.svg)

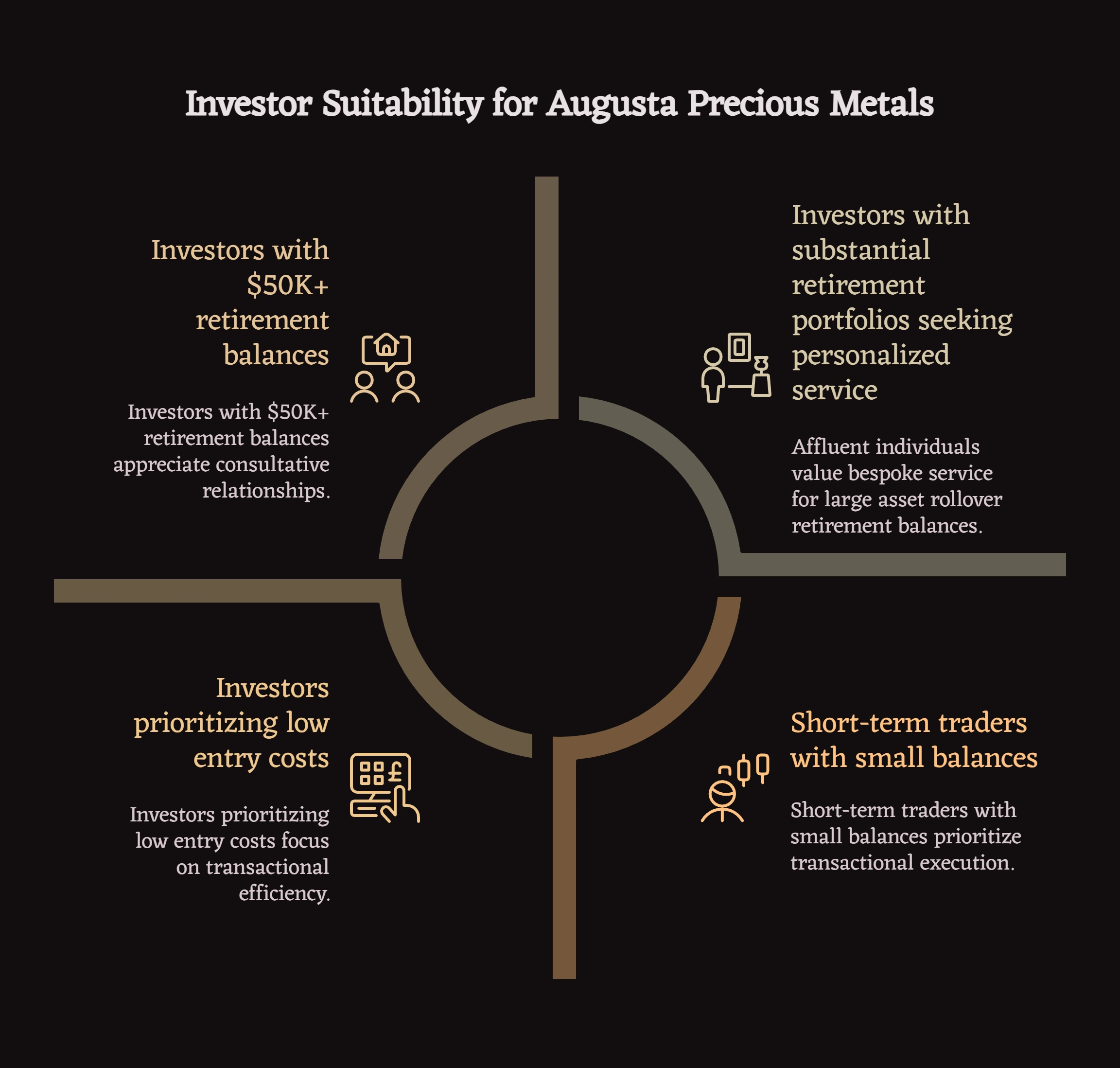

For investors with substantial retirement portfolios, Augusta Precious Metals is often considered a suitable option specifically because of its high minimum investment threshold. This structure functions less as a limitation and more as a deliberate filter that fosters a specialized, education-centric, and high-touch service model designed to mitigate risk and provide a level of personalized guidance that can be essential when protecting a significant nest egg.

