.svg)

A comprehensive guide to converting your federal retirement savings into physical precious metals through Noble Gold's specialized TSP rollover process.

Most TSP account holders don't realize they can move their federal retirement savings into a Gold IRA without triggering taxes or penalties. Whether you're a federal employee, military service member, or retired government worker, rolling over your Thrift Savings Plan to precious metals can offer inflation protection and portfolio diversification. This guide provides step-by-step instructions tailored for TSP investors who want more control over their retirement nest egg.

What Is the TSP and Why It Matters for Retirement Planning

The Thrift Savings Plan serves as the cornerstone of federal retirement security, yet many participants don't fully understand its limitations or alternatives for wealth preservation.

TSP Basics for Federal Employees & Military Members

The Thrift Savings Plan operates as a defined contribution retirement savings program for federal employees and uniformed service members. Established by the Federal Employees' Retirement System Act of 1986, it mirrors private sector 401(k) plans but with unique features designed for government workers [1].

Federal employees contribute through payroll deductions, with the government providing automatic contributions and matching funds up to 5% of basic pay. Military members can contribute but don't receive matching until completing 60 days of service, with full vesting after two years of service.

Your TSP account grows tax-deferred in traditional accounts or tax-free in Roth TSP accounts. The plan offers lifecycle funds that automatically adjust asset allocation based on your target retirement date, simplifying investment decisions for busy government workers.

What Makes the TSP Different From a 401(k) or IRA?

The TSP's structure differs significantly from private sector retirement plans and traditional IRAs. Most notably, participants choose from only five fund options: G Fund (government securities), F Fund (bonds), C Fund (large company stocks), S Fund (small company stocks), and I Fund (international stocks).

This limited selection contrasts sharply with typical 401(k) plans offering dozens of mutual fund choices. While simplicity helps some investors avoid decision paralysis, others find the constraints limiting for retirement diversification strategies beyond paper investments.

According to a 2024 Congressional Research Service study, nearly 62% of federal employees rely solely on TSP assets for retirement planning. This concentration increases exposure to long-term policy shifts such as adjustments in COLA or debt ceiling negotiations [1].

Why Many Retirees Consider a Rollover to Precious Metals

Federal employees increasingly explore precious metals rollovers due to concerns about paper asset concentration and inflation protection. The civilian federal workforce particularly values assets that maintain purchasing power during economic uncertainty.

With digital currencies becoming more mainstream in 2025, some federal retirees express concerns about dollar dilution and centralization of wealth storage. Physical gold offers a trust-minimized alternative—free from issuer dependency or regulatory reinterpretation that could affect digital assets.

Military personnel and federal workers often seek safe haven assets that maintain value independently of government fiscal policies. This physical wealth storage appeals to those who understand bureaucratic limitations from professional experience and want retirement security outside institutional control.

How to Roll Over Your TSP to Noble Gold: Step-by-Step

This streamlined process transforms your federal retirement savings into physical precious metals while maintaining tax advantages and avoiding penalties.

