.svg)

Many investors assume precious metals retirement accounts require massive upfront investments. This misconception keeps countless Americans from exploring physical bullion IRAs as a portfolio diversification strategy.

The reality? Entry points vary more than most realize. While some providers like Noble Gold accept accounts starting around $2,000, others like Birch Gold set minimums at $10,000. The growth strategies, cost management principles, and storage decisions remain consistent regardless of your starting point.

Modern self-directed IRA providers recognize that most investors prefer testing new strategies before committing larger sums This approach makes sense for federal employees transitioning from TSP accounts, engineers evaluating portfolio alternatives, and business leaders seeking non-correlated assets alongside traditional holdings.

Key Takeaways

- Starting points from $2,000 to $10,000 provide accessible entry into physical precious metals IRAs

- Annual contributions and selective rollovers create multiple pathways for account expansion

- Flat-fee structures favor growing accounts over percentage-based models

- Strategic metal allocation between gold, silver, and platinum optimizes both value and diversification

Pros and Cons of Starting a Small Gold IRA

Pros

- Low Entry Point — Accessible minimum makes physical precious metals IRAs available to everyday investors

- Diversification — Adds non-correlated assets alongside stocks, bonds, and TSP funds

- Inflation Hedge — Gold and silver have historically held purchasing power during inflationary cycles

- Flat Fees — Same annual costs whether your account holds $10K or $100K

- Scalable — Easy to grow through annual IRA contributions and rollovers

Cons

- Fixed Costs Impact Small Accounts — $180/year in fees represents a higher percentage of a $10K balance

- No Dividends or Yield — Metals preserve wealth but don't generate income

- Liquidity Takes Time — Selling metals for cash usually takes several business days

- Price Volatility — Gold can swing 10–20% in the short term

- RMD Requirements — After age 73, distributions may force partial liquidations

Thinking about starting small? Even a $10K metals IRA can compound into meaningful diversification—provided you understand costs, storage, and IRS rules. Providers like Birch Gold (case study below) make it possible without six-figure commitments.

Why Investors Start Small With Gold IRAs

Most investors overlook the psychological advantage of starting modestly with alternative assets. Whether starting with $2,000 or $10,000, smaller allocations allow thorough evaluation of custodian services, storage arrangements, and metal selection without major portfolio disruption.

Modest Entry Points in Today's Economy

Federal employees and private sector professionals often maintain disciplined budgets during uncertain economic periods. Allocating amounts in the four- to five-figure range represents a meaningful commitment without jeopardizing other financial objectives. This amount provides exposure to precious metals price movements while maintaining flexibility for portfolio adjustments.

Veterans transitioning from military service frequently appreciate the measured approach. Rather than rushing into large positions, they can evaluate how physical bullion IRAs complement existing benefits and retirement planning strategies.

Small Accounts vs. High-Minimum Competitors

Several precious metals IRA providers such as Augusta Precious Metals require $50,000 or higher minimums, effectively excluding many potential investors. These concierge-focused firms target ultra-high-net-worth clients seeking white-glove service and extensive hand-holding throughout the process.

Lower-minimum providers serve investors who value accessibility over premium service layers. Engineers and STEM professionals often prefer straightforward processes with clear fee structures rather than elaborate consultation services that inflate costs.

Growing a Modest Precious Metals IRA Over Time

Systematic growth transforms modest initial investments into substantial alternative asset positions. Most successful precious metals IRA investors follow disciplined approaches rather than sporadic large additions.