Augusta Precious Metals at a Glance

- Best for: Investors with $100K+ retirement balances who value education-focused, white-glove service

- Minimum investment: $50,000 (functions as a filter for serious, long-term investors)

- Service model: Dedicated specialists, lifetime support, one-on-one education with a Harvard-trained analyst

- Product focus: Gold and silver only (intentionally excludes platinum and palladium)

- Not suitable for: Investors with less than $50K, those seeking platinum/palladium, or prioritizing lowest entry costs over service quality

Who this analysis is designed for (and who should look elsewhere)

This analysis focuses on Augusta’s suitability for investors with substantial IRA or 401(k) balances, not short-term trading or speculative allocation strategies.

This guide is designed for: - Investors with retirement balances of $100K+ considering precious metals allocation - High-net-worth individuals prioritizing education and personalized service - Those seeking a consultative relationship rather than transactional execution - Investors who value transparency and lifetime account support

This guide is NOT designed for: - Investors starting with less than $50,000 - Those seeking platinum or palladium IRA options (Augusta offers gold and silver only) - Individuals prioritizing the lowest possible entry costs above service quality - Short-term traders or speculators in precious metals markets

For a broader framework on how gold IRAs function at higher portfolio levels, see our complete guide to gold IRAs for substantial retirement portfolios.

The High-Stakes Question for Affluent Retirees

As we navigate the economic landscape going into 2026, the question of how to protect a large retirement account with gold and other precious metals has moved from a niche concern to a central theme in sophisticated retirement planning. For those who have spent a lifetime building a nest egg of six or seven figures, the goal shifts from aggressive growth to strategic wealth preservation. This is where diversifying a 7-figure portfolio with precious metals comes into focus, offering an approach historically discussed as a hedge against the very forces—inflation, market volatility, and currency devaluation—that pose the greatest threat to a large accumulation of assets.

Gold IRAs have historically been discussed as a hedge against inflation and economic uncertainty, offering portfolio diversification, making them a consideration for this purpose. However, the path to setting up a large self-directed IRA with precious metals is filled with choices, and not all providers are created equal. This brings us to a critical decision point for affluent retirees and high-net-worth individuals: the choice of a partner company. Among the most discussed names in the industry is Augusta Precious Metals. But a common question arises immediately: is Augusta Precious Metals good for a large 401k rollover, especially given its significant minimum investment? This article provides a comprehensive cost-benefit analysis of Augusta for large accounts, examining how its high barrier to entry functions as part of its service model.