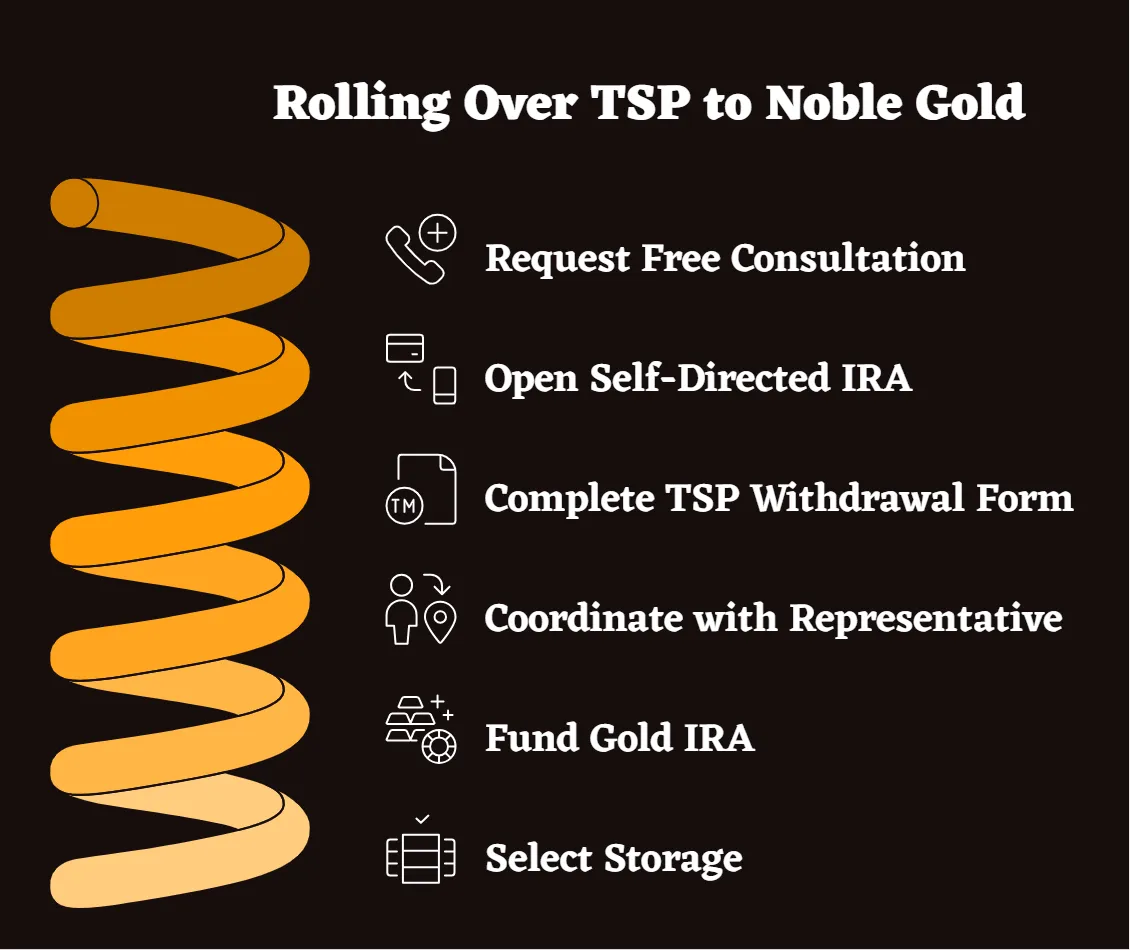

Step 1: Request a Free Consultation

Contact Noble Gold's federal employee specialists to schedule a consultation focused on TSP rollover eligibility and precious metals education. These 30-45 minute sessions cover your current TSP allocation, years of service, proximity to retirement, and diversification objectives.

Advisors explain precious metals characteristics, historical performance patterns, and storage options without pressure tactics. They review TSP withdrawal regulations and how they affect your specific situation, ensuring compliance with federal retirement system requirements.

Step 2: Open a Self-Directed IRA with Noble Gold

The company establishes your new self-directed precious metals IRA through their custodian partner, typically Equity Trust Company. This account structure allows physical metals investments while maintaining IRS compliance and tax advantages.

Account setup requires minimal paperwork and completes within 24-48 hours. Unlike your TSP's limited fund options, the self-directed IRA permits precious metals purchases, real estate investments, and other alternative assets while preserving retirement account benefits.

Step 3: Complete TSP Form TSP-70 (Full Withdrawal) or TSP-77 (Partial Withdrawal)

Request the appropriate withdrawal form from the TSP website or by calling the ThriftLine at 1-877-968-3778. Complete the direct rollover section designating your new IRA custodian as the receiving account to avoid tax consequences.

Specify the exact amount you want to transfer and ensure accurate custodian information. Direct rollovers eliminate the 60-day deadline that applies to indirect rollovers, reducing compliance risks and tax complications.

Step 4: Coordinate With Your Noble Gold Representative

Your advisor tracks the rollover status and coordinates with TSP administrators if processing delays occur. They maintain detailed records for tax and compliance purposes while providing confirmation at each step of the transfer process.

