.svg)

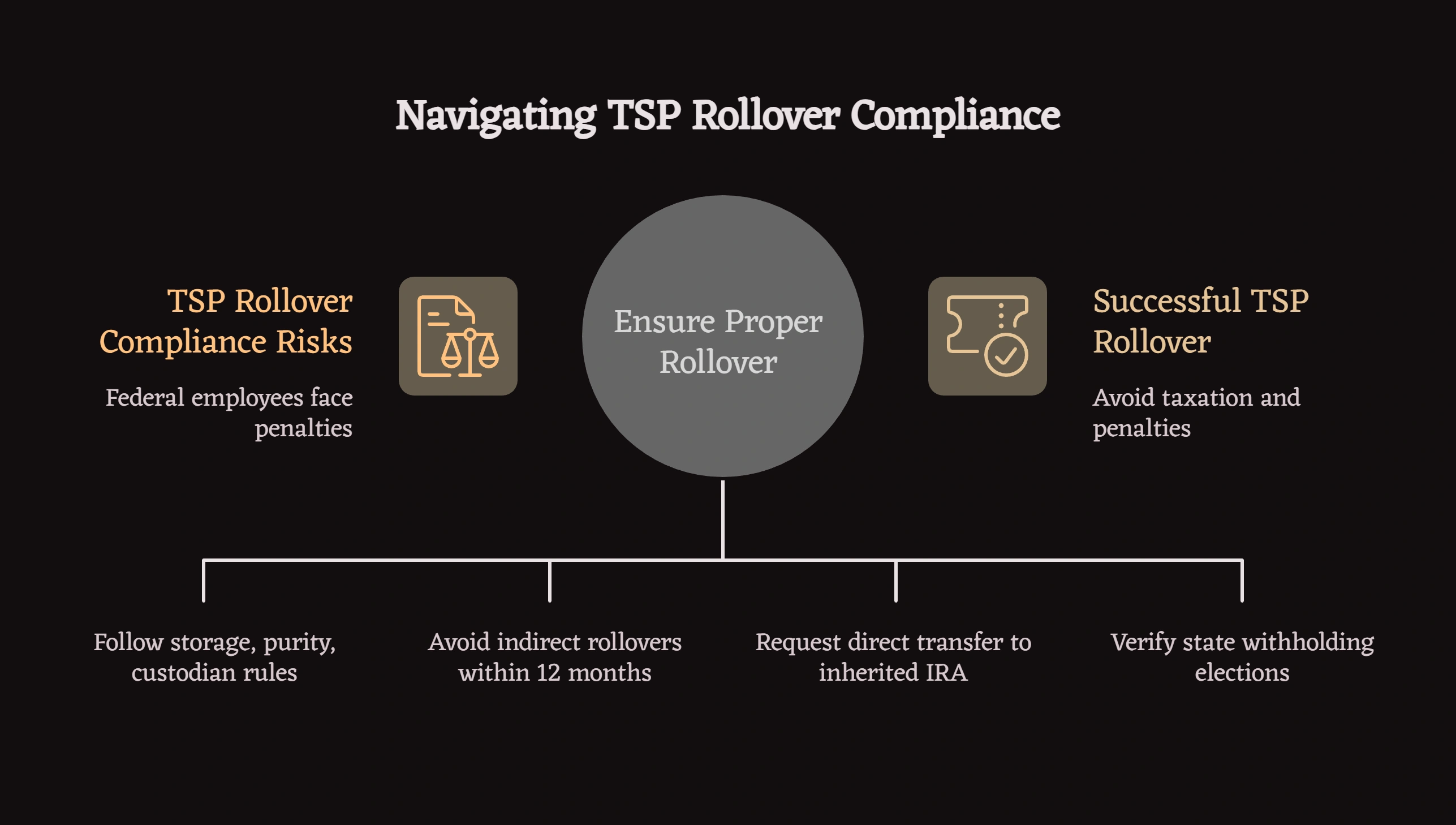

Federal employees executing TSP rollovers face specific IRS compliance requirements where mistakes trigger immediate taxation and penalties. The most costly errors involve indirect rollover timing failures, mandatory withholding miscalculations, and improper account type matching. According to IRS enforcement data, over 15% of indirect TSP rollovers result in unintended tax consequences, with federal employees losing an average of $8,000-$15,000 per incident through avoidable penalties and taxes.

