.svg)

The TSP G Fund and gold IRAs serve fundamentally different protection functions for federal retirement savings. The G Fund guarantees principal through government-backed securities with a 0.042% expense ratio—costing $42 annually per $100,000. Gold IRAs may hedge against inflation and currency devaluation but carry average fees of $780 per year per $100,000 and price volatility the G Fund doesn't have. Neither option universally outperforms the other. The right allocation depends on whether your primary concern is capital preservation or purchasing power protection.

Last updated: February 2026

Key Takeaways

- The G Fund guarantees principal protection—no market exposure, no loss risk, regardless of economic conditions

- Gold IRAs historically hedge inflation but introduce 15% standard deviation in price volatility absent from G Fund holdings

- Fee differential is significant: G Fund costs $42/year per $100,000 vs. gold IRA average of $780/year—a $738 annual gap that compounds over decades

- Liquidity differs substantially: G Fund allows daily interfund transfers; gold IRA liquidations typically require 7-30 days

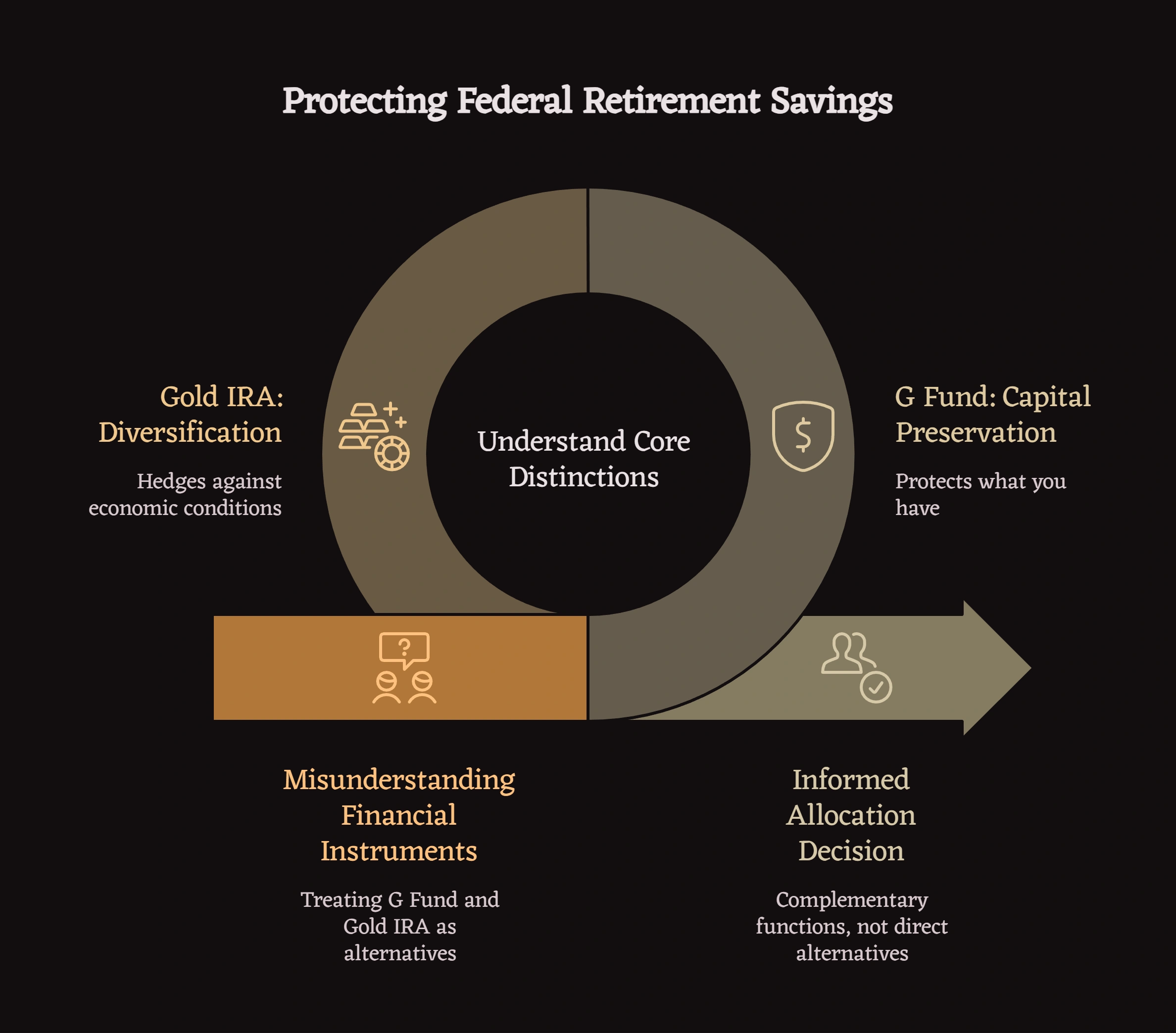

Understanding the Core Distinction

Federal employees evaluating these two options are often comparing fundamentally different financial instruments. The G Fund is a capital preservation vehicle—it protects what you have. Gold IRAs are diversification instruments—they hedge against specific economic conditions that erode purchasing power.

Understanding this distinction prevents the most common mistake: treating them as direct alternatives when they often function as complements.

Why This Question Keeps Coming Up

Federal employees with G Fund allocations increasingly encounter gold IRA marketing through retirement seminars, financial advisor outreach, and peer discussions. Many are analytically minded professionals—engineers, administrators, senior officials—who recognize the G Fund's cost efficiency but question whether it adequately protects against inflation scenarios where purchasing power erodes even as principal stays intact.

This comparison addresses that specific concern with data rather than promotional framing.

How Does the G Fund Actually Work?

The TSP G Fund invests exclusively in short-term U.S. Treasury securities issued specifically for the TSP by the federal government. This structure provides two unique characteristics unavailable in any private investment:

Principal guarantee: Unlike money market funds or short-term bond funds, the G Fund cannot lose nominal value. The government guarantees both principal and interest regardless of market conditions.

Long-term rate on short-term risk: The G Fund earns interest based on the weighted average yield of all outstanding Treasury notes and bonds with four or more years to maturity—while taking on no duration risk. This creates a return profile unavailable elsewhere.

2024-2025 performance context: G Fund yields tracked between 4.0-4.5% during 2024, reflecting the higher interest rate environment. Projected 2025-2026 yields sit around 3-4% depending on Federal Reserve policy trajectory.

Cost structure: The 0.042% TSP expense ratio translates to $42 annually per $100,000—among the lowest costs of any retirement investment vehicle available to American workers.

The G Fund does not protect against inflation in real terms. If inflation runs at 4% and the G Fund returns 3.5%, purchasing power declines by 0.5% annually despite nominal principal preservation.

How Do Gold IRAs Actually Work Within Retirement Accounts?

Gold IRAs are self-directed IRAs holding IRS-approved physical precious metals rather than securities. They operate under the same contribution and distribution rules as traditional IRAs but with additional compliance requirements governing metal purity, custodianship, and storage.

IRS requirements: Gold must meet .995 fineness (American Gold Eagles are an exception at .9167). Silver requires .999 fineness. All metals must remain with IRS-approved custodians at qualified depositories—personal possession triggers immediate taxable distribution.

Inflation hedge mechanism: Gold historically maintains purchasing power during inflationary periods because its price tends to rise when paper currency loses value. The World Gold Council identifies a historical correlation between gold prices and CPI of approximately 0.6 over multi-decade periods.

Volatility profile: Gold carries a standard deviation of approximately 15% annually compared to the G Fund's 0%. During the 2011-2015 period, gold declined approximately 45% from peak to trough before recovering. During 2022 inflation, gold underperformed many inflation hedge expectations despite surging consumer prices.

Fee structure: Typical annual costs for a $100,000 gold IRA include custodial fees ($75-$300), storage fees ($100-$300), and dealer spreads on purchases (4-8% for legitimate dealers, potentially 30-50% for predatory firms). Total annual ongoing costs average $780 per $100,000.