The Federal Retirement Thrift Investment Board typically processes direct rollovers within 7-14 business days, though complex cases may take longer. Your representative ensures proper documentation and follows up on any administrative issues.

Step 5: Fund the Gold IRA with Your TSP Savings

Once TSP transfers your funds to the new IRA custodian, you select IRS-approved precious metals based on your preferences and investment goals. Choose from gold, silver, platinum, and palladium options that meet purity requirements for retirement accounts.

Popular selections include American Gold Eagles, Canadian Maple Leafs, and approved bars from recognized refiners. Your advisor explains each metal's characteristics without pressuring specific choices, allowing informed decisions based on your risk tolerance.

Step 6: Select Storage and Confirm Allocation

Choose from secure depository options in Texas, Delaware, or Canada through International Depository Services. Many federal retirees based in Texas prefer storing hard assets close to home, and the company's partnership with IDS in Dallas offers that regional peace of mind.

All locations provide segregated storage where your specific metals remain separate under your name rather than commingled with other investors' assets. Comprehensive insurance through Lloyd's of London protects your custodian-controlled assets independently of market conditions.

Receive photographic confirmation once your metals arrive at the chosen facility. This transparency exceeds what's possible with institutional retirement plans, providing tangible proof of your alternative IRA's physical existence and secure storage.