Key Takeaways

- Indirect rollover failures account for the majority of IRS penalties—missing the 60-day deadline converts distributions into taxable income

- The 20% mandatory withholding on indirect rollovers creates out-of-pocket funding requirements most federal employees don't anticipate

- Account type mismatches (Traditional TSP to Roth IRA) trigger immediate taxation without proper conversion procedures

- Direct rollovers eliminate virtually all penalty risks by transferring funds trustee-to-trustee without personal possession

Understanding TSP Rollover Compliance Requirements

The Thrift Savings Plan operates under specific federal regulations managed by the Federal Retirement Thrift Investment Board. When federal employees move funds from TSP to other qualified retirement accounts—whether traditional IRAs, Roth IRAs, or self-directed accounts for alternative assets like precious metals—IRS rules govern every aspect of the transfer.

Compliance failures don't result from complex loopholes or obscure regulations. Most penalties stem from misunderstanding fundamental rollover mechanics, particularly the distinction between direct and indirect transfers.

Why This Question Keeps Coming Up

Federal employees approaching retirement receive information from multiple sources—TSP seminars, financial advisors, precious metals dealers, and fellow retirees. This information often conflicts or oversimplifies critical details about rollover execution. Understanding the specific mistakes that trigger IRS penalties helps federal employees distinguish between safe transfer procedures and costly errors.

