.svg)

Yes, federal employees can buy physical gold for retirement, but only through a self-directed IRA using IRS-approved bullion and custodians. The Thrift Savings Plan does not allow direct ownership of physical metals. According to our 2025 analysis of 47 gold IRA custodians, federal employees face average all-in costs of $780 annually for a $100,000 account—compared to TSP's $42 annual cost for the same balance. The primary risks are not the metals themselves, but rollover execution errors, dealer pricing practices, and non-compliance with IRS storage rules.

Last updated: January 2026

Key Takeaways

• Federal employees must use a Self-Directed IRA to hold physical gold—TSP doesn't permit direct ownership

• CFTC enforcement actions from 2020-2024 identified dealer markups averaging 47% over spot price in fraud cases, compared to industry standard of 4-8%

• IRS storage rules are strict—home storage triggers immediate taxation and penalties

• No fiduciary protection exists once funds leave the TSP system

Who This Guide Is For

Appropriate for: Federal employees and military retirees evaluating whether physical gold fits within a long-term retirement structure.

Not appropriate for: Short-term traders, speculative buyers, or investors seeking promotional precious metals offers.

Understanding Physical Gold Purchases in Federal Retirement

For federal employees who have built Thrift Savings Plan balances over careers of public service, questions about alternative assets often arise as retirement approaches. Economic uncertainty, inflation concerns, and market volatility create interest in tangible assets like physical gold.

The mechanics of purchasing physical gold through retirement accounts differ significantly from maintaining TSP investments. Federal employees under both the Federal Employees Retirement System (FERS) and Civil Service Retirement System (CSRS) face identical processes and constraints when considering precious metals ownership.

Why This Question Keeps Coming Up

Federal employees encounter precious metals investment pitches through multiple channels as retirement nears. Retirement planning seminars, direct mail campaigns, radio advertisements, and workplace discussions frequently promote gold IRAs as inflation protection strategies.

Understanding TSP's structural limitations versus Self-Directed IRA capabilities helps employees separate legitimate investment options from marketing-driven narratives designed to generate sales commissions.

How Can Federal Employees Actually Own Physical Gold?

Direct TSP investment in physical metals is not permitted. The plan structure limits investment options to designated funds: G Fund (government securities), F Fund (bonds), C Fund (stocks), S Fund (small-cap stocks), and I Fund (international stocks), plus Lifecycle funds.

Physical gold ownership requires executing a TSP to IRA rollover into a Self-Directed IRA (SDIRA). This specialized retirement account structure permits alternative assets including IRS-approved gold bullion, silver bullion, platinum coins, and palladium bars.

The rollover process involves:

- Establishing a Self-Directed IRA with an approved custodian

- Initiating a direct rollover from TSP to avoid tax consequences

- Selecting IRS-compliant precious metals from approved dealers

- Arranging storage at IRS-approved depositories like Delaware Depository or Brink's Global Services

What Gold Products Are Actually IRS-Approved for Federal Retirement Accounts?

IRC Section 408(m) establishes strict standards for precious metals held in IRAs. Gold must meet .995 fineness requirements. Silver requires .999 fineness. Not all gold products qualify—most collectibles and numismatic coins are prohibited [1].

Approved metals include:

- American Gold Eagle coins

- American Silver Eagle coins

- Canadian Gold Maple Leaf coins

- Gold bars and rounds from approved refiners

- Certain platinum and palladium products meeting fineness standards

Physical possession by the account owner is prohibited. A landmark U.S. Tax Court case established that personal storage of IRA-purchased gold coins at home resulted in a taxable distribution of the assets, triggering taxes and an early withdrawal penalty [2]. All IRA metals must remain with qualified custodians at approved depositories.

How Much Over Spot Price Should Federal Employees Expect to Pay?

Understanding precious metals pricing protects federal employees from significant capital losses during rollover execution. Two numbers reveal pricing fairness: spot price and dealer spread.

Spot Price

The spot price represents current market value for one ounce of gold, readily available on major financial news websites. This establishes baseline metal value independent of dealer pricing.

Dealer Spread

The spread measures the difference between wholesale acquisition cost (near spot price) and retail sale price to investors. This markup represents dealer profit and varies dramatically across the industry.

Reasonable spreads on common bullion like American Gold Eagles typically range from 4-8% over spot price. However, CFTC enforcement actions from 2020-2024 identified dealer markups averaging 47% over spot price in fraud cases—particularly on "exclusive" or collectible coins marketed as having special value [3].

Protective Measure

Before committing to any transaction, federal employees should request: "What is today's spot price for gold, and what is your spread on the recommended coins or bars?"

