.svg)

A comprehensive analysis of precious metals rollovers for federal employees, including hidden pitfalls that can cost thousands in penalties.

Most federal employees don't realize their Thrift Savings Plan (TSP) rollover decision could either protect their retirement or trigger devastating tax penalties. While precious metals IRAs offer compelling benefits for portfolio diversification, the rollover process contains hidden traps that have cost federal workers tens of thousands of dollars in avoidable mistakes.

This analysis examines the real advantages and risks of converting TSP funds to physical gold and silver, based on actual federal employee experiences and IRS regulations. Understanding these factors helps you make informed decisions about whether precious metals belong in your retirement strategy.

This guide explains the advantages, risks, and common mistakes federal employees face when moving TSP funds into self-directed precious metals IRAs.

Key Takeaways

- Direct rollovers avoid the 10% early withdrawal penalty that affects 60-day indirect transfers

- Gold IRAs provide inflation protection but come with higher fees than TSP's low-cost structure

- Federal employees over age 59½ can make partial rollovers while remaining employed

- Common mistakes include missing deadlines, choosing wrong account types, and overlooking tax implications

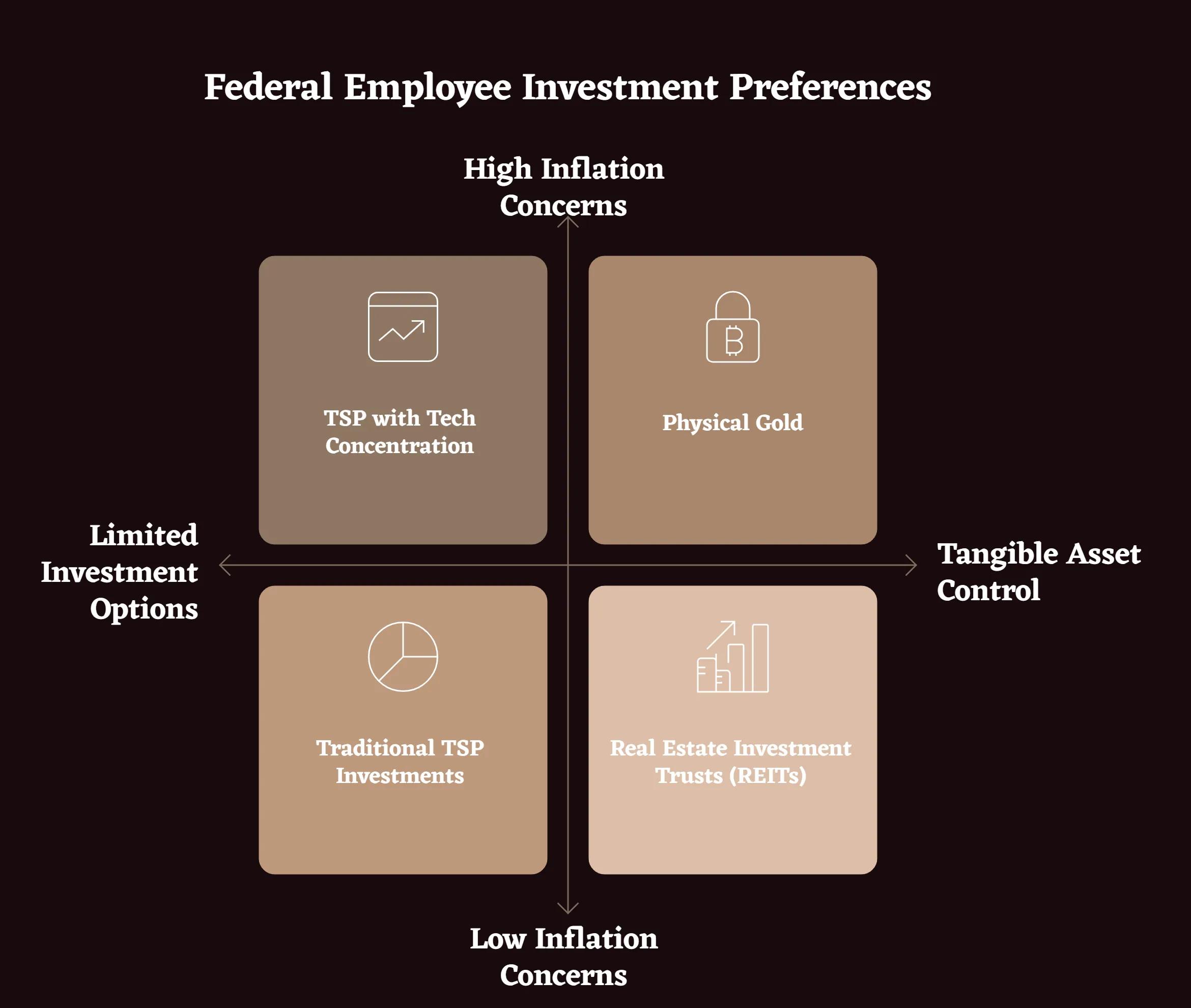

Why Federal Employees Consider a Gold IRA Rollover

Federal workers face unique retirement challenges that drive interest in alternative asset diversification beyond traditional TSP investments.

Limited Investment Options Create Concentration Risk

The TSP's five-fund structure constrains federal employees to government securities, bonds, and broad market indices. This limitation becomes problematic when economic conditions favor assets outside these categories or when employees seek exposure to commodities and alternative investments [1].