TSP G Fund vs Gold IRA: Full Comparison

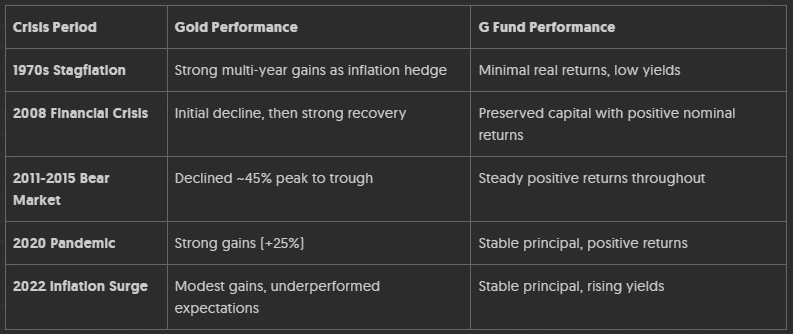

Which Provided Stronger Protection During Historical Crises?

Pattern: G Fund consistently outperforms during deflationary crises and periods of market panic. Gold tends to outperform during sustained inflationary periods but underperforms during sudden crises and deflation.

Neither instrument has provided consistent crisis protection across all economic environments.

How Do Fees Compound Over Time?

The $738 annual fee difference between G Fund ($42) and average gold IRA ($780) per $100,000 compounds significantly over long holding periods.

30-year fee impact on $100,000 (no additional contributions):

- G Fund cumulative fees: approximately $1,260

- Gold IRA cumulative fees: approximately $23,400

- Fee differential: approximately $22,140

This calculation assumes no fee increases and no account growth compounding the fee base. With account growth, the differential widens further because gold IRA fees often scale with account value.

For analytically-minded federal employees, this fee structure means gold prices must outperform G Fund returns by at least 0.74% annually just to break even on costs alone—before accounting for volatility risk.

What Are the Real Risks of Each Option?