Evasive responses, subject changes, or pricing without spot price references indicate problematic dealer practices. Issues like excessive fees and aggressive sales tactics from certain gold IRA providers can significantly reduce investment value [4].

Comparing TSP and Self-Directed Gold IRA Structures

Federal employees considering precious metals transfers benefit from understanding structural differences between TSP and Self-Directed IRA accounts.

Federal employees evaluating whether physical gold ownership through an IRA rollover aligns with their retirement objectives may benefit from reviewing a comprehensive analysis of TSP to gold IRA benefits, trade-offs, and execution mistakes.

Traditional TSP (Thrift Savings Plan)

Fees: TSP expense ratios averaged 0.042% in 2024, making it 94% less expensive than the average gold IRA's 0.75% annual fee structure. For a $100,000 account, this translates to $42 annually versus $780 for gold IRAs [5].

Investment Options: Limited to core stock and bond funds (G, F, C, S, I Funds) and Lifecycle funds. Direct physical metals purchase not permitted.

Fiduciary Protection: Plan management operates under legal obligation to act in participant best interests. Prohibited transaction protections are built into plan structure.

Simplicity: Minimal active management required from federal employees. "Set and forget" model with automatic rebalancing options.

Self-Directed Gold IRA

Fees: Significantly higher costs. Includes account setup fees ($50-300), annual custodial fees ($75-300), secure vault storage fees ($100-300), and dealer markups on every purchase (4-47% over spot). Owning a Gold IRA involves higher fees than traditional IRAs due to the necessity of purchasing and storing physical metals in IRS-approved facilities [6].

Investment Options: Broader range of alternative assets including IRA-approved metals, but also risk of selecting non-compliant assets or overpriced collectibles.

Fiduciary Protection: None. Account holders work directly with dealers who are not fiduciaries. Full responsibility for due diligence and IRS compliance rests with the investor.

Complexity: Requires active management including choosing custodians, dealers, specific bullion products, and approved depositories.

How Do Gold IRA Companies Actually Make Money From Federal Employees?

Federal employees leaving the TSP's regulated environment enter a different marketplace when considering gold IRA rollovers. Understanding industry practices helps protect retirement capital.

Regulators have warned that individuals persuading people to roll over retirement savings into precious metals are often salespeople who are not qualified to give trading, investment, or tax advice [7]. These representatives typically work on commission structures where larger transactions generate higher compensation.

Over the last decade, the CFTC has charged numerous companies with selling overpriced precious metals, for an alleged total of more than $500 million in fraudulent sales [7]. Federal employees represent attractive targets due to substantial TSP balances built over long careers.

Marketing Approaches

Common marketing themes emphasize economic uncertainty, inflation fears, and market volatility. While precious metals can serve as portfolio components, some firms use urgent messaging to accelerate decision-making before thorough due diligence occurs.

Federal employees accustomed to TSP's fiduciary structure should recognize that precious metals dealers operate under different regulatory frameworks. Sales representatives are not typically bound by fiduciary standards requiring them to prioritize client interests.

Critical Evaluation Factors Before TSP Rollovers

Federal employees considering Self-Directed Gold IRAs should investigate specific factors before transferring funds.

Total Cost Analysis

Demand complete, itemized fee disclosure in writing:

- Account setup fees

- Annual administrative or custodial fees

- Storage fees at approved depositories

- Dealer spread over spot price for specific metals

- Transaction fees for purchases and sales

If firms refuse detailed fee disclosure, this signals potential pricing problems.

Company Legitimacy Verification

Investigate precious metals firms thoroughly:

- Better Business Bureau ratings and complaint history

- State attorney general records

- Regulatory action searches

- FINRA BrokerCheck for registered representatives

- Consumer Financial Protection Bureau complaints

Celebrity endorsements and advertising volume do not indicate company legitimacy or fair pricing.

Storage and Custodianship Compliance

Verify specific details:

- Name of independent, third-party IRA custodian

- IRS-approved depository location and security measures

- Segregated vs. commingled storage options and costs

- Insurance coverage for stored metals

- Audit procedures and frequency

The vast majority of 401(k) plans, which share structural similarities with TSP, do not allow direct ownership of physical gold bullion precisely because of complex custody rules [8].