Federal employees often express frustration with their inability to adjust portfolios during market volatility beyond the five predetermined options. The C Fund's heavy concentration in technology stocks exemplifies this constraint—seven major tech companies now drive disproportionate index performance, creating vulnerability should sector sentiment shift.

Inflation Concerns Drive Precious Metals Interest

Government workers possess front-row seats to fiscal policy discussions and mounting debt concerns. This insider perspective naturally leads to questions about long-term dollar stability and purchasing power preservation during retirement decades.

Recent inflation data showing sustained price increases across essential goods has prompted many federal employees to seek assets with historical inflation resistance. Physical precious metals offer this characteristic, having maintained purchasing power across centuries of currency devaluations and economic disruptions [2].

Desire for Tangible Asset Control

Federal employees who understand bureaucratic limitations often prefer retirement assets they can verify and control directly. Unlike digital account balances that depend on institutional stability, physical gold and silver exist as tangible objects stored in secure facilities under individual ownership.

This psychological comfort appeals particularly to military personnel and veterans who value independence from political decisions affecting government-sponsored retirement programs. Physical metals provide wealth storage that doesn't rely on future policy decisions or institutional solvency.

Looking ahead, federal employees may increasingly compare precious metals against other inflation hedges like Treasury Inflation-Protected Securities (TIPS) or real estate investment trusts (REITs). However, geopolitical tensions and potential currency competition from digital assets could drive more conservative investors toward physical metals that exist outside the traditional financial system entirely.