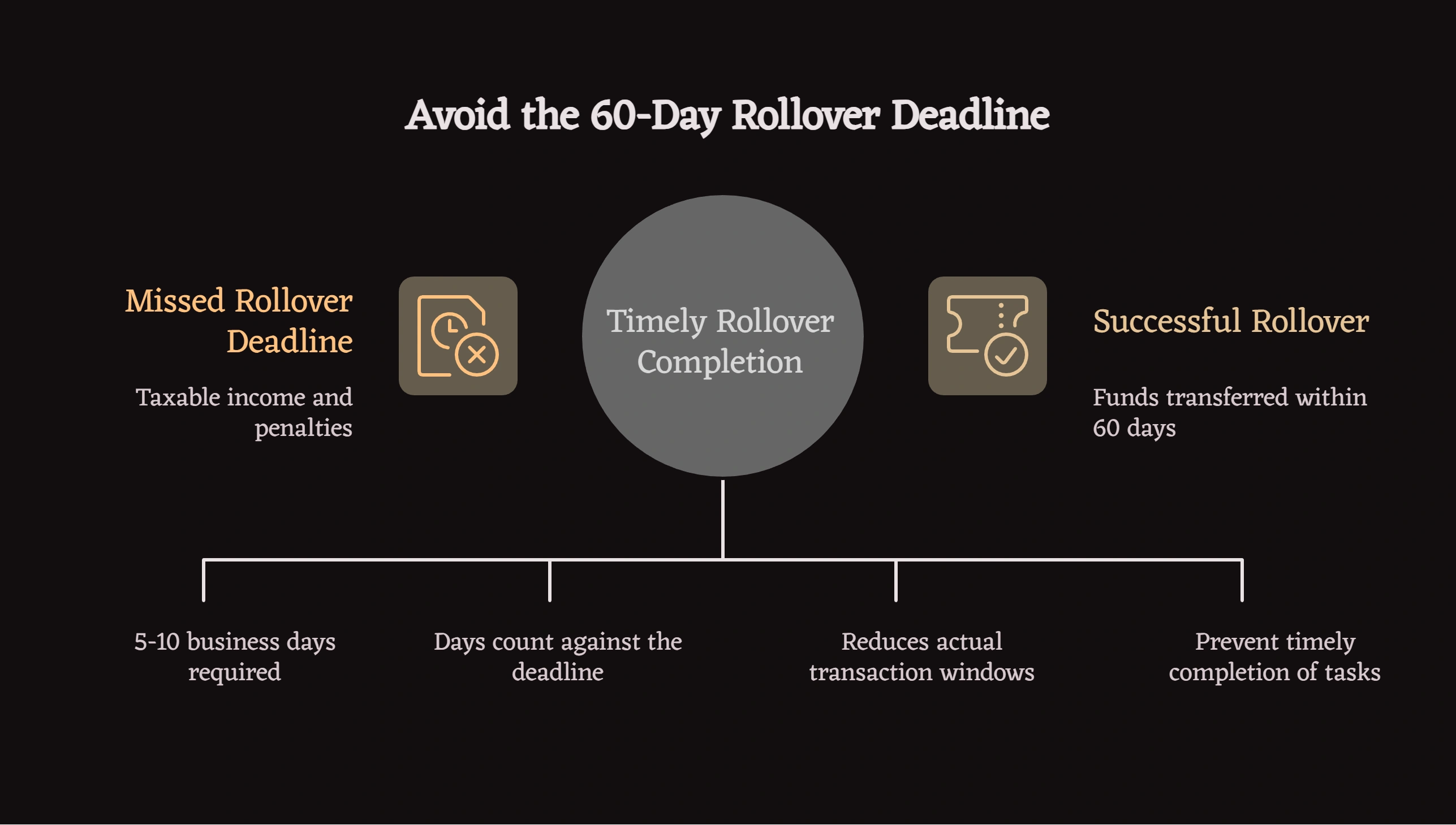

The 60-Day Indirect Rollover Deadline Trap

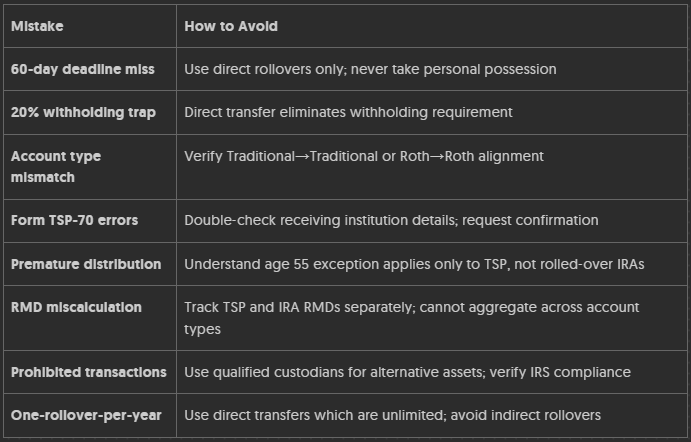

The most expensive rollover mistake involves indirect transfers where federal employees receive TSP distribution checks personally. IRS regulations require completing these rollovers within 60 calendar days from the date funds are received. Missing this deadline—even by a single day—converts the entire distribution into taxable income.

How the Deadline Gets Missed

Federal employees underestimate how quickly 60 days pass when dealing with:

- New IRA account establishment delays: Receiving institutions may require 5-10 business days to open accounts and verify documentation

- Mail processing time: Physical check deposits and account transfers consume days that count against the deadline

- Weekend and holiday compression: 60 calendar days includes non-business days, reducing actual transaction windows

- Personal emergencies: Medical issues, family crises, or travel disruptions prevent timely completion

For a $150,000 TSP distribution, missing the 60-day deadline triggers:

- Federal income tax on the full $150,000 (potentially $30,000-$45,000 depending on tax bracket)

- 10% early withdrawal penalty if under age 59½ (an additional $15,000)

- State income tax in most jurisdictions (varies by state)

Total cost: $45,000-$65,000 in unintended taxes and penalties—permanent capital destruction that can never be recovered.