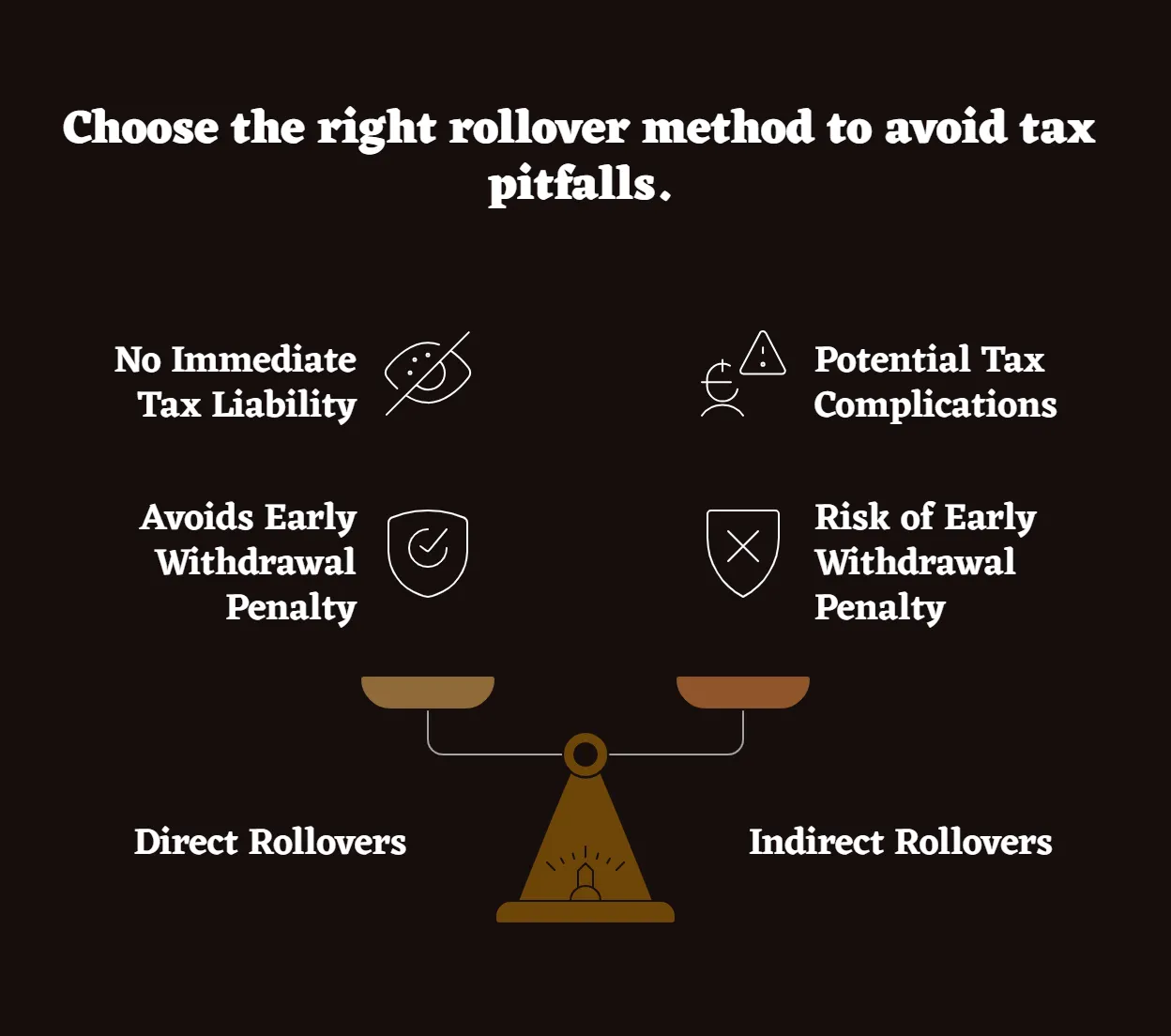

Will I Pay Penalties or Taxes on a TSP Rollover?

Understanding tax implications helps federal employees execute rollovers without triggering unnecessary penalties or immediate tax liability.

Conditions That Trigger Penalties (And How to Avoid Them)

Direct rollovers from TSP to precious metals IRAs generate no immediate tax liability when executed correctly. The trustee-to-trustee transfer maintains your funds' tax-advantaged status throughout the process, avoiding the 10% early withdrawal penalty [2].

Indirect rollovers where you receive funds directly create potential tax complications. You must deposit the full amount into your new IRA within 60 days, or the distribution becomes taxable income subject to early withdrawal penalties if you're under age 59½.

Rolling over Required Minimum Distributions or attempting to transfer after-tax contributions can trigger penalties. Your advisor helps identify these situations and recommends appropriate strategies to maintain tax compliance.

Age-Based Rules for Federal Employees

Federal employees who reach age 59½ can make "age-based in-service withdrawals" from their TSP while continuing employment. This allows partial rollovers without separating from federal service, providing flexibility for phased retirement planning [1].

Employees over age 73 must begin taking Required Minimum Distributions from traditional TSP accounts. These distributions can be rolled into precious metals IRAs if not needed for living expenses, allowing continued tax-deferred growth.

Separation from federal service at any age eliminates TSP rollover restrictions. Whether through retirement, resignation, or career change, departing employees gain full control over their TSP accounts for rollover purposes.

Roth TSP vs Traditional TSP: Tax Considerations

Traditional TSP rollovers to traditional precious metals IRAs maintain tax-deferred status. You'll pay ordinary income tax on distributions during retirement, but the rollover itself creates no immediate tax event.

Roth TSP funds must transfer to Roth precious metals IRAs to preserve tax-free growth and distribution advantages. These transfers maintain the five-year holding rule and other Roth account characteristics.

Converting traditional TSP funds to Roth precious metals IRAs triggers immediate taxation on the converted amount. This strategy benefits younger federal workers expecting higher tax rates in retirement but requires careful planning to manage current-year tax liability.

Why Federal and Military Investors Trust Noble Gold

The company's specialized focus on government workers creates unique advantages for federal employees and military personnel seeking precious metals diversification.

Experience With Federal Benefits & TSP Accounts

Noble Gold maintains dedicated expertise in federal retirement systems that general precious metals dealers often lack. Their advisors understand TSP withdrawal rules, timing requirements, and tax implications specific to government workers.

Many clients are veterans or current federal employees who appreciate working with representatives familiar with military and government service. This shared background creates natural communication efficiency and trust-building throughout the rollover process.

The company's educational approach emphasizes long-term wealth preservation rather than short-term speculation, aligning with federal employees' typically conservative investment philosophies and retirement planning horizons.