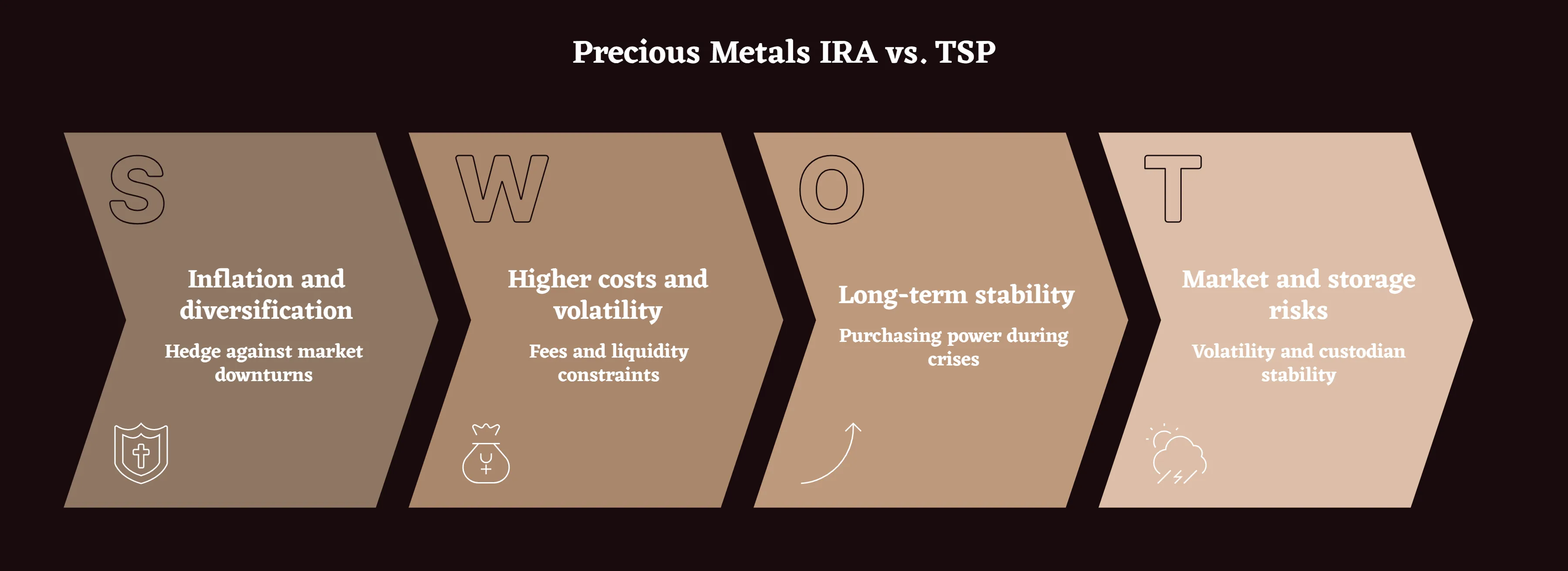

Pros of Moving TSP Funds to a Precious Metals IRA

Key Advantages:

- Inflation hedge: Gold rose from $35 to $800+ during 1970s inflation crisis.

- Diversification: Precious metals move independently from stocks and bonds.

- Direct ownership: Coins and bars held in your name at secure vaults.

- Geographic flexibility: Choose Delaware, Texas, or Canadian depositories.

Details below expand on each point:

Inflation Protection Through Historical Stability Gold has maintained purchasing power across multiple economic cycles, currency collapses, and inflationary periods throughout recorded history. During the 1970s inflation crisis, gold prices increased from $35 to over $800 per ounce, providing substantial purchasing power protection for holders [2].

If you believe current inflation trends may persist long-term, then allocating a portion of retirement savings to historically inflation-resistant assets could provide portfolio balance.

Portfolio Diversification Beyond Paper Assets Physical precious metals offer low correlation with traditional investments, providing genuine diversification benefits during market stress periods. When stocks and bonds decline simultaneously, gold often maintains or increases value, helping stabilize overall portfolio performance.

Direct Ownership and Storage Control Alternative asset IRAs provide ownership of specific coins and bars held in investors' names at secure depositories, rather than claims on pooled assets. This direct ownership provides verification opportunities through facility visits and detailed quarterly statements showing exact holdings.

Geographic Storage Flexibility Modern precious metals IRAs offer storage options across multiple states and countries, allowing geographic diversification of retirement assets. Texas, Delaware, and Canadian facilities provide alternatives to traditional East Coast storage, appealing to federal employees seeking regional distribution.

Cons and Risks You Should Understand

Potential Drawbacks:

- Higher fees: Annual costs ($200-$500) exceed TSP's <0.05% expense ratios.

- Reduced liquidity: Converting metals to cash takes days vs instant transfers.

- Third-party reliance: Success depends on vault security and custodian stability.

- Price volatility: Gold dropped 40%+ between 2011-2015.

Details below expand on each point:

Higher Fees Compared to TSP Structure The TSP's expense ratios typically run under 0.05%, making it one of the lowest-cost retirement plans available. Physical bullion IRAs charge annual custodial fees ($50-$300), storage fees ($100-$300), and setup costs that can total $200-$500 annually regardless of account size [3].

Liquidity Constraints During Distribution Converting physical precious metals to cash for retirement income requires selling metals and transferring proceeds, a process taking several business days. This contrasts with TSP accounts offering immediate access to funds through electronic transfers.

Storage and Insurance Dependencies Alternative hard asset IRAs depend on third-party storage facilities and insurance coverage for asset protection. While reputable providers maintain comprehensive security and insurance, investors ultimately rely on institutional stability they sought to avoid through precious metals ownership.

Market Volatility Despite Long-Term Stability While gold provides long-term purchasing power protection, short-term price volatility can be substantial. Federal employees nearing retirement might experience significant account value fluctuations that could affect distribution planning and psychological comfort.

Where Are Precious Metals IRAs Stored?