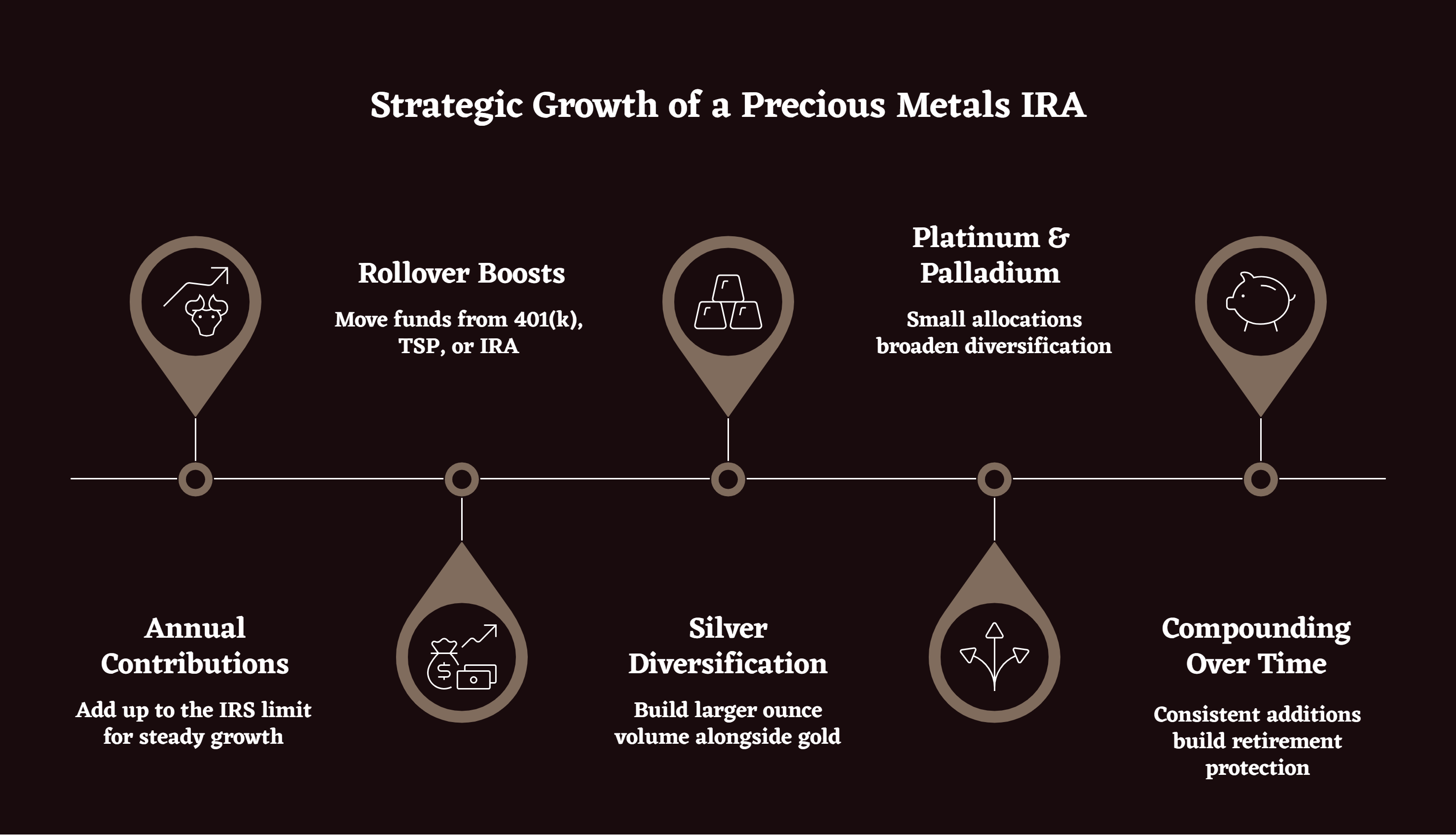

Growth Strategies for a Small Gold IRA

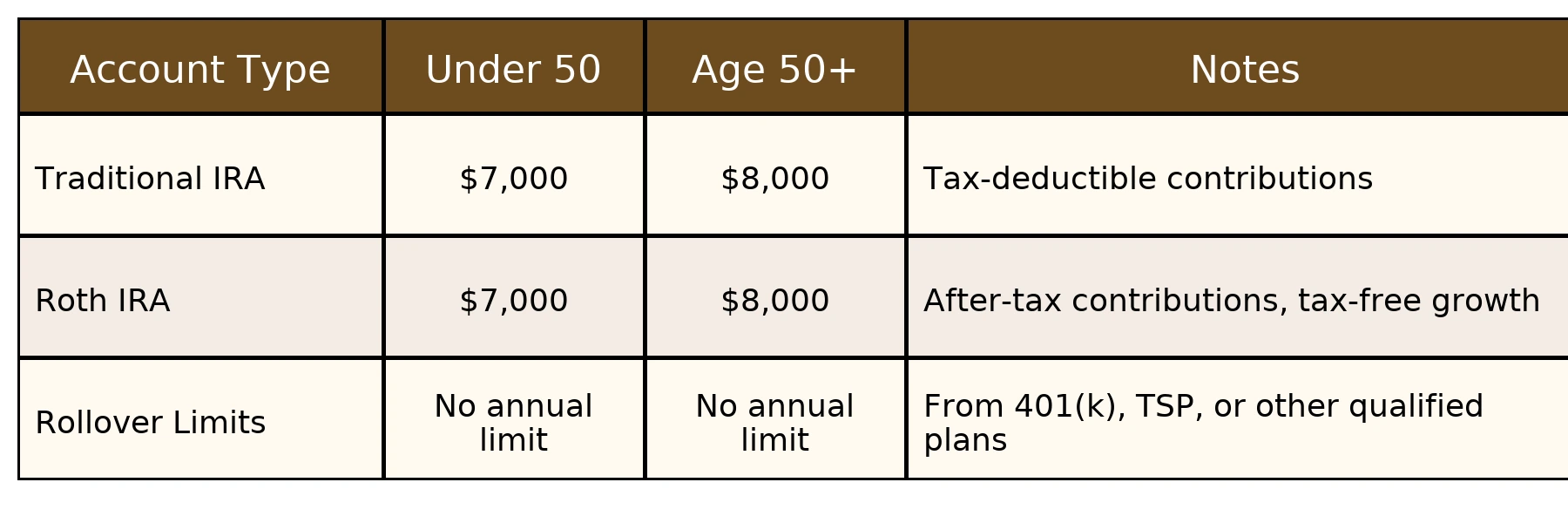

- Annual Contributions — Add up to the IRS limit ($7K–$8K depending on age) for steady year-over-year growth

- Rollover Boosts — Move part of a 401(k), TSP, or IRA into metals for faster scaling than contributions alone

- Silver Diversification — Use silver's lower entry cost to build larger ounce volume alongside gold

- Platinum & Palladium — Small allocations (3–10%) broaden diversification beyond gold/silver

- Flat-Fee Advantage — Fixed custodian/storage fees mean costs shrink as balances grow

- Compounding Over Time — Consistent additions plus long-term stability build meaningful retirement protection

Annual Contribution Strategies (Traditional vs. Roth)

The choice between Traditional and Roth precious metals IRAs affects both current tax situations and long-term growth potential. Federal employees earning steady salaries often benefit from Traditional contributions, reducing current taxable income while deferring taxes until retirement.

Business leaders with variable income may prefer splitting contributions. Contributing $3,500 to Traditional and $3,500 to Roth accounts provides both immediate tax relief and tax-free growth potential. This strategy works particularly well for professionals expecting higher tax brackets in retirement.

Catch-up contributions allow investors over 50 to add an extra $1,000 annually. Veterans and engineers approaching retirement often maximize these additional contributions to accelerate precious metals accumulation during peak earning years.

Diversifying with Silver, Platinum, and Palladium

Silver often provides better ounce accumulation for modest budgets. With silver trading roughly 80:1 against gold, investors can acquire larger quantities of physical metal per dollar invested. Many successful precious metals IRA holders maintain 60-70% gold and 30-40% silver allocations.

Platinum offers different correlation patterns than gold or silver. Industrial demand from automotive and technology sectors creates price dynamics independent of monetary concerns. Small platinum allocations—perhaps 5-10% of total metals holdings—provide additional diversification benefits.

Palladium remains the most volatile precious metal approved for IRA inclusion. Its primary use in automotive catalytic converters creates supply constraints during economic expansion periods. Conservative investors often limit palladium to 3-5% of total precious metals allocations.

When to Add Cash vs. Rollovers for Growth

Annual cash contributions provide steady, predictable account growth. Professionals with stable employment can automate monthly transfers, smoothing out metal price fluctuations through dollar-cost averaging. This approach works well for systematic accumulation over 10-15 year periods.