Segregated Storage & Conservative Investment Approach

All precious metals storage utilizes segregated arrangements where your specific coins and bars remain separate under your name. This approach eliminates commingling risks and provides clear ownership documentation for tax and estate planning purposes.

Storage facilities in Texas, Delaware, and Canada offer geographic diversification and appointment-based visitation rights. Comprehensive insurance coverage protects against loss or damage independently of the company's business operations.

The focus on IRS-approved bullion rather than collectible coins ensures your investment goes toward precious metals content rather than numismatic premiums. This strategy aligns with wealth preservation objectives rather than speculative collecting.

Testimonials From Government Retirees

Federal employee clients frequently praise the company's patient, educational approach and transparent fee structure. Many specifically mention feeling comfortable with representatives who understand government service and retirement planning challenges.

Military retirees often highlight the value of working with a veteran-owned company that appreciates their service background and financial planning needs. The straightforward communication style resonates with those accustomed to direct, professional interactions.

Government workers consistently mention peace of mind from knowing their retirement assets exist as physical objects in secure facilities rather than digital account balances subject to market volatility or institutional risks.

Common Questions About TSP to Noble Gold Rollovers

Federal employees frequently ask specific questions about moving TSP funds into precious metals IRAs through the company's specialized process.

Can I move just part of my TSP?

Yes, federal employees can transfer any amount from their TSP to a precious metals IRA, from several thousand dollars to entire account balances. Partial rollovers allow testing the process while maintaining TSP growth potential for remaining funds.

Many government workers start with smaller amounts to gain comfort with precious metals ownership before making larger transfers. This approach provides dollar-cost averaging benefits and reduces decision-making pressure around optimal timing.

What happens if I've already retired from government work?

Retired federal employees maintain full control over their TSP accounts for rollover purposes. Separation from service eliminates in-service withdrawal restrictions, providing maximum flexibility for precious metals diversification strategies.

Retirees can take advantage of direct rollover benefits without employment-related limitations. The process remains identical whether you're currently employed or have separated from federal service.

Can I roll Roth TSP funds into a Gold IRA?

Roth TSP funds can transfer to Roth precious metals IRAs, preserving tax-free growth and distribution advantages. These transfers maintain the five-year holding rule and other Roth account characteristics essential for tax-free retirement income.

The rollover process for Roth accounts mirrors traditional TSP transfers but requires careful attention to account type matching. Your advisor ensures proper custodial arrangements to maintain Roth account benefits throughout the process.