Physical bullion IRAs must use IRS-approved depositories with secure facilities and full insurance coverage.

Major Depository Locations

- Delaware Depository (Wilmington, DE): Most common East Coast option, offering both segregated and commingled storage.

- Texas Precious Metals Depository (Dallas, TX): State-of-the-art facility serving Southwest federal employees and retirees.

- IDS of Canada (Mississauga, Ontario): International diversification option for cross-border considerations.

Segregated vs. Commingled Storage

- Segregated: Your specific coins/bars held separately under your name. Higher cost ($150–$250/yr) but maximum control and estate planning clarity.

- Commingled: Lower cost ($100–$150/yr). Metals pooled but records maintain your ownership share.

Federal employees often choose segregated storage for verification capabilities and facility visit options.

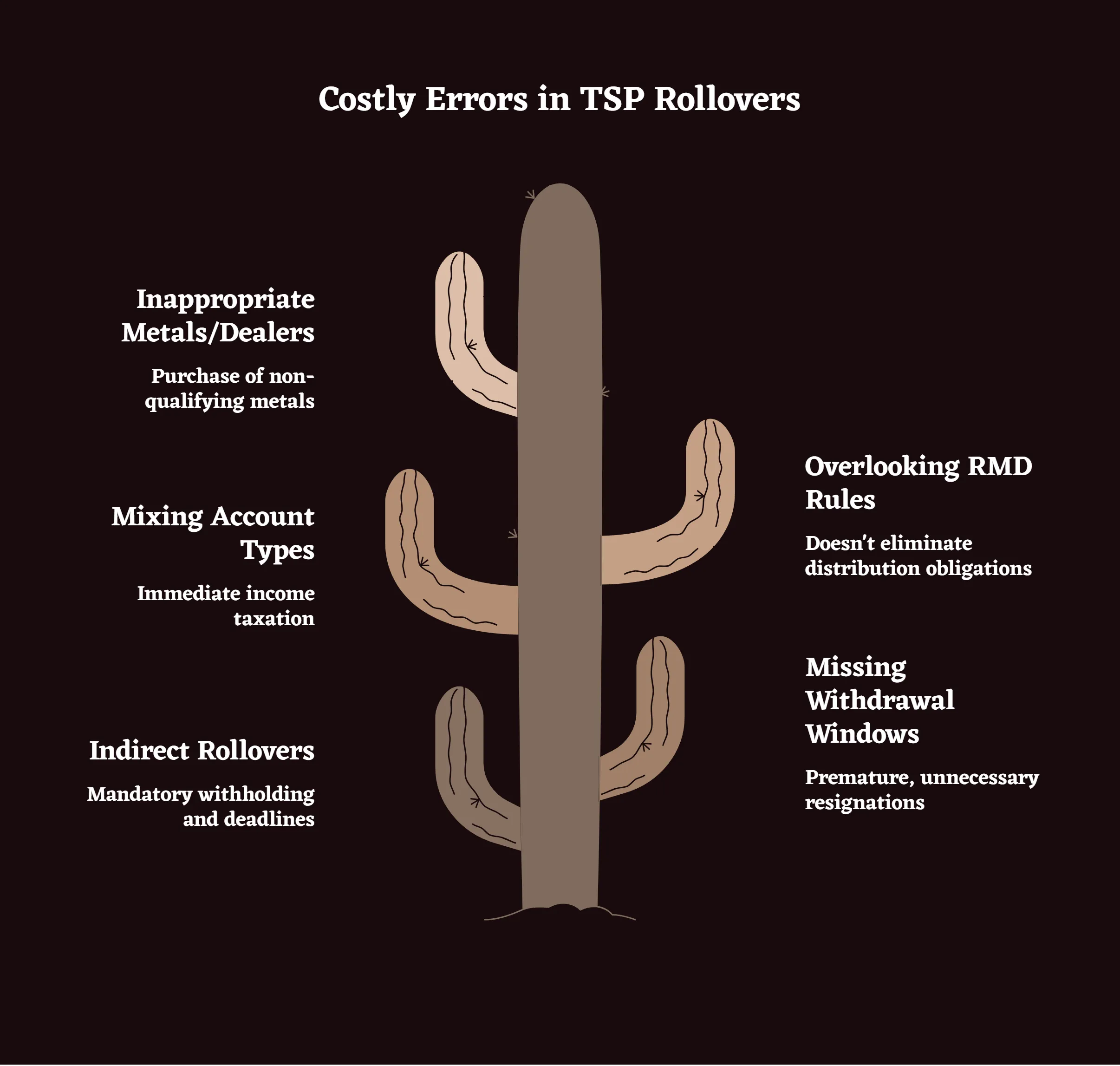

Common Mistakes in the Rollover Process

Federal employees frequently make costly errors during TSP to self-directed IRA conversions that trigger penalties and tax consequences.