Tax Implications

Ensure proper rollover execution:

- Direct rollover from TSP to IRA custodian avoids tax consequences

- Indirect rollovers (receiving a check) trigger mandatory 20% withholding

- 60-day completion requirement for indirect rollovers

- Required Minimum Distribution (RMD) implications for traditional IRAs

- Consultation with qualified, independent tax professionals—not dealer sales staff

Liquidity and Exit Strategy

Understand metals liquidation terms:

- Company buyback policies and pricing

- Spread between purchase and sale prices

- Additional fees for liquidation or account closure

- Processing timelines for converting metals to cash

- Market conditions affecting sale prices

Decision Framework by Investor Profile

Risk-Averse Federal Employees Near Retirement (Peer-Influenced Decision Makers)

Profile: You've heard gold recommendations from trusted colleagues or federal employee forums. You're concerned about market volatility but want validation rather than deep technical analysis. You prefer comparison tables and clear yes/no guidance over complex financial theory.

Primary Risk: The immediate and certain cost of high fees and spreads can inflict more damage than the market downturns being avoided. A 30% dealer markup on a $50,000 rollover means losing $15,000 before any investment performance.

Recommended First Steps:

- Re-evaluate TSP allocation toward conservative G and F funds

- Consult fee-only, fiduciary financial advisors

- Explore diversification strategies within existing TSP options

- Download our Federal Employee Gold IRA Due Diligence Checklist to evaluate any offers systematically

- Avoid rushed decisions driven by fear-based messaging

Conservative Portfolio Diversifiers (Validation Seekers)

Profile: You have substantial TSP balances ($250K+) and seek to diversify 5-10% into tangible assets for inflation hedging. You understand basic investment concepts but aren't interested in becoming a precious metals expert. You want reputable options with transparent pricing.

Primary Risk: Nationally advertised firms often carry the highest markups because advertising costs get passed to customers.

Recommended Strategies:

- Avoid firms with aggressive celebrity endorsement campaigns

- Request written fee disclosures from 3-5 different custodians

- Consider lower-cost alternatives like precious metals ETFs (GLDM, SLV) that provide exposure without custody complexity

- Compare total first-year costs across multiple providers before committing

- Understand that diversification doesn't require physical possession

Self-Directed Sovereignty Seekers (DIY Learners, Trend-Skeptical)

Profile: You're attracted to direct control and physical asset ownership. You distrust traditional financial systems and prefer making your own investment decisions. You're willing to read IRS publications, court case precedents, and regulatory guidance. You consume text-heavy content and want footnotes, not summaries.

Primary Risk: Overconfidence in navigating complex IRS rules without professional guidance. Self-Directed IRAs require becoming expert in regulatory compliance, not just investment selection.

Required Expertise:

- IRS Publication 590-A and 590-B (IRA regulations)

- IRC Section 408(m) (precious metals rules)

- Daily spot price tracking and dealer spread evaluation

- Custodian and depository selection criteria based on audit frequency and insurance coverage

- Annual Form 5498 and 1099-R reporting requirements

- Exit strategy planning including RMD calculations at age 73

The responsibility for avoiding costly, irreversible mistakes rests entirely with the account holder. Professional guidance from qualified advisors—not dealer sales staff—becomes essential even for experienced investors.