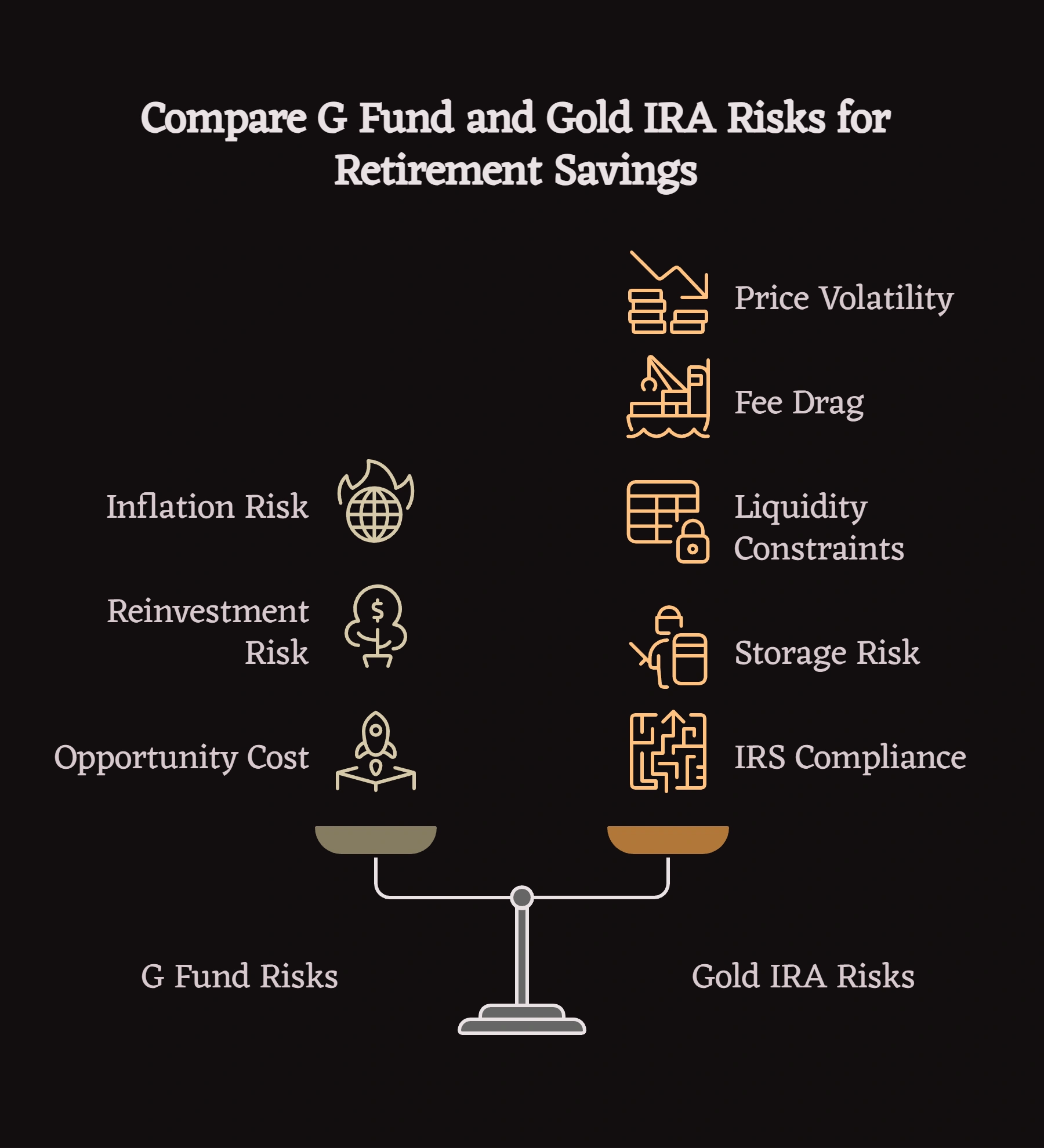

G Fund Risks

Inflation risk: The G Fund's primary vulnerability is purchasing power erosion during sustained high inflation. If inflation consistently exceeds G Fund yields, real retirement wealth declines despite nominal preservation.

Reinvestment risk: If interest rates decline sharply, future G Fund yields fall accordingly. The 4-4.5% yields of 2024 may not persist in lower rate environments.

Opportunity cost: Federal employees who hold large G Fund allocations during extended bull markets forgo equity returns that would have grown retirement wealth substantially.

Gold IRA Risks

Price volatility: Gold's 15% standard deviation means significant short-term losses are entirely possible. Employees who need funds during gold downturns face forced selling at losses.

Fee drag: As detailed above, the $780 annual fee per $100,000 requires meaningful gold appreciation simply to break even versus alternatives.

Liquidity constraints: Selling IRA-held physical gold requires custodian processing, potential shipping, and settlement periods of 7-30 days. Emergency access is not available.

Storage and counterparty risk: Physical gold in depositories involves third-party custody risk absent from G Fund holdings.

IRS compliance complexity: Storage requirement violations, prohibited transaction rules, and metal purity standards create compliance risks not present in TSP management.

Who Might Consider Each Option?

Analytical Savers Favoring G Fund Allocation

Risk-averse federal employees within 5-10 years of retirement who prioritize capital certainty over inflation protection. These professionals—often in senior administrative, legal, or technical roles—have sufficient pension income or other inflation-protected assets that G Fund's stability serves as the appropriate foundation.

Primary concern: Avoiding nominal losses that could delay retirement or reduce standard of living certainty.

Conservative Portfolio Diversifiers Considering Gold IRAs

Federal employees with 15-20+ years to retirement who have maximized TSP contributions and seek to add inflation protection outside the TSP structure. These professionals—often engineers, analysts, or senior technical specialists—understand the fee trade-off and accept gold's volatility in exchange for exposure to a non-correlated asset class.

Primary concern: Purchasing power preservation over multi-decade horizons where inflation's compounding effect on real wealth matters more than short-term volatility.