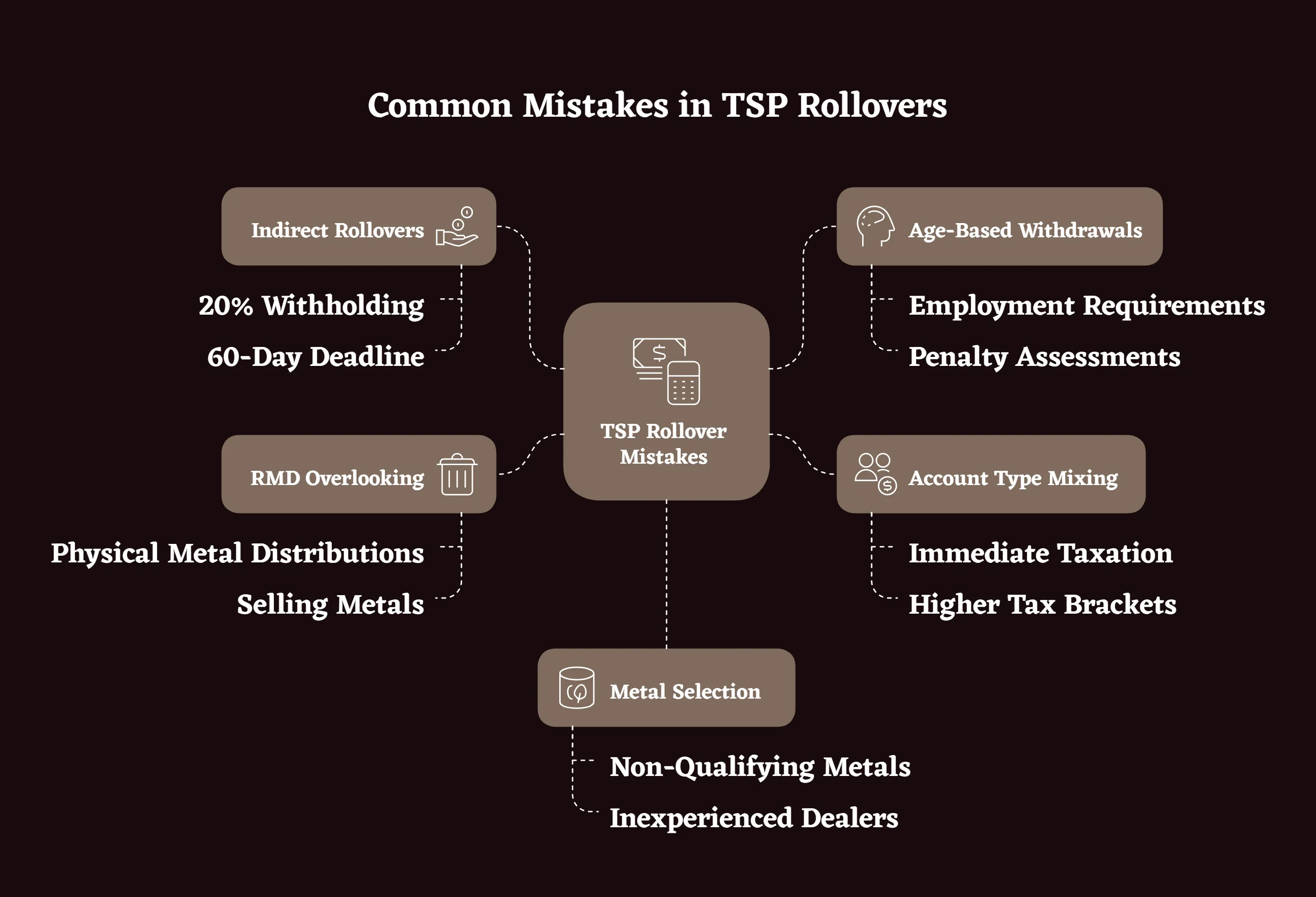

Choosing Indirect Over Direct Rollovers

The most expensive mistake involves taking personal possession of TSP funds during rollover rather than arranging direct trustee-to-trustee transfers. Indirect rollovers trigger 20% mandatory withholding and create 60-day deadlines for redepositing funds [4].