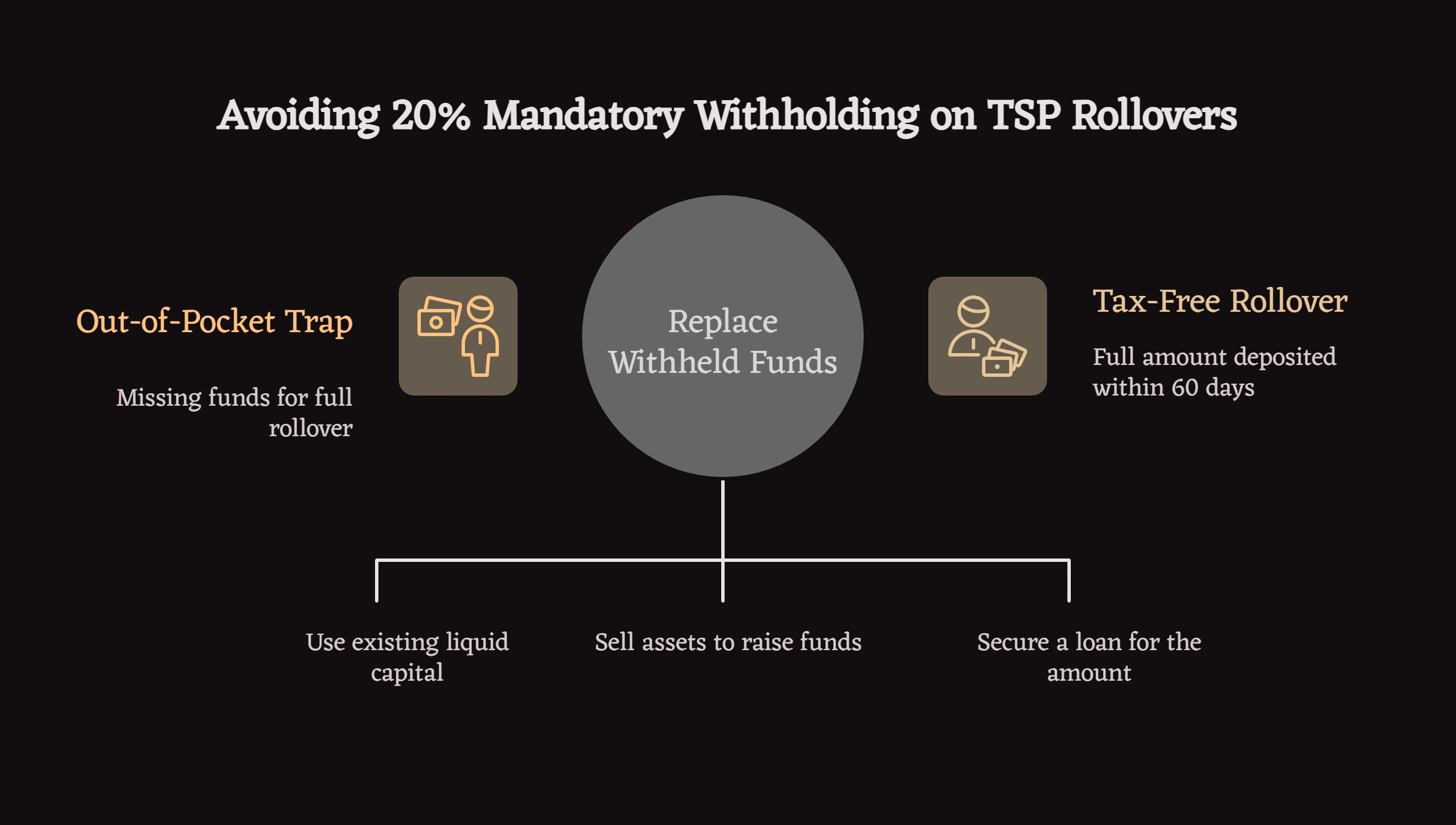

The 20% Mandatory Withholding Problem

Federal law requires the FRTIB to withhold 20% of any taxable TSP distribution paid directly to federal employees through indirect rollovers. This withholding applies regardless of stated intentions to complete a full rollover.