Poor Fit for Gold IRAs

Federal employees within 5 years of retirement who depend on retirement savings for near-term income should carefully evaluate gold IRA liquidity constraints and volatility before converting G Fund holdings. The combination of potential price declines and 7-30 day liquidation timelines creates meaningful income planning risk.

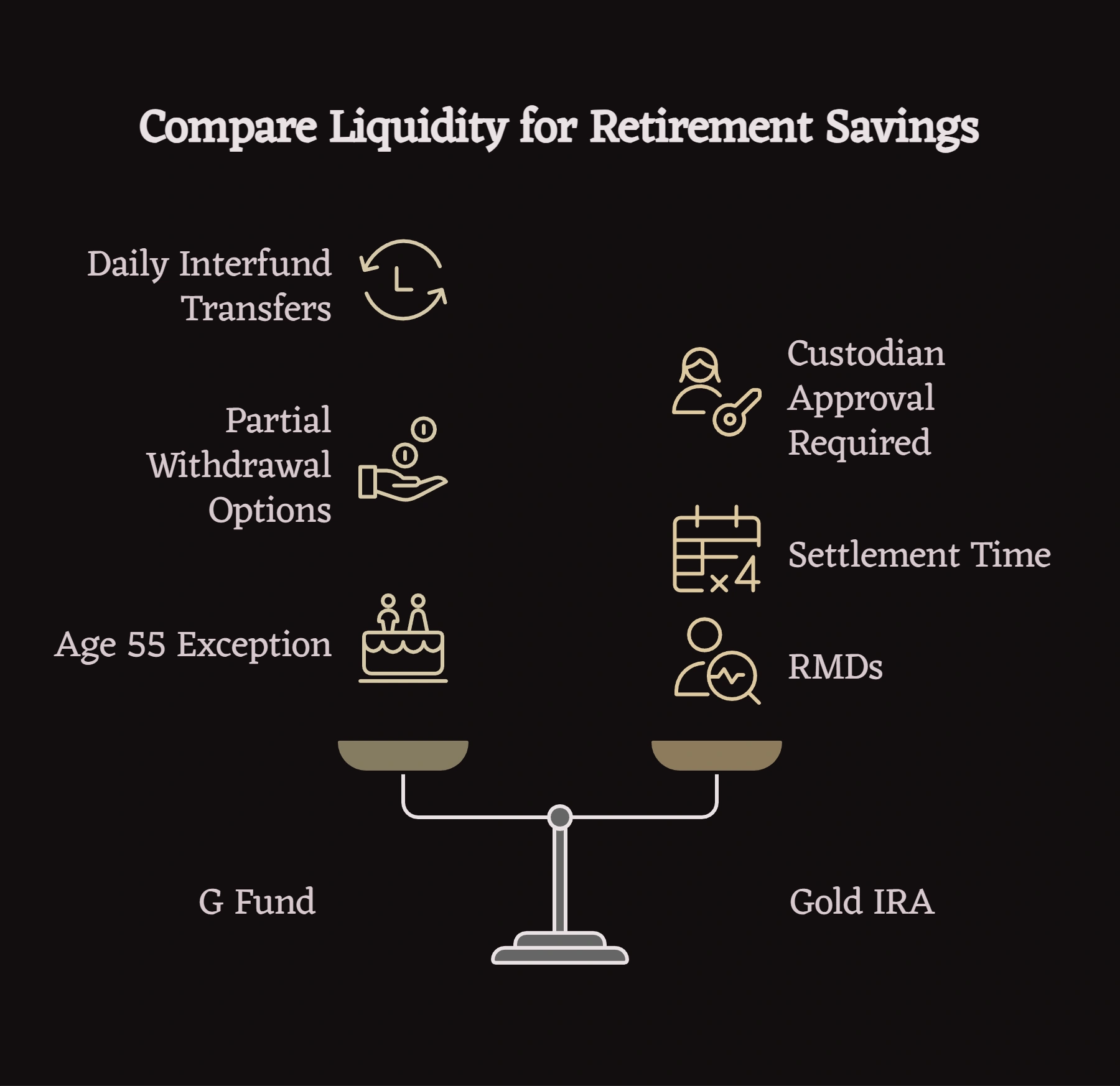

How Do These Options Compare for Liquidity?