Federal employees receiving $100,000 TSP distributions face $20,000 immediate withholding. They must find $20,000 from other sources to complete the full rollover within 60 days, or face income tax and early withdrawal penalties on the withheld amount.

One common misstep occurs when federal employees take direct possession of their TSP funds thinking they’ll "reinvest later." If they miss the 60-day deadline, the IRS may treat the distribution as income, triggering both taxes and early withdrawal penalties—even if the intention was to reinvest.

Missing Age-Based Withdrawal Windows

Federal employees often misunderstand TSP withdrawal eligibility rules, attempting rollovers when still employed without meeting age 59½ requirements for in-service withdrawals. This triggers separation requirements or penalty assessments [1].

Some federal workers resign unnecessarily to access TSP funds, forgoing continued employment benefits and advancement opportunities when age-based withdrawals would have provided rollover access while maintaining employment.

Mixing Traditional and Roth Account Types

Improper account type matching during rollovers creates immediate tax consequences. Traditional TSP funds rolled to Roth Gold & Silver IRAs trigger current-year income taxation on the entire converted amount, potentially pushing federal employees into higher tax brackets.

Federal employees earning $80,000 who convert $200,000 traditional TSP funds to Roth accounts face immediate taxation on $200,000 as ordinary income, potentially doubling their tax liability for that year.

Overlooking Required Minimum Distribution Rules

Federal employees over age 73 must satisfy Required Minimum Distribution requirements from traditional retirement accounts. Rolling entire TSP balances to physical bullion IRAs doesn't eliminate RMD obligations—it transfers them to the new account [5].

Investors must either take physical metal distributions or sell metals annually to generate required cash distributions, adding complexity and potential costs to retirement income planning.

Selecting Inappropriate Metals or Dealers

Not all precious metals qualify for IRA inclusion. Collectible coins, numismatic pieces, and metals below IRS purity standards (gold 99.5%, silver 99.9%) trigger immediate taxation and penalty assessments [6].

Federal employees working with inexperienced dealers may unknowingly purchase non-qualifying metals, discovering tax problems only during IRS audits or required distributions years later.

Some providers, such as Noble Gold, offer dedicated specialists for federal employees to avoid exactly these mistakes.