The Out-of-Pocket Trap

A civil service retirement system employee requesting a $200,000 indirect rollover receives a check for $160,000. The remaining $40,000 goes directly to the IRS as withholding. To complete a tax-free rollover, the employee must deposit the full $200,000 into their new IRA within 60 days.

The missing $40,000 must come from personal savings, liquidated investments, or borrowed funds. Veterans transitioning from military service and federal employees entering retirement often lack immediate access to tens of thousands in liquid capital. Failing to replace the withheld amount means:

- The $40,000 becomes permanently taxable income

- 10% early withdrawal penalty applies if under 59½

- Tax bracket impacts compound the losses

This scenario affects employees pursuing various IRA strategies—whether rolling into traditional brokerage IRAs, self-directed accounts for real estate investments, or precious metals IRAs for inflation protection through physical gold and silver holdings.

Account Type Mismatch Mistakes

TSP accounts exist in two forms: Traditional (pre-tax) and Roth (after-tax). The destination account type matters enormously for tax consequences.

Traditional TSP to Roth IRA Conversions

Moving Traditional TSP funds into a Roth IRA constitutes a Roth conversion, not a simple rollover. The entire distribution becomes taxable income in the year of conversion. Federal employees making this move without understanding tax implications face unexpected five-figure tax bills.

Correct approach: Execute as deliberate Roth conversion with tax planning, not as standard rollover.

Roth TSP to Traditional IRA Mistakes

Moving Roth TSP funds into Traditional IRAs reverses the tax-free status of contributions and earnings. While not immediately penalized, this mistake eliminates the primary benefit of Roth accounts—tax-free distributions in retirement.

Correct approach: Roth TSP funds should transfer only to Roth IRAs to maintain tax-free status.

Mixed Account Complications

Some federal employees maintain both Traditional and Roth TSP balances. Rolling these into a single destination account creates reporting complications and potential tax issues. The IRS requires separate accounting for pre-tax and after-tax funds.