Rollovers create opportunities for substantial account expansion during career transitions. Leaving one employer and joining another often triggers 401(k) rollover decisions. Moving even partial amounts—perhaps 20-30% of retirement savings—into precious metals IRAs can dramatically accelerate alternative asset accumulation.

TSP holders face unique considerations when evaluating partial rollovers. Federal employees must weigh TSP's low-cost index fund options against precious metals' inflation protection benefits. Many choose modest 10-15% allocations to metals while maintaining TSP participation for continued growth potential.

Managing Costs With a Smaller Account

Fee structures significantly impact small account economics. Understanding the mathematics behind different pricing models helps investors make informed decisions about provider selection and growth strategies.

Flat Annual Fees vs. Percentage-Based Fees

Most precious metals IRA providers charge flat annual fees ranging from $150-$250. These cover custodian services, storage, and insurance regardless of account size. For a $10,000 account paying $180 annually, fees represent 1.8% of holdings.

As accounts grow, flat fees become increasingly advantageous. That same $180 fee represents only 0.72% of a $25,000 account and just 0.36% of a $50,000 balance. This mathematical reality favors investors committed to systematic growth over time.

For federal employees, this means your small $10K account isn't penalized compared to a $50K+ investor—you both pay the same flat fee.

Percentage-based fee structures work differently. Providers charging 0.5-1.0% annually maintain consistent percentage costs but create higher absolute dollar amounts as accounts grow. A 0.75% annual fee costs $75 on a $10,000 account but $375 on a $50,000 balance.

How Birch's Structure Supports Smaller Investors

Birch Gold Group exemplifies the flat-fee approach that benefits growing accounts. Their $180 annual fee structure covers storage at secure depositories, custodian services, and comprehensive insurance regardless of account value. This pricing model particularly advantages investors planning systematic growth from modest starting points.

Federal employees and veterans often appreciate Birch's educational approach combined with accessible minimums. Companies like Noble Gold offer similar structures, though with different service emphases. Rather than requiring extensive upfront commitments, these providers allow investors to develop familiarity with precious metals IRAs while maintaining reasonable cost structures.

IRS Rules for Small Metals IRAs

Understanding contribution limits and distribution requirements helps investors plan effective long-term strategies. Recent changes to required minimum distribution rules affect precious metals IRAs differently than traditional retirement accounts.

IRS Contribution Limits and Rollover Eligibility in 2025

Here's a quick table of 2025 contribution limits by IRA type:

Rollover eligibility extends beyond traditional 401(k) accounts. Federal employees can move TSP funds using Form TSP-70 for partial distributions or TSP-77 for full account transfers. These rollovers don't count against annual contribution limits, allowing substantial precious metals IRA funding during career transitions.

Required Minimum Distributions (RMDs) to Plan For

Traditional precious metals IRAs face RMD requirements beginning at age 73. Unlike stock-based accounts where partial share sales provide flexibility, metals IRAs require either partial metal liquidation or in-kind distributions of physical coins or bars.

Roth precious metals IRAs avoid RMDs during the original owner's lifetime. This advantage allows continued accumulation and metals price appreciation without forced distribution timing. Inherited Roth accounts face different rules requiring distributions over 10-year periods.

Planning for RMDs involves maintaining sufficient liquidity outside precious metals IRAs. Many successful investors keep 2-3 years of planned RMD amounts in cash or short-term investments, avoiding forced metals sales during unfavorable market conditions.

Risks and Rewards of Starting Small

Every investment strategy involves trade-offs between growth potential and preservation focus. Small precious metals IRAs offer unique advantages while presenting specific challenges requiring careful consideration.

Liquidity and Storage Trade-offs

Physical metals stored in approved depositories provide security and IRS compliance but reduce immediate liquidity compared to electronically traded assets. Selling metals typically requires 3-5 business days for completion, including transportation and processing time.

Emergency cash needs should be met through separate savings accounts rather than precious metals IRAs. Financial planners often recommend maintaining 6-12 months of expenses in liquid accounts before considering alternative asset allocations.