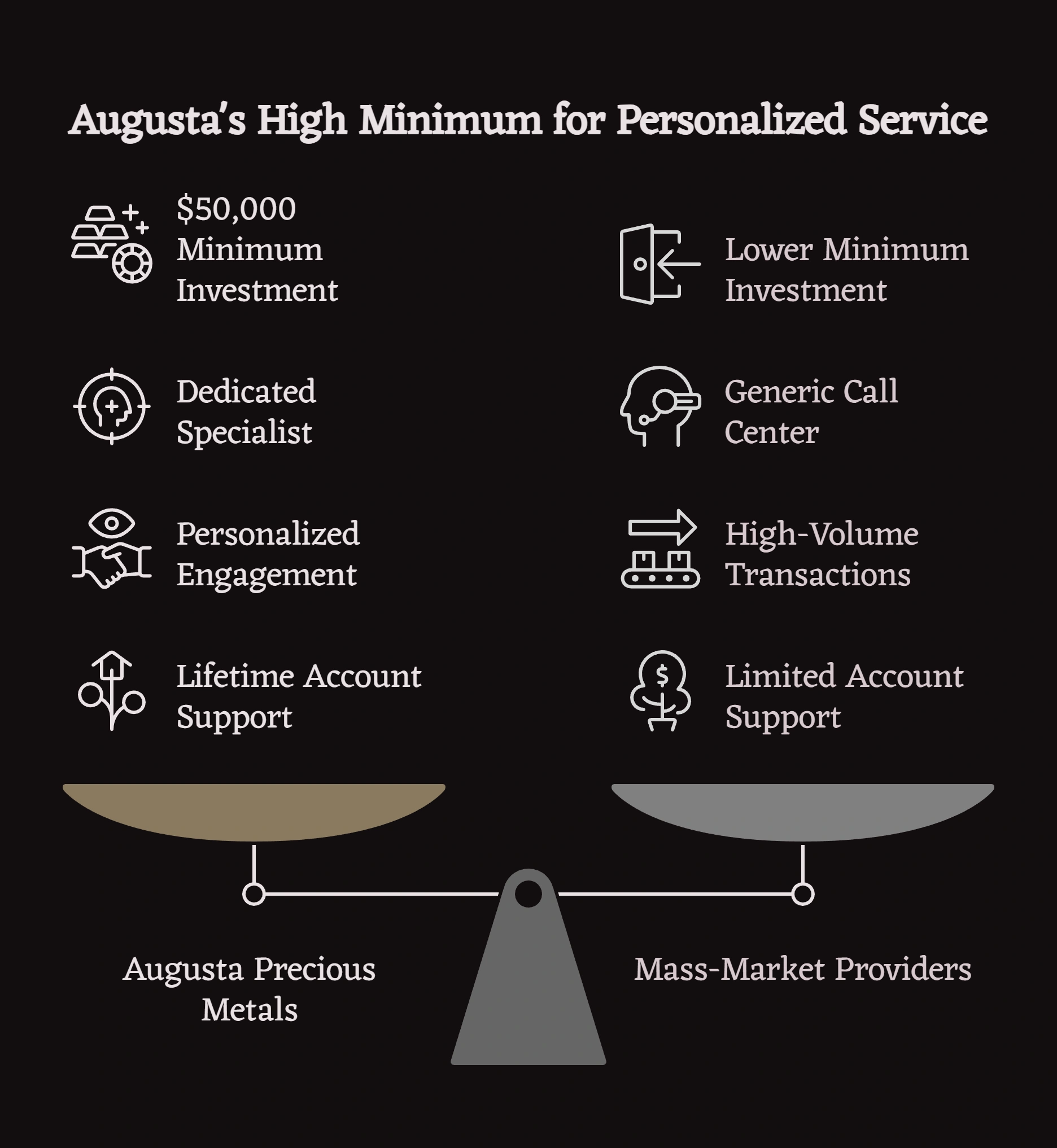

The $50k Minimum: A Deliberate Filter for a Bespoke Experience

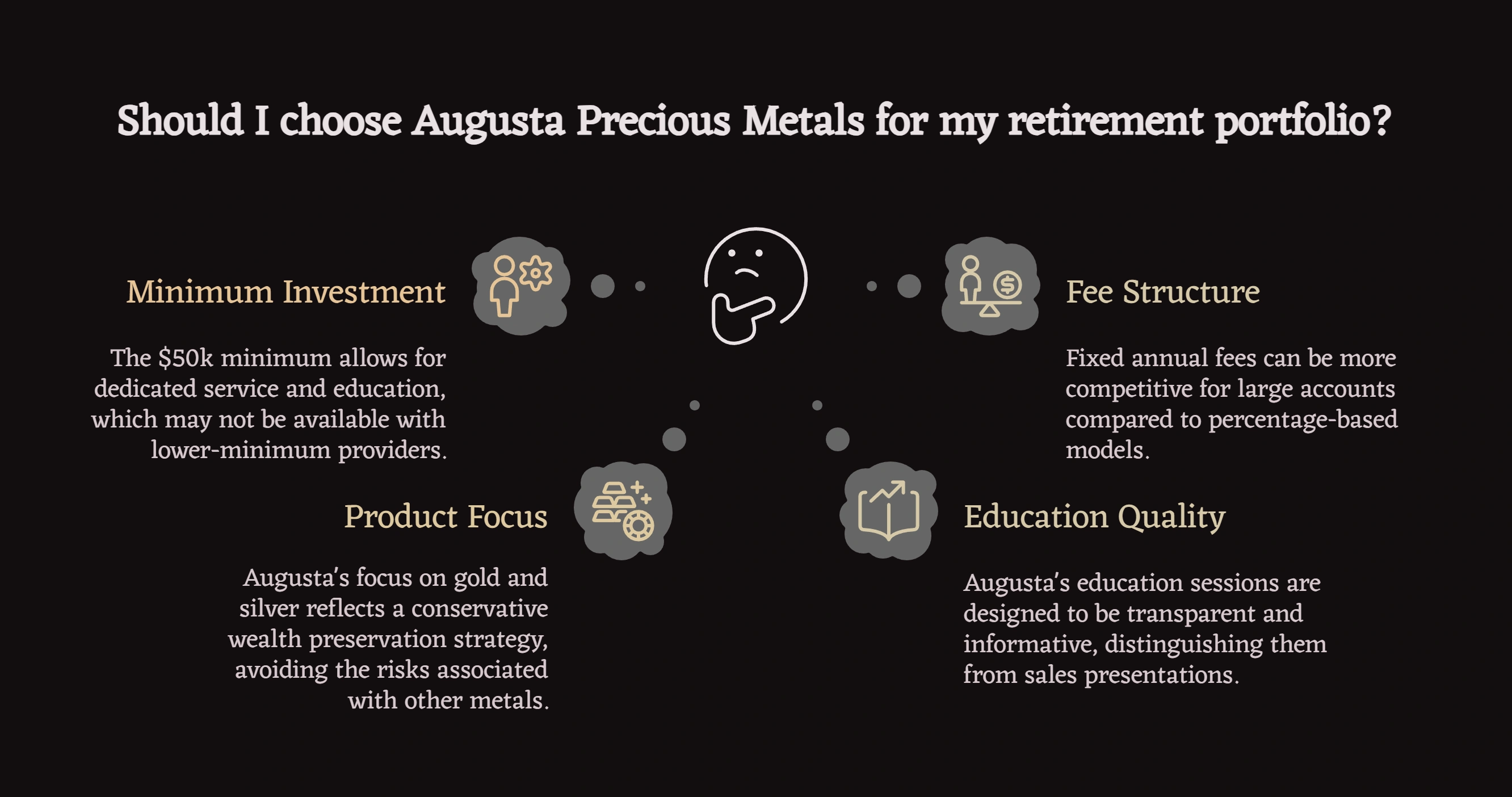

One of the first facts investors learn about this company is that Augusta Precious Metals requires a minimum investment of $50,000. In an industry where many competitors vie for business with lower, or even non-existent, minimums, this figure can seem daunting. However, viewing the Augusta Precious Metals account minimum of 2026 as a simple barrier is to miss its strategic purpose. This threshold is not a flaw; it is a feature designed to create a specific kind of client experience.

By establishing this minimum, Augusta deliberately filters for serious investors who are committing a significant portion of their assets to long-term wealth preservation. This approach allows the company to move away from a high-volume, transactional model and instead cultivate an environment of deep, personalized engagement. The answer to the question, is Augusta’s $50,000 minimum worth it, lies in understanding the caliber of service this focus enables. It creates the foundation for the Augusta Precious Metals white-glove service, a concierge-level experience that high-volume, mass-market providers are not structured to replicate.

For those considering a substantial investment, this translates into tangible benefits. Instead of being routed through a generic call center, clients are paired with a dedicated specialist who understands the nuances of a large account. This level of customer support for high-value clients at Augusta ensures continuity and a deep understanding of your personal goals. The Augusta Precious Metals lifetime account support means this relationship doesn’t end after the initial transaction; it extends for the entire duration you hold the account. This long-term commitment is a crucial factor when contemplating why to choose Augusta Precious Metals for a significant investment.