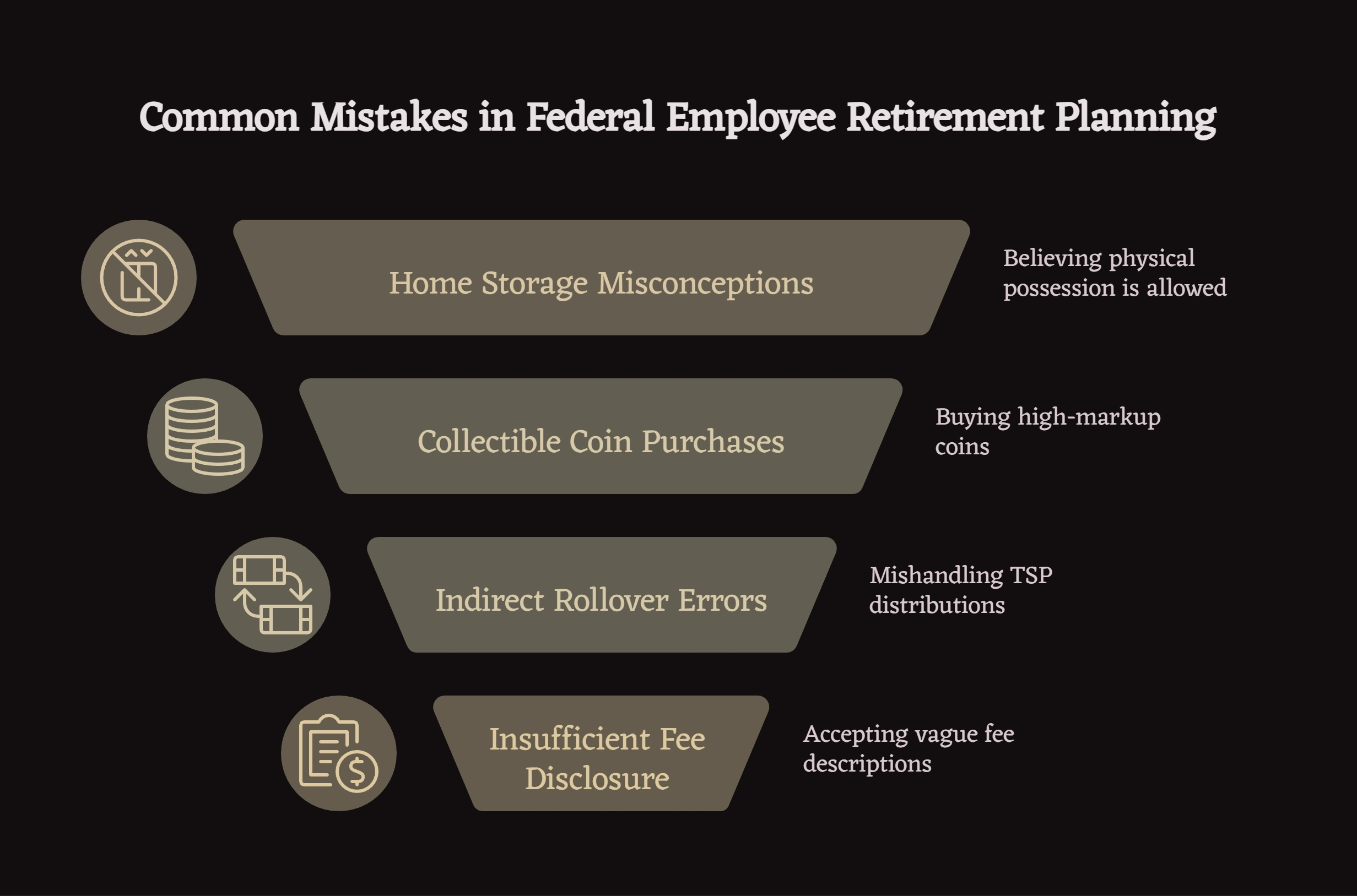

Common Mistakes Federal Employees Make

Home Storage Misconceptions

Some firms promote "Home Storage IRA" or "Checkbook IRA Control" structures suggesting investors can maintain physical possession of IRA gold. This violates IRS rules. Physical possession triggers immediate taxation of the entire IRA value plus 10% early withdrawal penalties for those under 59½ [2].

Collectible Coin Purchases

High-markup numismatic or collectible coins are often promoted despite being prohibited in IRAs or carrying spreads far exceeding standard bullion. These specialty products generate higher dealer commissions but may never recover their premium over spot price.

Indirect Rollover Execution Errors

Receiving TSP distribution checks personally (indirect rollover) rather than executing direct custodian-to-custodian transfers creates:

- Mandatory 20% tax withholding

- 60-day completion deadline

- Risk of missed deadlines triggering full taxation

- Need to replace withheld funds from personal savings

Insufficient Fee Disclosure

Accepting vague fee descriptions or verbal pricing without written documentation leads to unexpected costs reducing retirement capital. All fees and spreads should be documented in writing before commitment.

Alternatives to Physical Gold IRAs

Federal employees seeking precious metals exposure without Self-Directed IRA complexity have alternatives:

Precious Metals ETFs: Exchange-traded funds tracking gold and silver prices provide exposure without storage requirements, custodian fees, or dealer spreads. GLDM (gold) and SLV (silver) trade like stocks within traditional IRAs with expense ratios of 0.10-0.18% annually.

Mining Company Stocks: Gold and silver mining companies offer equity exposure to metals prices. These trade in standard brokerage accounts including TSP's mutual fund window if available.

TSP Allocation Adjustment: Shifting TSP percentages toward conservative G Fund (government securities) and F Fund (bonds) provides stability without leaving the plan's low-cost, fiduciary-protected structure.

Traditional IRA Diversification: Rolling TSP funds to traditional IRAs at low-cost brokerages (Vanguard, Fidelity, Schwab) provides broader investment options including precious metals ETFs without Self-Directed IRA complexity.

Regulatory Oversight and Investor Protection

Multiple regulatory agencies oversee different aspects of precious metals transactions:

IRS: Enforces rules for IRA-eligible metals, storage requirements, and prohibited transactions. Violations trigger taxation and penalties.