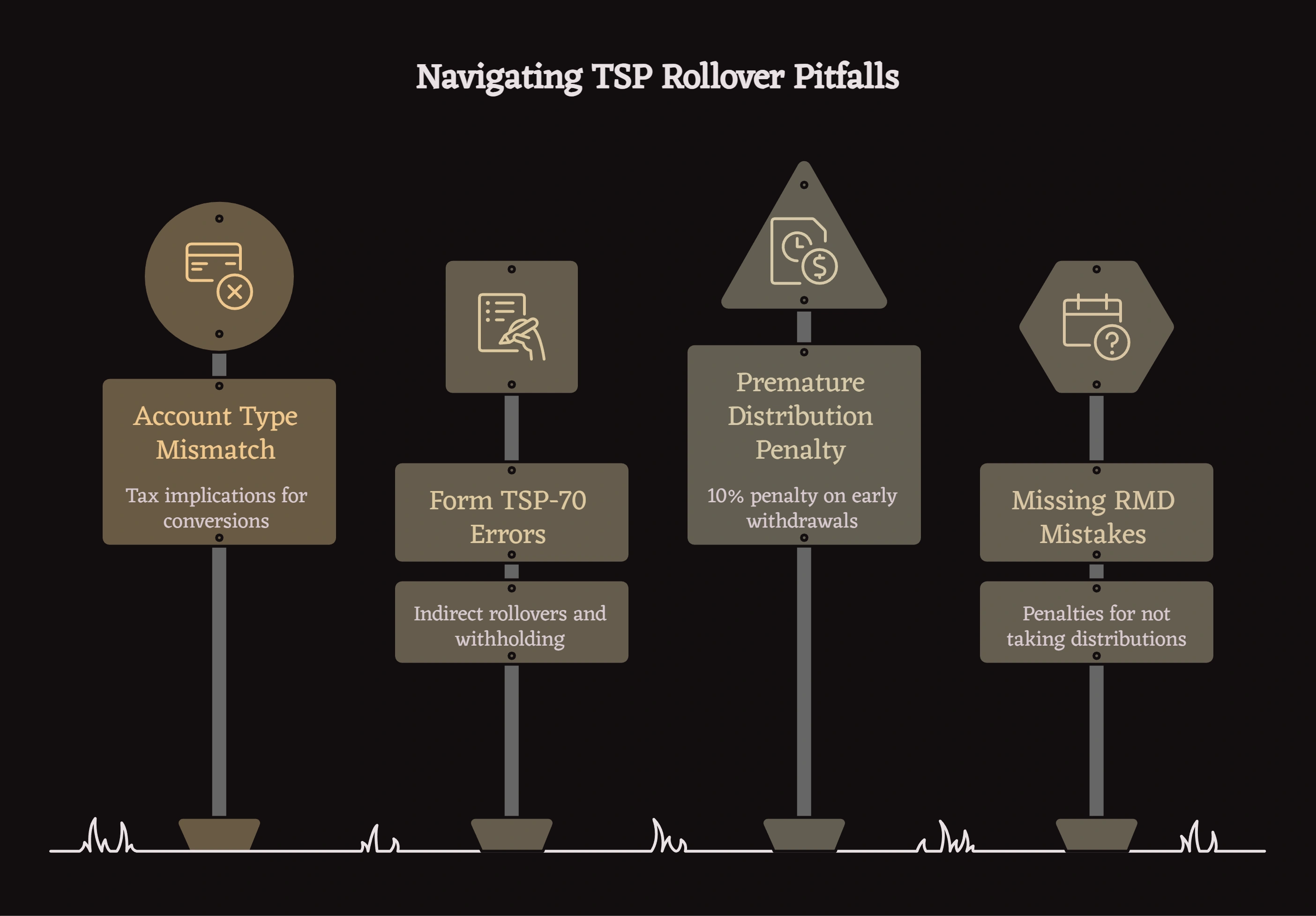

Form TSP-70 Completion Errors

The Request for Full Withdrawal form (TSP-70) determines whether funds transfer directly to the receiving institution or come to the federal employee personally. Completion errors create indirect rollovers when direct transfers were intended.

Common Form Mistakes

Incorrect receiving institution information: Wrong routing numbers, account details, or addresses delay transfers and may cause checks to be issued to the employee instead.

Missing direct rollover designation: Failing to check the correct box results in checks being mailed to the employee, triggering withholding and deadline requirements.

Incomplete new account establishment: Requesting rollovers before fully opening and verifying receiving accounts causes processing failures.

Partial vs. full rollover confusion: Incorrectly specifying amounts leads to unintended partial distributions subject to taxation.

The Premature Distribution Penalty

Federal employees under age 59½ face 10% early withdrawal penalties on distributions not properly rolled over. This penalty applies on top of ordinary income taxes.

Age 55 Exception Confusion

A special exception allows penalty-free TSP withdrawals after separating from federal service in or after the year of turning 55. This exception does NOT apply to IRA distributions—only to funds remaining in TSP or other employer plans.

Federal employees who:

- Separate from service at age 57

- Roll TSP funds to an IRA

- Take distributions from the IRA before 59½

...lose the age 55 exception and face 10% penalties on IRA distributions. This mistake particularly affects federal law enforcement officers and air traffic controllers with earlier retirement ages.

Missing Required Minimum Distribution Mistakes

Federal employees who leave TSP funds in place while also maintaining IRAs must calculate Required Minimum Distributions separately for each account type after age 73.

Aggregation Confusion

RMDs from multiple Traditional IRAs can be calculated collectively and withdrawn from any single IRA. TSP RMDs must come specifically from the TSP—they cannot be satisfied through IRA withdrawals.