The ROI of Education: Supporting Informed Decision-Making at Scale

When you are considering an IRA rollover process for balances over $100k, the potential for a single misstep is magnified. A mistake that might be a minor setback for a small account can have severe consequences for a larger one. This is where the value of Augusta’s educational model becomes clear. The company’s philosophy is not merely to sell precious metals, but to ensure each investor is thoroughly educated before committing any funds.

A cornerstone of this approach is Augusta’s one-on-one web conference for investors. This is not a sales pitch; it is an intensive educational session led by a Harvard-trained economic analyst. The session covers the intricacies of the economy, the role of gold and silver in a portfolio, and, critically, the common gimmicks and high-pressure tactics used by some other IRA companies. For an investor with a portfolio over $500k, this education in risk awareness can provide more value than saving a few hundred dollars on initial fees. It helps equip investors to navigate the market with greater confidence and avoid the predatory practices that can erode a substantial nest egg.

This commitment to education helps sophisticated investors understand complex topics, such as the tax implications of a large precious metals IRA and the specific types of IRA-eligible bullion for high-value accounts. It addresses the fundamental goal of securing a large nest egg with precious metals by supporting investors with knowledge. This focus on informed decision-making is a core component of their strategy for retirement protection in 2026 and beyond.

Understanding Augusta’s Intentional Product Limitations

Augusta deliberately limits product selection to gold and silver only—a constraint that reflects a specific investment philosophy rather than a service gap.

Why Augusta offers only gold and silver: - Gold and silver have the longest historical track records as monetary metals - Eliminates complexity and potential confusion for investors new to precious metals - Reduces exposure to metals with higher industrial volatility (platinum, palladium) - Aligns with a conservative, long-term wealth preservation approach

The trade-off with Augusta’s model: This focused approach means investors seeking diversification into platinum or palladium must look elsewhere. This is intentional—Augusta positions itself as a specialist in the two core monetary metals, not a comprehensive precious metals marketplace. For investors who value depth of service and education over breadth of product options, this constraint is often viewed as an advantage. For those who specifically want exposure to industrial precious metals, it represents a limitation.

A Tale of Two Philosophies: Contrasting Service Models for Different Investor Needs

The precious metals IRA industry is largely divided into two camps, each with a distinct philosophy. Understanding this division is key to determining if Augusta is the right fit for your financial stature. The definition of “best” depends entirely on the size and goals of your investment.

High-Touch, High-Value: The Augusta Approach

This model, exemplified by Augusta, prioritizes depth over breadth. It is built for a specific clientele: high-net-worth individuals and affluent retirees who demand a higher level of service and risk management. The pros and cons of Augusta Precious Metals for large portfolios are two sides of the same coin.

- Pros: The unparalleled, personalized support from a dedicated team ensures a seamless experience when setting up a large self-directed IRA with Augusta. The deep educational resources empower investors to make informed, confident decisions. The focus is on building a long-term relationship, offering a robust Augusta Precious Metals buyback program and lifetime support. This model is often evaluated positively by accredited investors and those executing multi-million dollar portfolio diversifications.

- Cons: The primary drawback is its exclusivity. The high minimum makes it inaccessible for those looking to start with a smaller amount. It is not designed for individuals who want to make a small, speculative play in the metals market. Additionally, the limitation to gold and silver only means investors seeking platinum or palladium exposure must look elsewhere.

Low-Cost, High-Volume: The Mass-Market Alternative

On the other side of the spectrum are companies that cater to a broader audience by lowering the barrier to entry. For instance, in a market analysis of gold IRA companies, it was noted that in contrast to high-minimum providers, JM Bullion offers gold IRAs with no account minimum. This approach has its own set of advantages and disadvantages.

- Pros: The main advantage is accessibility. Anyone can open an account, regardless of their initial investment size. This makes it a good entry point for beginners or those who wish to diversify a small portion of their portfolio. The fee structures may appear more attractive for smaller account balances on a percentage basis.