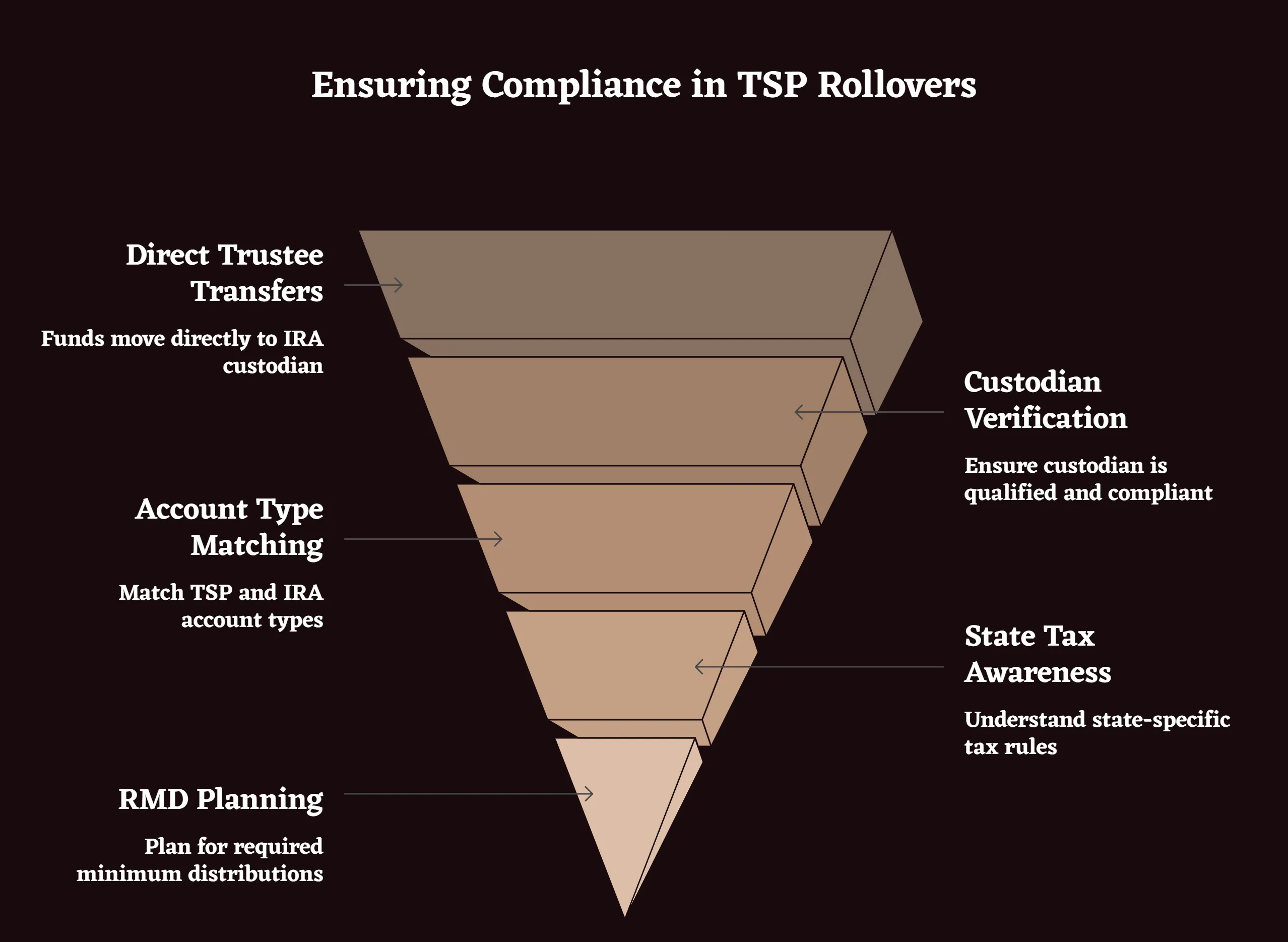

How to Avoid IRS Penalties

Proper rollover execution prevents costly mistakes and ensures compliance with federal tax regulations governing retirement account transfers.

Execute Direct Trustee-to-Trustee Transfers

Always arrange direct rollovers where TSP funds transfer directly to bullion IRA custodians without passing through personal accounts. This eliminates withholding requirements, avoids 60-day deadlines, and prevents accidental early withdrawal penalties.

Contact TSP administrators to initiate direct rollovers using Form TSP-70 for full withdrawals or TSP-77 for partial transfers. Provide exact custodian information and account details to ensure proper transfer completion.

Verify IRA Custodian Qualifications

Choose IRA custodians specifically approved for precious metals investments with established track records and proper regulatory compliance. Unqualified custodians can invalidate entire IRA structures, triggering immediate taxation on account values.

Research custodian credentials through IRS databases and industry associations. Verify insurance coverage, storage arrangements, and compliance histories before authorizing fund transfers.

For a provider walkthrough, see our Noble Gold TSP Rollover Guide that details the trustee-to-trustee process step-by-step.

Match Account Types Appropriately

Transfer traditional TSP funds to traditional Gold IRAs and Roth TSP funds to Roth Gold IRAs to maintain tax treatment. Cross-type transfers trigger immediate taxation that can be avoided through proper account matching.

Consider timing for strategic Roth conversions during low-income years when tax impact may be minimized, but understand the immediate tax consequences before proceeding.

Decision Support Checklist:

- Are your TSP funds traditional, Roth, or a mix?

- Are you planning a Roth conversion during a low-income year to reduce the tax hit?

- Do you understand how this affects your overall taxable income for the year?

Understand State Tax Implications

Some states tax precious metals transactions or impose additional regulations on alternative IRA investments. Research state-specific rules before executing rollovers to avoid unexpected tax liabilities [7].

Federal employees with multi-state work histories should consider tax consequences in both current residence states and states where they might retire.