Storage trade-offs involve security versus cost considerations. Segregated storage provides individual identification of specific coins and bars but typically costs more than commingled storage arrangements. Investors with growing accounts often start with commingled storage and upgrade to segregated arrangements as balances increase.

Inflation Hedge Even with Modest Holdings

Historical data demonstrates precious metals' purchasing power preservation during inflationary periods. A 5-15% allocation to metals within overall retirement planning can provide meaningful protection against currency devaluation without overwhelming portfolio allocation.

Engineers and business leaders often appreciate the mathematical approach to inflation hedging. Rather than attempting to time major economic shifts, systematic metals accumulation provides steady protection against gradual purchasing power erosion over 20-30 year periods.

Smart Storage Choices for Growing Accounts

Storage decisions impact both security and cost structures as precious metals IRAs grow over time. Understanding the differences between storage options helps investors make informed choices aligned with their specific circumstances.

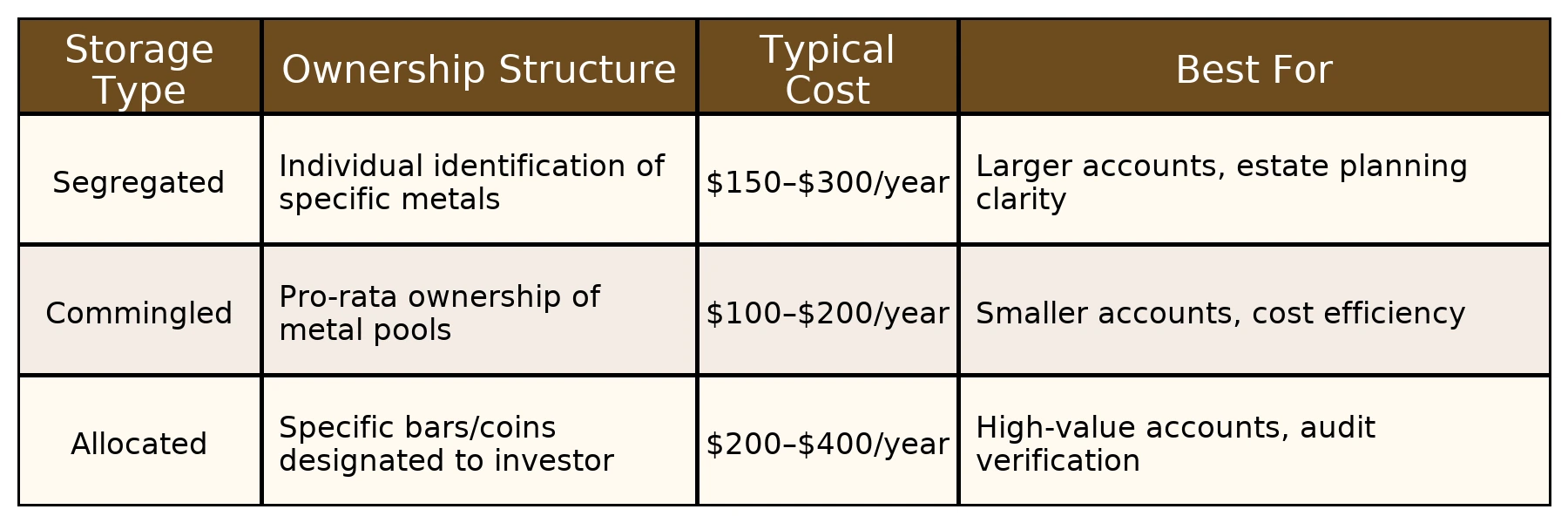

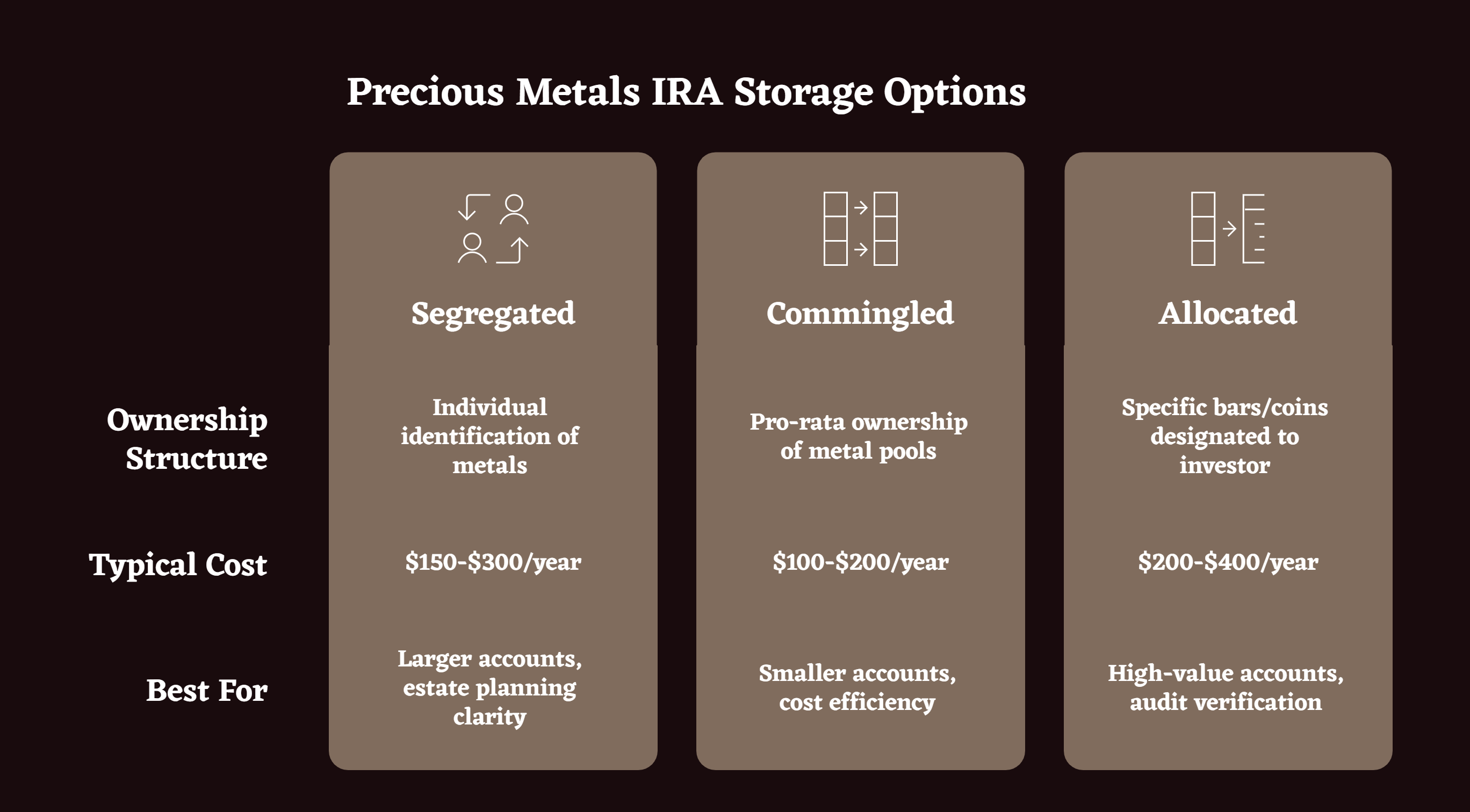

Storage Options at a Glance

- Segregated Storage — Your exact coins and bars are kept separate under your name; higher cost but maximum clarity and estate planning ease

- Commingled Storage — Metals are pooled with others but ownership records track your share; more affordable for small accounts

- Allocated Storage — Specific bars or coins assigned to you within a vault; best for high-value accounts that require audit-level verification

Storage Options Comparison

Here's a breakdown of storage types for precious metals IRAs:

Examples of U.S. Depositories

Delaware Depository serves as a leading storage facility with comprehensive security systems and insurance coverage. Located in Wilmington, Delaware, this facility provides both segregated and commingled storage options for precious metals IRAs.

Texas Precious Metals Depository (Dallas) offers regional diversification with full insurance coverage and regular audit services ensuring accurate record-keeping.