- Cons: The trade-off for accessibility is often a lack of personalized service. Customer support may be less consistent, and the educational component is typically less robust. With a business model focused on volume, the experience can feel more transactional, and clients with larger, more complex needs may not receive the specialized attention they require. Comparisons like Augusta Precious Metals vs Goldco for large balances, or Augusta Precious Metals vs American Hartford Gold for $200k+, often highlight this difference in service depth.

Beyond Fees—The True Cost of Inexperience with a Seven-Figure Portfolio

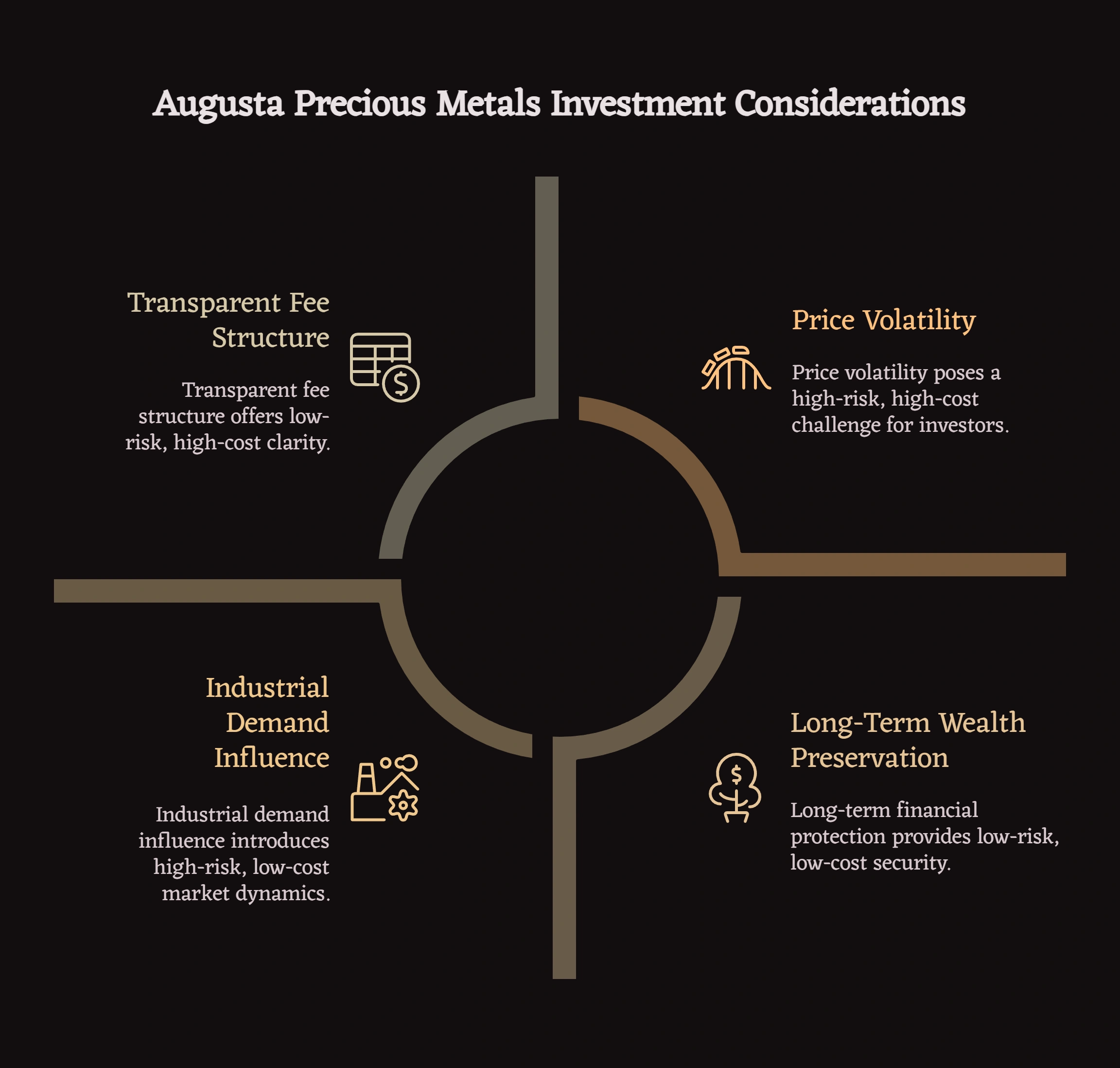

For investors managing substantial assets, the conversation must extend beyond a simple comparison of annual fees. The most significant financial danger is not a $100 storage fee; it is the risk of making an uninformed decision based on incomplete or misleading information. This is where Augusta’s industry-leading transparency becomes its most critical asset.