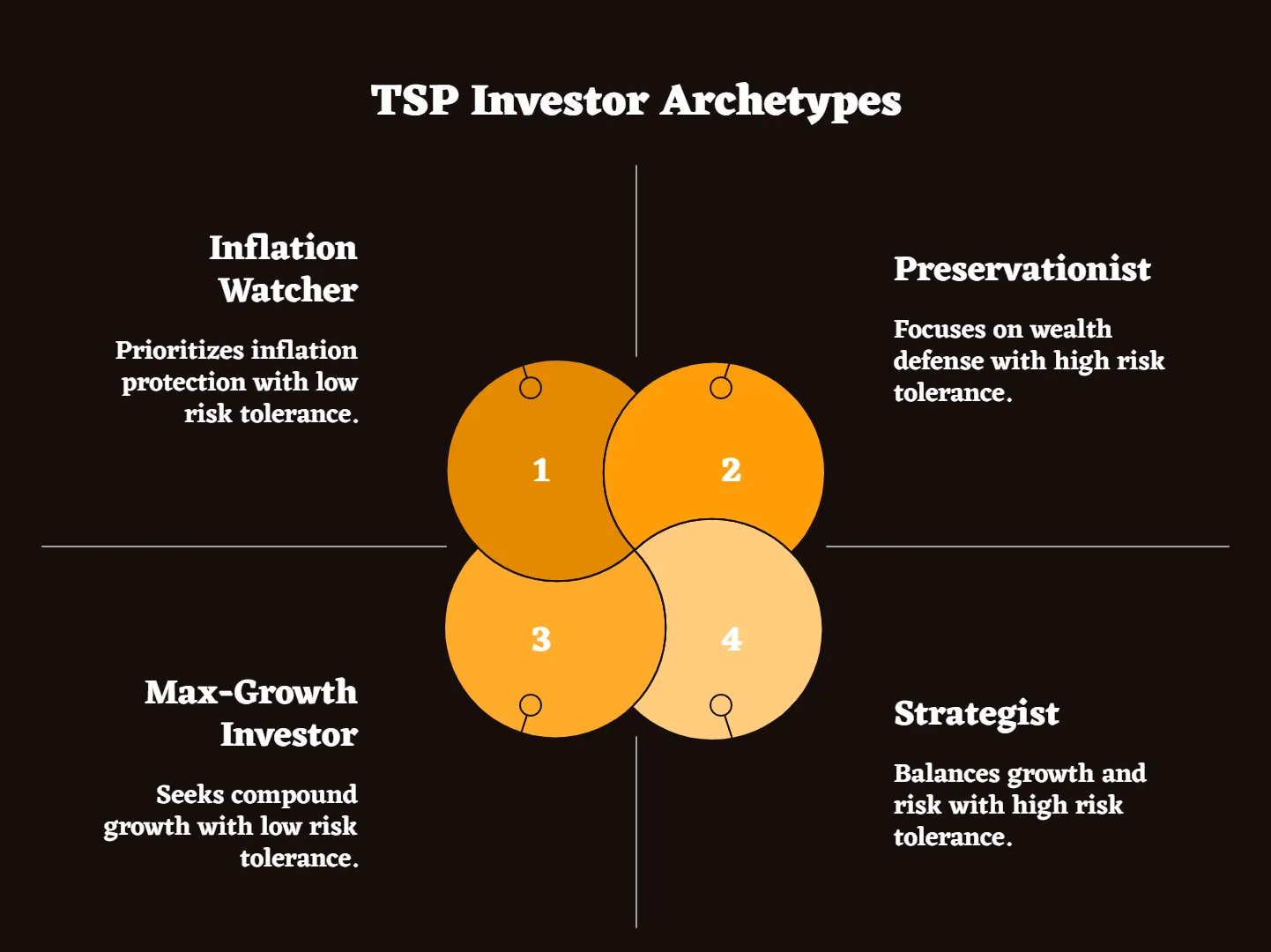

TSP Rollover Archetypes: What Kind of Federal Investor Are You?

Understanding your investor profile helps determine whether a precious metals rollover aligns with your retirement strategy and risk tolerance.

The Preservationist: Nearing retirement, focused on wealth defense over growth. Values gold-backed retirement strategies for stability and inflation protection during the distribution phase.

The Inflation Watcher: Concerned about rising prices eroding real returns from government securities. Prefers hard assets that maintain purchasing power regardless of monetary policy changes.

The Strategist: Splits TSP allocations between traditional growth funds and alternative asset classes to maximize portfolio optionality and reduce concentration risk.

The Max-Growth Investor: Early career federal employee who remains in TSP lifecycle funds for compound growth potential, viewing precious metals as premature for their timeline.