Federal employees aged 45-70 face different liquidity needs depending on career stage and separation timing.

G Fund liquidity advantages:

- Daily interfund transfers within TSP at no cost

- Partial withdrawal options post-separation

- Age 55 exception permits penalty-free withdrawals for employees separating at 55 or later

- Required Minimum Distributions begin at 73, calculated separately from IRAs

Gold IRA liquidity constraints:

- Physical gold sales require custodian initiation and approval

- Settlement typically requires 7-30 days including potential shipping

- Bid-ask spreads on gold sales reduce proceeds versus spot price

- RMDs must be satisfied through distributions—gold may need to be liquidated at inopportune prices

For employees who may need access to retirement funds before 59½, the G Fund's liquidity and the age 55 separation exception represent meaningful advantages that gold IRA structures cannot replicate.

Federal employees evaluating how precious metals fit within their broader retirement strategy—including whether TSP rollovers to gold IRAs make sense given their specific timeline and risk profile—may benefit from reviewing a comprehensive analysis of whether rolling a TSP into a gold IRA makes sense for their situation, including pros, cons, and common execution mistakes.

Federal employees evaluating how precious metals fit within their broader retirement strategy—including whether TSP rollovers to gold IRAs make sense given their specific timeline and risk profile—may benefit from reviewing a comprehensive analysis of whether rolling a TSP into a gold IRA makes sense for their situation, including pros, cons, and common execution mistakes.

Making an Informed Allocation Decision

The G Fund vs. gold IRA comparison ultimately reflects two different definitions of "protection":

G Fund protects nominal capital—what you put in stays intact regardless of market conditions.

Gold IRAs aim to protect real purchasing power—what your money can actually buy over time.

Federal employees whose primary retirement concern is avoiding nominal losses will generally find the G Fund better suited to that objective. Those whose primary concern is maintaining purchasing power across decades of potential inflation may find gold IRA exposure worth the fee premium and volatility trade-off.

Many analytically-minded federal employees find that the question isn't "which is better" but rather "what percentage allocation serves my specific risk profile." A modest gold IRA allocation alongside G Fund holdings addresses both concerns without overconcentrating in either approach.

No allocation decision should be made without understanding the complete cost structure, liquidity implications, and IRS compliance requirements of gold IRA management.

Disclaimer: This article provides educational comparison of TSP G Fund and gold IRA characteristics and does not constitute financial, tax, or legal advice. Federal employees should consult qualified financial advisors, tax professionals, and legal counsel before making retirement allocation decisions. Past performance does not predict future results. TSP.gov and IRS.gov provide authoritative guidance on plan rules and precious metals IRA requirements.

References

[1] Federal Retirement Thrift Investment Board. "G Fund: Government Securities Investment Fund." TSP.gov.

[2] Federal Retirement Thrift Investment Board. "TSP Annual Report 2024: Expense Ratios and Fund Performance." FRTIB.gov.

[3] Internal Revenue Service. "IRC Section 408(m): Precious Metals in IRAs." IRS.gov.

[4] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[5] World Gold Council. "Gold as a Strategic Asset: Inflation Correlation Analysis." Gold.org.

[6] U.S. Department of the Treasury. "Treasury Securities and the G Fund Yield Formula." Treasury.gov.

[7] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020-2024." CFTC.gov.

[8] U.S. Tax Court. "McNulty v. Commissioner: IRA Precious Metals Storage Requirements." Tax Court Case Precedent.

[9] Federal Reserve Bank of San Francisco. "Gold as an Inflation Hedge: Historical Analysis." FRBSF.org.

[10] Internal Revenue Service. "Retirement Topics: Required Minimum Distributions." IRS.gov.