It is no small feat that based on an analysis of 17 gold IRA companies, Investopedia designated Augusta Precious Metals as ‘Best for Transparency’. This recognition stems from their commitment to clear, upfront communication about every aspect of the investment. The transparent pricing for Augusta Precious Metals means there are no hidden costs. From the outset, investors are given a complete breakdown of the fee structure. For example, the fee structure for a $250,000 gold IRA with Augusta is laid out plainly, including any one-time setup fees and recurring annual costs for storage and administration.

This clarity extends to the products themselves. Augusta helps clients select from a range of premium gold and silver products, explaining the difference between various coins and bars and their suitability for an IRA. They provide secure storage options through reputable third-party facilities, like the Delaware Depository, and detail the associated Augusta Precious Metals storage fees for large holdings. This removes the ambiguity that can plague the industry and helps protect investors from the real “cost” of a mistake, which can run into the tens of thousands on a large transaction.

Answering Your Critical Questions

When considering a significant financial move, specific questions naturally arise. Here are straightforward answers to some of the most common inquiries about investing with a company like Augusta.

What are the risks of investing in Augusta Gold?

No investment is without risk, and precious metals are no exception. The primary risks include price volatility—the value of gold and silver can fluctuate based on market conditions. Another consideration is liquidity; while Augusta has a buyback program, converting physical metals back to cash is not as instantaneous as selling a stock. A core part of Augusta’s educational process is to ensure every client understands these risks thoroughly before making an investment. They emphasize that precious metals are a long-term strategy for wealth preservation, not a short-term tool for speculative gains, noting that gold has a low correlation with other asset classes, which means that it can provide a hedge against market volatility and economic uncertainty.

What percentage of retirement should be in precious metals?

While Augusta Precious Metals cannot provide investment advice, as they are not fiduciaries but rather sellers of precious metals, they can share common strategies discussed by financial experts. Many financial advisors suggest an allocation of 5% to 15% of a total portfolio to precious metals. The right percentage depends on an individual’s age, risk tolerance, and overall financial goals. Augusta’s role is to provide the education necessary for you and your financial advisor to determine the appropriate allocation for your specific situation, helping you understand what percentage of a large portfolio should be in gold for your long-term security.

Will silver outperform gold in 2026?

Predicting the short-term performance of any asset is speculative. Gold and silver are driven by different factors. Gold is primarily a monetary metal and a safe-haven asset. Silver has significant industrial applications in addition to its monetary role, which means its price can be influenced by industrial demand and economic growth. Consequently, silver is often more volatile than gold. Rather than trying to predict which will “outperform,” most sophisticated investors view owning both gold and silver as a way to diversify within the precious metals asset class itself.

How much do Augusta precious metals charge?

Augusta is known for its transparent fee structure. Typically, this includes a one-time setup fee for the IRA account (which can sometimes be waived), an annual fee for your chosen IRA custodian, and an annual storage fee for the secure depository. For large accounts, these fixed annual fees become a smaller and smaller percentage of the total investment, which answers the question, are Augusta’s fees competitive for large investments? For multi-million dollar portfolios, the fixed-cost structure is often more advantageous than percentage-based fees found elsewhere. Augusta provides a full, detailed breakdown of all potential costs during their web conference so there are no surprises.

Common Misconceptions About Augusta Precious Metals

When evaluating Augusta for six-figure and seven-figure retirement account balances, several common misunderstandings can cloud the decision:

Misconception #1: “The $50k minimum is arbitrary or profit-driven” The minimum investment threshold is a business model choice that enables a specific service structure. It allows Augusta to provide dedicated specialists, in-depth education, and lifetime support—resources that high-volume, low-minimum providers cannot economically sustain.