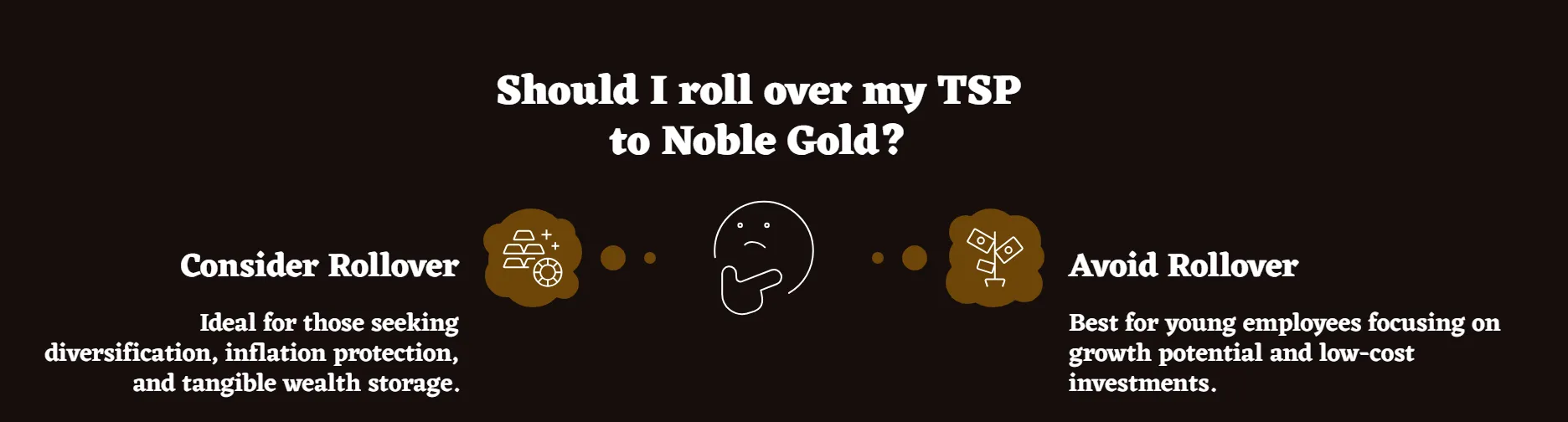

Final Thoughts: Should You Roll Over Your TSP to Noble Gold?

The decision to roll TSP funds into a self-directed metals account depends on your individual circumstances, risk tolerance, and retirement planning objectives.

When It Makes Sense (And When It Doesn't)

TSP rollovers to precious metals work best for federal employees seeking portfolio diversification beyond traditional paper assets. This strategy particularly benefits those concerned about inflation protection and institutional stability.

Consider precious metals allocation if you're approaching retirement and want assets that maintain value independently of government fiscal policies. The strategy also appeals to those seeking tangible wealth storage for estate planning purposes.

Avoid rollovers if you're early in your career and can benefit from TSP's low-cost growth potential. Young federal employees typically benefit more from aggressive growth strategies than conservative precious metals allocation.

Comparing a TSP-Only vs Diversified Retirement Portfolio

Maintaining your entire retirement savings in TSP provides simplicity and low costs but concentrates risk in government-sponsored investments. Diversification with precious metals adds inflation protection and reduces dependence on paper assets.

A balanced approach might involve keeping core TSP funds while rolling a portion into precious metals for diversification. This strategy provides both growth potential and stability characteristics across different economic environments.

Next Steps to Protect Your Retirement Savings

Schedule a consultation with federal employee specialists to explore your specific situation and rollover eligibility. These educational sessions provide personalized guidance without obligation or pressure tactics.

Request their comprehensive information package covering precious metals characteristics, storage options, and tax implications. This educational approach helps you make informed decisions based on your unique circumstances and retirement goals.

While the company specializes in federal rollovers, federal employees may wish to compare multiple providers or consult TSP-approved financial advisors to explore a full range of retirement options. Even as digital currencies emerge as modern cash alternatives, many federal and military investors seek tangible, policy-resistant wealth storage that exists outside digital custody systems altogether.

Disclosure: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult a licensed financial advisor before making investment decisions. Some links in this article may be affiliate links, meaning we may earn a small commission if you purchase through them—at no additional cost to you. Investing in precious metals and other alternative assets involves risk, and past performance does not guarantee future results. Do your own due diligence before making any investment decisions.

References

- Federal Retirement Thrift Investment Board. "Understanding TSP Withdrawals." Thrift Savings Plan, 2025.

- IRS. "Retirement Plan Rollovers." Internal Revenue Service, 2025.

- World Gold Council. "Gold Investment Research." World Gold Council, 2025.

- Noble Gold Investments. "Federal Employee Guide." Noble Gold, 2025.

- Federal Retirement Thrift Investment Board. "In-Service Withdrawals." TSP, 2025.

- IRS. "Required Minimum Distributions." Internal Revenue Service, 2025.

- Better Business Bureau. "Noble Gold Reviews." BBB, 2025.