Misrepresenting profit potential

- Employing high-pressure sales tactics

- Failing to disclose fees and risks adequately

- Making unrealistic price predictions

The education-first model potentially provides stronger regulatory protection by:

- Documenting comprehensive risk disclosure

- Creating extensive paper trails of informed investor consent

- Demonstrating non-coercive sales practices

- Establishing realistic expectation frameworks

State Securities Regulators

State-level securities and consumer protection agencies also oversee precious metals transactions within their jurisdictions. Firms emphasizing thorough education and documentation generally experience fewer regulatory complaints and enforcement actions.

Cost Structures and Fee Transparency

Regardless of business model, precious metals IRAs involve specific fee categories:

Account setup fees: One-time charges for establishing self-directed IRA accounts, typically $50-$300.

Annual custodial fees: Charges for IRA administration and record-keeping, typically $75-$300 annually.

Storage fees: Charges for secure vault storage at IRS-approved depositories, typically $100-$300 annually depending on segregated vs. commingled storage.

Dealer spreads: Markup over spot price when purchasing metals, typically 5-15% for common bullion products.

Education-focused providers generally maintain fee structures comparable to industry standards. The primary cost difference stems from minimum investment requirements rather than per-dollar fee percentages.

Alternative Approaches for Different Investors

For Investors Below the $50,000 Minimum

Lower-minimum competitors: Numerous reputable precious metals IRA firms accept $10,000-$25,000 minimums with straightforward processes.

Precious metals ETFs: Funds like GLD and SLV provide exposure without storage complexity or high minimums, trading like stocks in regular IRAs with expense ratios of 0.10-0.18%.

Direct bullion purchases: Buying physical metals outside IRA structures for home storage or private vault arrangements.

For Self-Directed Researchers

Transaction-focused firms: Companies offering streamlined processes for experienced investors who've completed independent research.

Online precious metals dealers: Firms providing competitive pricing with minimal consultation for knowledgeable buyers.

For Those Seeking Middle-Ground Approaches

Firms offering optional education: Some companies provide educational resources without making them mandatory prerequisites.

Fee-only precious metals advisors: Independent consultants offering education and guidance without product sales.

Making an Informed Decision

Selecting a precious metals IRA provider requires understanding your preferences, circumstances, and priorities:

If you value comprehensive education and consultation before major financial decisions, and meet the $50,000 minimum, education-first models may align well with your decision-making style.

If you prefer efficient transactions after independent research, or have less than $50,000 available, volume-oriented firms with lower minimums better serve your needs.

If you're uncertain about precious metals allocation, consider starting with ETF exposure in existing IRAs before committing to physical metals' higher costs and complexity.

The choice depends on individual circumstances rather than one approach being universally superior. Understanding what you value in the purchasing process—speed versus education, efficiency versus consultation, independence versus guidance—helps identify providers matching your preferences.

Investors evaluating whether an education-first precious metals model aligns with their retirement strategy can review Augusta's public educational materials and onboarding process before making any commitment.

Investors seeking a deeper operational breakdown can review a detailed Augusta Precious Metals analysis covering onboarding process, fees, storage partners, and long-term account support.

Disclaimer: This article provides educational analysis of different precious metals IRA business models and does not constitute financial advice or specific provider recommendations. Investors should conduct independent research and consult qualified financial professionals before making retirement account decisions. Investment choices involve individual circumstances including risk tolerance, time horizons, and financial objectives.

References

[1] Commodity Futures Trading Commission. "Customer Advisory: Precious Metals Fraud." CFTC.gov.

[2] Federal Trade Commission. "Investing in Gold." Consumer Information. FTC.gov.

[3] Internal Revenue Service. "IRC Section 408(m) - Precious Metals in IRAs." IRS.gov.

[4] FINRA. "Buying Physical Gold or Other Metals for Your Retirement Account." Investor Insights.

[5] Better Business Bureau. "Gold IRA Companies: Tips for Consumers." BBB.org.

[6] Investopedia. "Gold IRA: What It Is and How It Works." Updated 2025.

[7] Consumer Financial Protection Bureau. "What to know before investing in precious metals." CFPB.gov.