Misconception #2: “Limited to gold and silver means incomplete service” Augusta’s focus on gold and silver only is intentional, not a gap. This specialization reflects a conservative wealth preservation philosophy and reduces complexity for investors. Platinum and palladium have different risk profiles tied to industrial demand—their exclusion is a feature of Augusta’s approach, not a limitation.

Misconception #3: “Education sessions are just sales presentations” The one-on-one web conference is structured as investor education, including discussion of common industry tactics and gimmicks used by other companies. This transparency-first approach distinguishes genuine education from promotional content.

Misconception #4: “Higher minimums always mean higher fees” While Augusta has a high minimum investment, their fee structure for large accounts is often more competitive than percentage-based models. Fixed annual fees become proportionally smaller as account size increases, making them particularly suitable for six- and seven-figure portfolios.

Decision Summary: Who Should (and Shouldn’t) Consider Augusta

Augusta Precious Metals is structured to serve a specific investor profile. Understanding whether you fit that profile is more important than debating whether Augusta is universally “best.”

Augusta is often well-suited for: - Investors with $100K+ retirement balances who meet the $50K minimum comfortably - Those who prioritize education, transparency, and lifetime relationship over lowest entry cost - High-net-worth individuals seeking white-glove service and dedicated specialists - Investors focused exclusively on gold and silver for conservative wealth preservation - Those executing a 401(k) or IRA rollover and valuing comprehensive onboarding support

Augusta is typically NOT well-suited for: - Investors with less than $50K to allocate to precious metals - Those seeking exposure to platinum or palladium in addition to gold and silver - Individuals prioritizing the absolute lowest fees over service quality - Speculators or short-term traders rather than long-term wealth preservers - Self-directed investors who prefer minimal guidance and transactional relationships

For a deeper look at Augusta’s fees, education process, storage options, and long-term gold and silver IRA approach, see our full Augusta Precious Metals review.

Making the Right Choice for Your Needs

The decision of which gold IRA company to partner with is not about finding the universally “best” option, but about finding the one that is structured to serve your specific needs. The suitability of any provider is directly tied to the investor’s profile and portfolio size.

The High-Net-Worth Retiree (Portfolio > $250k)

For this investor, wealth preservation, risk mitigation, and expert guidance are the highest priorities. The value of a dedicated specialist, in-depth education, and a company structured to handle complex, high-value transactions far outweighs the initial investment minimum. The concierge-level service and transparency offered by a high-minimum provider like Augusta align well with the needs of securing a substantial, multi-generational nest egg.

The Cautious First-Time Investor (Portfolio < $50k)

An investor who is new to precious metals and wants to start small to test the waters would not be a good fit for Augusta. The $50,000 minimum is a prohibitive barrier. For this profile, a low-minimum or no-minimum mass-market provider is the more logical choice. It allows them to gain experience with a smaller capital outlay and learn the basics of the market before making a more significant commitment.

The Self-Directed Diversifier (Portfolio $50k - $250k)

This investor sits in a middle ground. They meet the minimum investment requirement but may also be comfortable conducting their own extensive research. For this individual, the choice hinges on how much they value personalized guidance. If they desire a partner to walk them through the process, educate them on potential pitfalls, and offer long-term support, Augusta is an excellent choice. If they are highly confident, self-directed, and prioritize minimizing entry costs above all else, they might explore other options, though they would be forgoing the specialized service model.

Ultimately, the choice to partner with a precious metals company for a significant portion of your retirement savings is one of the most important you will make. Augusta Precious Metals has built its entire business model around serving the specific needs of serious investors with large balances, emphasizing education, transparency, and dedicated, long-term support. For those looking to make a substantial and well-informed investment in their financial future, this focused approach may provide a distinct advantage worth evaluating. To learn more about Augusta’s structure and determine if their model aligns with your specific retirement goals, you can explore their educational resources and fee transparency documentation.