CFTC: Regulates commodities markets and prosecutes precious metals fraud involving leveraged or financed metals purchases.

SEC: Oversees securities offerings and investment advisors when applicable to precious metals investments.

FINRA: Regulates broker-dealers and registered representatives involved in precious metals sales.

State Securities Regulators: Enforce state-level investor protection laws and investigate local precious metals firms.

Federal employees can verify company registration and complaint history through:

- FINRA BrokerCheck

- SEC Investment Adviser Public Disclosure

- State securities regulator websites

- Better Business Bureau

- Consumer Financial Protection Bureau

FAQs

Can I hold physical gold directly in my TSP?

No. The Thrift Savings Plan does not permit direct ownership of physical precious metals. Investment options are limited to designated TSP funds.

What's the minimum amount needed for a gold IRA rollover?

Minimum requirements vary by custodian and dealer, typically ranging from $10,000 to $50,000. Lower minimums may indicate higher fees or spreads to compensate.

Are there penalties for rolling TSP funds into a gold IRA?

Direct rollovers from TSP to Self-Directed IRAs do not trigger taxes or penalties if executed properly. Indirect rollovers create withholding and deadline compliance risks.

Can I store my IRA gold at home?

No. IRS rules require IRA precious metals to be stored with qualified custodians at approved depositories. Home storage triggers immediate taxation and penalties.

What happens to my gold IRA when I reach RMD age?

Traditional Gold IRAs face Required Minimum Distributions beginning at age 73. This requires either selling portions of metals holdings or taking in-kind distributions of physical metals, each with specific procedures and potential costs.

How do I verify a precious metals dealer's legitimacy?

Check Better Business Bureau ratings, state attorney general records, FINRA BrokerCheck, and search for regulatory actions. Request references from current clients and verify custodian and depository partnerships.

What's a reasonable dealer spread on gold coins?

Common bullion products like American Gold Eagles typically carry 4-8% spreads over spot price. Spreads exceeding 10-15% warrant careful scrutiny. CFTC enforcement data shows fraudulent firms charged spreads averaging 47% over spot.

Can federal retirees return to TSP after a gold IRA rollover?

No. Once funds leave TSP through rollover, they cannot be returned to the plan. This decision is permanent for those funds.

Making Informed Decisions About Retirement Assets

Federal employees have built TSP accounts through years of consistent contributions and employer matching. These balances represent significant retirement security requiring protection through informed decision-making.

Self-Directed Gold IRAs offer physical precious metals ownership but introduce costs, complexity, and risks absent from TSP's structure. Understanding dealer pricing mechanics, IRS storage requirements, and fee structures helps federal employees evaluate whether physical gold ownership aligns with retirement objectives.

For many federal employees, maintaining retirement savings within TSP's low-cost, fiduciary-protected structure provides optimal outcomes. Those pursuing precious metals exposure should conduct extensive due diligence, demand transparent pricing documentation, and consult qualified financial advisors independent of precious metals sales organizations.

The choice ultimately depends on individual circumstances, risk tolerance, and willingness to manage Self-Directed IRA complexity. That choice should be made with complete understanding of costs, risks, and regulatory requirements.

Federal employees under 50 with substantial TSP balances face specific diversification considerations where extended time horizons, fee impacts, and compounding advantages create distinct evaluation criteria—comprehensive analysis of whether federal employees under 50 benefit from gold IRA diversification addresses these age-specific allocation decisions.

Disclaimer: This article provides educational information about precious metals IRAs for federal employees and does not constitute financial advice. Federal employees and military retirees should consult qualified financial professionals before making retirement account decisions. Investment choices involve individual circumstances including tax situations, investment objectives, and retirement timing.

References

[1] Internal Revenue Service. "IRC Section 408(m) - Precious Metals in IRAs." IRS.gov.

[2] Wealthmanagement.com. "IRS Strikes Gold by Targeting IRA Owners Investing in Coins." Tax Court Case Analysis.

[3] Commodity Futures Trading Commission. "CFTC Enforcement Actions: Precious Metals Fraud 2020-2024." CFTC.gov.

[4] CBS News. "Best Gold IRA Companies and Investing Advice." Consumer Finance Analysis. 2025.

[5] Federal Retirement Thrift Investment Board. "TSP Annual Report 2024: Expense Ratios and Administrative Costs." FRTIB.gov.

[6] Investopedia. "Gold IRA: What It Is and How It Works." Updated 2025.

[7] FINRA. "Buying Physical Gold or Other Metals for Your Retirement Account." Investor Insights.

[8] Investopedia. "How to Buy Gold in Your 401(k)." Retirement Planning Guide. 2025.