IDS Canada offers international storage options for investors seeking geographic diversification beyond U.S. borders. While less common for small accounts, some investors prefer international storage as accounts grow substantially.

Why Federal Employees Often Prefer Segregated Storage

Federal employees and veterans frequently choose segregated storage despite higher costs. Their security clearance backgrounds create familiarity with verification procedures and documentation requirements that segregated storage provides.

Estate planning considerations also influence storage choices. Segregated storage simplifies inheritance processes by providing clear identification of specific metals belonging to individual accounts. This clarity proves valuable for surviving spouses navigating complex estate administration procedures.

FAQs

Is $10K enough to start a precious metals IRA?

Yes, $10,000 provides sufficient entry into physical precious metals IRAs. This amount allows meaningful exposure to gold and silver price movements while maintaining reasonable cost structures relative to account size.

What's the fastest way to grow a low entry point Gold IRA?

Combining annual IRA contributions with partial rollovers from existing retirement accounts creates the fastest growth path. Many investors add $7,000-$8,000 annually while moving portions of 401(k) or TSP funds during job transitions.

Which metals are best for small accounts?

Gold provides stability while silver offers greater ounce accumulation per dollar invested. Most small account holders start with 60-70% gold and 30-40% silver, adding platinum or palladium as balances grow beyond $25,000.

Can I add to my account later with cash or rollovers?

Annual IRA contributions up to $7,000-$8,000 provide systematic growth opportunities. Rollovers from 401(k), TSP, or other qualified plans offer additional funding sources without contribution limit restrictions.

Do smaller accounts get treated differently by providers?

Reputable providers offer identical services regardless of account size. Storage, insurance, and custodian services remain consistent whether accounts hold $10,000 or $100,000 in precious metals.

Does storage choice matter more for small balances?

Commingled storage typically makes more sense for accounts under $25,000 due to lower costs. Segregated storage becomes more attractive as accounts grow and estate planning considerations become more complex.

How long before a $10,000 USD initial account feels substantial?

With consistent annual contributions and occasional rollovers, accounts often reach $25,000-$30,000 within 3-5 years. At these levels, flat annual fees represent smaller percentages of total holdings.

Can I store metals at home?

No—IRA metals must remain with approved depositories to maintain tax-advantaged status. Home storage disqualifies accounts from IRA benefits and creates immediate tax consequences for all holdings.

Is Starting Small With a Gold IRA Worth It?

Starting small with precious metals IRAs provides practical entry into alternative asset investing without overwhelming existing financial strategies. The starter low minimum opens opportunities for systematic growth through annual contributions, selective rollovers, and strategic diversification across multiple metals.

Federal employees, veterans, engineers, and business leaders often find measured approaches align with their risk management preferences. Rather than making dramatic portfolio changes, modest precious metals allocations provide inflation protection and diversification benefits while maintaining overall financial stability.

Successful small account growth requires understanding fee structures, storage options, and IRS regulations affecting contributions and distributions. Investors who master these fundamentals position themselves for meaningful wealth preservation as accounts mature over 15-20 year periods.

Disclaimer: This article provides educational information only and does not constitute financial advice. Consult qualified financial professionals before making investment decisions. Precious metals investments involve risks including price volatility and storage considerations.

References

[1] Internal Revenue Service. "Retirement Plans FAQs regarding IRAs." Accessed March 2025.

[2] Federal Retirement Thrift Investment Board. "TSP-70: Request for Full Withdrawal." Accessed March 2025.

[3] U.S. Bureau of Labor Statistics. "Consumer Price Index Summary." Accessed March 2025.

[4] Delaware Depository Service Company. "Storage Services Overview." Accessed March 2025.

[5] Commodity Futures Trading Commission. "Customer Advisory: Precious Metals Fraud." Accessed March 2025.

[6] Investment Company Institute. "The Economics of Providing 401(k) Plans." Accessed March 2025.

[7] Federal Trade Commission. "Investing in Gold." Accessed March 2025.

[8] Internal Revenue Service. "IRA Deduction Limits." Publication 590-A. Accessed March 2025.

[9] Government Accountability Office. "Federal Retirement: Better Information and Guidance Could Help Federal Employees." Accessed March 2025.