Federal employees who:

- Rolled partial TSP amounts to IRAs

- Left remaining funds in TSP

- Attempt to satisfy all RMDs through IRA withdrawals

...face 25% excise penalties on TSP RMDs not taken properly.

Self-Directed IRA Prohibited Transaction Risks

Federal employees rolling TSP funds into self-directed IRAs for alternative assets face additional compliance requirements. Self-directed accounts permit investments beyond traditional stocks and bonds—including real estate, private placements, and precious metals.

Precious Metals IRA Compliance

For federal employees considering gold and silver IRAs as inflation protection strategies, specific IRS rules govern these holdings:

Storage requirements: IRA-owned precious metals must remain with IRS-approved custodians at qualified depositories. Personal possession triggers immediate taxation and penalties. A U.S. Tax Court case confirmed that home storage of IRA gold resulted in taxable distribution of the entire account value plus penalties.

Purity standards: Gold must meet .995 fineness; silver requires .999 fineness. Only specific bullion products qualify—most collectible or numismatic coins are prohibited.

Custodian requirements: Self-directed precious metals IRAs require specialized custodians familiar with IRS regulations for alternative assets. Using non-qualified custodians creates compliance failures.

Federal employees pursuing this strategy—whether through established providers like Noble Gold Investments, Augusta Precious Metals, Birch Gold Group, or other firms—must ensure proper account structure from the outset. Correcting compliance mistakes after the fact often proves impossible, resulting in permanent taxation.

One-Rollover-Per-Year Rule Violations

IRS regulations limit federal employees to one indirect rollover between IRAs within any 12-month period. This rule does NOT apply to:

- Direct trustee-to-trustee transfers (unlimited)

- Rollovers from TSP to IRAs (not counted)

- Roth conversions

However, once TSP funds enter an IRA, subsequent indirect rollovers from that IRA to another IRA trigger the one-per-year limitation.

The Violation

A federal employee who:

- Executes indirect rollover from IRA A to IRA B in March

- Attempts indirect rollover from IRA B to IRA C in November of the same year

...violates the rule. The second rollover becomes a taxable distribution subject to penalties.

Spousal Beneficiary Rollover Mistakes

When federal employees die, their TSP accounts pass to designated beneficiaries. Surviving spouses have unique rollover options not available to non-spouse beneficiaries.

The 60-Day vs. Direct Transfer Confusion

Surviving spouses receiving TSP distributions face the same 60-day indirect rollover deadline as living participants. However, they can also request direct rollovers to inherited IRAs without taking personal possession.

The mistake: Surviving spouses who receive TSP death benefit checks personally, intending to deposit them within 60 days, face:

- Mandatory 20% withholding (which doesn't apply to direct beneficiary transfers)

- Strict 60-day deadline during already stressful circumstances

- Potential taxation if deadlines are missed

Correct approach: Surviving spouses should request direct transfer from TSP to inherited IRA, avoiding personal possession entirely.

State Tax Withholding Oversights

Federal income tax withholding doesn't address state tax obligations. Federal employees moving to or from states with income taxes must consider state withholding requirements separately.

Several states do NOT have income taxes:

- Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming

Federal employees who:

- Relocate from taxed states to no-tax states during TSP rollover

- Or vice versa

...should verify proper state withholding elections to avoid underpayment penalties.

How to Avoid Every Rollover Mistake

Use Direct Rollovers Exclusively

Direct trustee-to-trustee transfers eliminate virtually all penalty risks:

- No 60-day deadline to track

- No mandatory 20% withholding

- No risk of personal possession mistakes

- Clean tax documentation (Form 1099-R coded properly)

Federal employees should complete Form TSP-70 specifying direct rollover to the new custodian, providing complete receiving institution details.