Plan for Required Minimum Distributions

Develop strategies for satisfying RMD requirements from precious metal IRAs before reaching age 73. This might involve maintaining partial traditional account balances or planning annual metal sales to generate required distributions.

Consider the logistics of physical metal distributions versus cash distributions when planning retirement income strategies from precious metals accounts.

Federal employees considering a rollover should compare providers like Noble Gold and Birch Gold that specialize in TSP transfers. Choosing the right custodian avoids costly IRS mistakes and ensures metals are stored securely.

For step-by-step rollover guidance specific to federal employees, see our Noble Gold TSP Rollover Guide.

Frequently Asked Questions

Q: Is a TSP to precious metals rollover tax-free?

A: Yes, when executed as a direct trustee-to-trustee transfer using Form TSP-70 or TSP-77. Indirect rollovers may trigger 20% withholding and penalties.

Q: Can I roll over my entire Thrift Savings Plan balance to a Gold IRA?

A: Yes, federal employees can transfer any amount from TSP to Gold IRAs, from partial amounts to complete account balances. However, consider maintaining some traditional investments for liquidity and fee efficiency.

Q: How long does a Thrift Savings Plan to Gold IRA rollover take?

A: Direct rollovers typically complete within 2-3 weeks. TSP processes withdrawal requests in 7-14 business days, followed by precious metals selection and storage confirmation taking an additional 3-5 business days.

Q: What happens to my TSP matching contributions?

A: Vested TSP matching contributions can be rolled over with your other TSP funds. Unvested contributions may be forfeited depending on your years of service and separation circumstances.

Q: Can I reverse a Precious Metals IRA rollover back to TSP?

A: No. The TSP does not accept incoming rollovers. Once funds leave, they can only move to other retirement accounts.

Q: Do I need to report these rollovers on my tax return?

A: Direct rollovers don't require tax reporting as they're non-taxable events. However, Roth conversions and indirect rollovers must be reported on annual tax returns with potential tax consequences.

Q: Which precious metals qualify for IRA investment?

A: IRS-approved metals include gold (99.5% purity), silver (99.9% purity), platinum (99.95% purity), and palladium (99.95% purity) in coin or bar form from approved manufacturers and refiners.

For federal employees considering a rollover, compare specialized providers like Birch Gold Group and Noble Gold Investments that understand TSP transfer requirements and offer dedicated federal employee support.

Final Considerations for Federal Employees

TSP to precious metal IRA rollovers can provide valuable portfolio diversification and inflation protection for federal workers, but success depends on proper execution and realistic expectations about costs and limitations.

The TSP's exceptional fee structure and broad market exposure make it an excellent foundation for most federal employees. Precious metals allocation should complement rather than replace this core retirement benefit, typically representing 5-20% of total retirement assets depending on individual circumstances.

If you’re considering a 5–20% gold allocation, what specific role will those metals serve? Diversification? Inflation hedge? Political risk insurance? Identifying purpose can help guide allocation amount and type (e.g., bars vs. coins, segregated vs. commingled).

Federal employees considering precious metals rollovers benefit from consulting tax professionals familiar with government retirement systems and IRA regulations. The complexity of rollover rules and potential penalties make professional guidance valuable for significant financial decisions.

Next Steps: Explore trusted providers like Noble Gold and Birch Gold for compliant rollovers.

For step-by-step instructions, see our Noble Gold TSP Rollover Guide on how to complete a penalty-free transfer.

This article is for informational purposes only. It does not constitute financial advice. Always consult a licensed financial advisor before making investment decisions.

References

- Federal Retirement Thrift Investment Board. "TSP Withdrawal Options and Tax Implications." Thrift Savings Plan, 2025.

- World Gold Council. "Gold as a Store of Value: Historical Performance Analysis." World Gold Council, 2025.

- IRS. "Individual Retirement Arrangement (IRA) Information." Internal Revenue Service, 2025.

- IRS. "Rollover Chart." Internal Revenue Service, Publication 590-A, 2025.

- IRS. "Required Minimum Distributions from Retirement Plans." Internal Revenue Service, 2025.

- IRS. "Prohibited Transactions in Individual Retirement Accounts." Internal Revenue Service, Publication 590-B, 2025.

- Tax Foundation. "State Taxation of Precious Metals Transactions." Tax Foundation Research, 2025.