Verify Account Type Matching

Confirm destination account tax treatment:

- Traditional TSP → Traditional IRA (tax-deferred)

- Roth TSP → Roth IRA (tax-free)

- Traditional TSP → Roth IRA only if deliberate conversion with tax planning

Document Everything

Maintain copies of:

- Completed Form TSP-70

- Receiving institution confirmations

- IRS Form 1099-R from FRTIB

- IRS Form 5498 from receiving custodian

- All correspondence with both institutions

Consult Before Acting

TSP rollover decisions affect decades of accumulated savings. Federal employees benefit from consulting:

- Fee-only fiduciary financial advisors familiar with federal benefits

- Qualified tax professionals who understand TSP-specific rules

- Receiving institution representatives who can confirm proper procedures

For federal employees considering alternative assets like precious metals IRAs, additional due diligence includes verifying:

- Custodian IRS approval and track record

- Depository security and insurance

- Fee structures and total cost analysis

- Dealer pricing transparency (spreads over spot price)

Federal employees evaluating whether precious metals fit within broader retirement strategies—including traditional securities, real estate, or other alternatives—may benefit from reviewing a comprehensive analysis of whether rolling over a TSP into a gold IRA makes sense for their situation, including pros, cons, and common execution mistakes.

Protection Strategies Summary

When Mistakes Happen: Remediation Options

Despite best efforts, rollover mistakes sometimes occur. Limited remediation options exist:

60-Day Extension Waivers

The IRS may grant hardship waivers for missed 60-day deadlines if:

- Financial institution errors caused delays

- Serious illness prevented timely completion

- Documentation proves good-faith attempt

Waivers are NOT guaranteed and require formal IRS application with supporting documentation.

Recharacterization (Limited Availability)

Some mistaken Roth conversions can be reversed through recharacterization, though recent tax law changes have eliminated this option for most situations.

Corrective Distributions

Certain excess contribution mistakes can be corrected through timely distributions, though this doesn't apply to most rollover errors.

The key principle: Prevention dramatically outperforms remediation. Once rollover mistakes trigger taxation and penalties, reversing those consequences rarely succeeds.

Making Informed TSP Rollover Decisions

Federal employees have built TSP accounts through years of consistent contributions and employer matching. These balances represent significant retirement security requiring protection through informed decision-making.

Understanding the specific mistakes that trigger IRS penalties helps federal employees execute rollovers safely—whether moving funds to traditional brokerage IRAs, self-directed accounts for alternative investments, or maintaining TSP participation.

The choice to rollover depends on individual circumstances: investment objectives, fee sensitivity, desired asset classes, and comfort with self-directed management. That choice should be made with complete understanding of execution requirements and penalty avoidance strategies.

Disclaimer: This article provides educational information about TSP rollover compliance and common penalty triggers. It does not constitute financial, tax, or legal advice. Federal employees and military service members should consult qualified financial advisors, tax professionals, and legal counsel before making retirement account decisions. Rollover choices involve individual circumstances including tax situations, investment objectives, retirement timing, and risk tolerance. The IRS provides official guidance through Publication 590-A and Publication 590-B, which should be reviewed for authoritative regulatory information.

References

[1] Internal Revenue Service. "Publication 590-A: Contributions to Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[2] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[3] Internal Revenue Service. "Topic No. 413: Rollovers from Retirement Plans." IRS.gov.

[4] Federal Retirement Thrift Investment Board. "Withdrawals in Retirement." TSP.gov.

[5] Internal Revenue Service. "Retirement Topics - Required Minimum Distributions (RMDs)." IRS.gov.

[6] U.S. Tax Court. "McNulty v. Commissioner: IRA Precious Metals Storage Requirements." Tax Court Case Precedent.

[7] Internal Revenue Service. "IRC Section 408(m): Treatment of Collectibles in IRAs." IRS.gov.

[8] Federal Retirement Thrift Investment Board. "Form TSP-70: Request for Full Withdrawal." TSP.gov.

[9] Internal Revenue Service. "One-Rollover-Per-Year Rule." IRS.gov.

[10] U.S. Office of Personnel Management. "FERS Transfer Handbook." OPM.gov.