.svg)

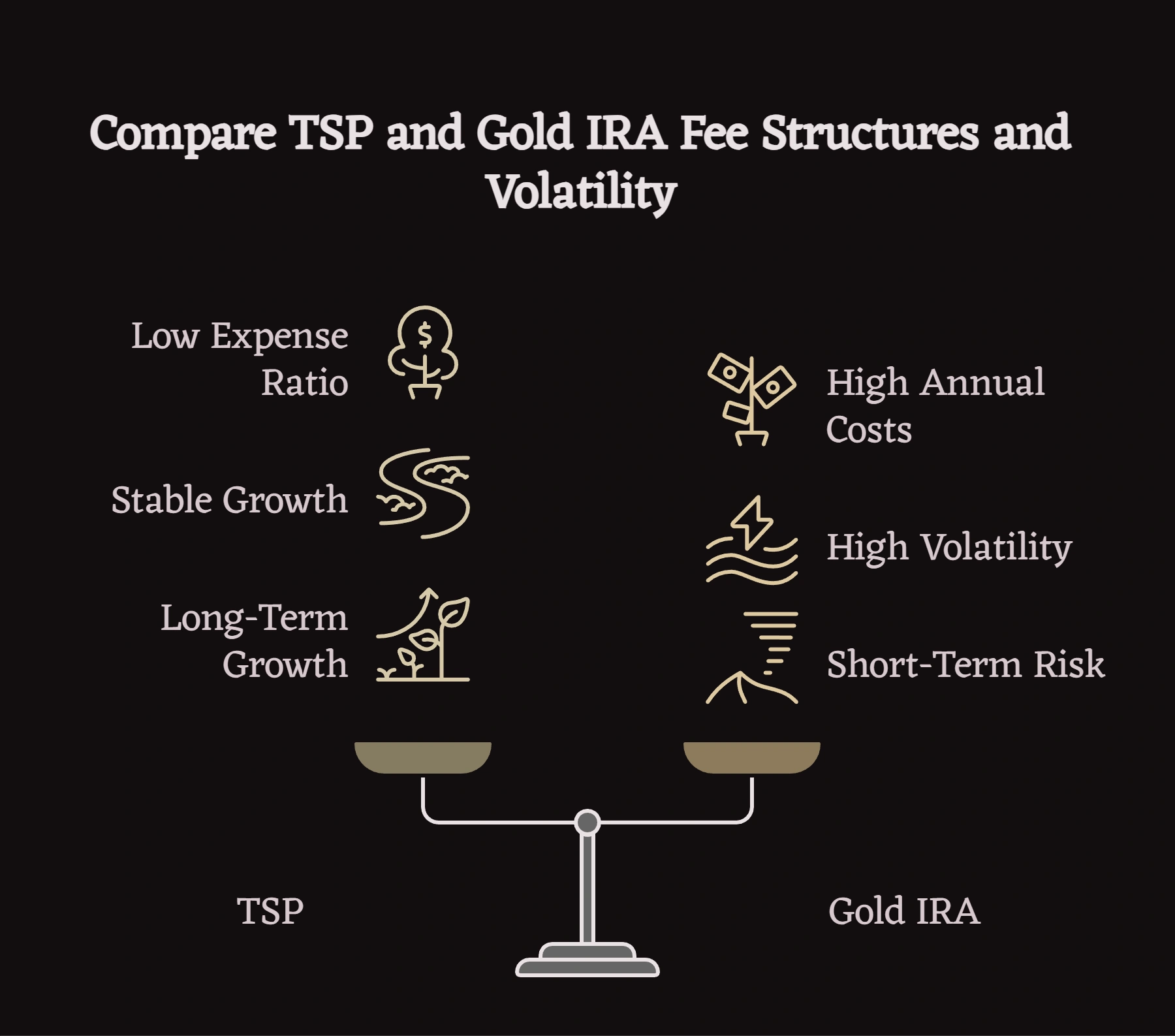

Federal employees under 50 with TSP balances exceeding $100,000 may benefit from gold IRA diversification if fee structures align with long-term growth projections and inflation hedge objectives. Smaller balances below $100,000 typically face disproportionately high relative costs—averaging 1.2-2.1% annually including custody, storage, and transaction fees—that erode compounding returns compared to TSP's 0.042% expense ratio. The decision hinges on whether purchasing power protection justifies the $738+ annual fee differential per $100,000, acceptance of 15% volatility gold introduces, and comfort with reduced liquidity versus TSP's daily access.

Last updated: February 2026

Key Takeaways

- TSP balances over $100,000 make gold IRA fees more manageable—below this threshold, 1.2-2.1% annual costs significantly impact long-term returns

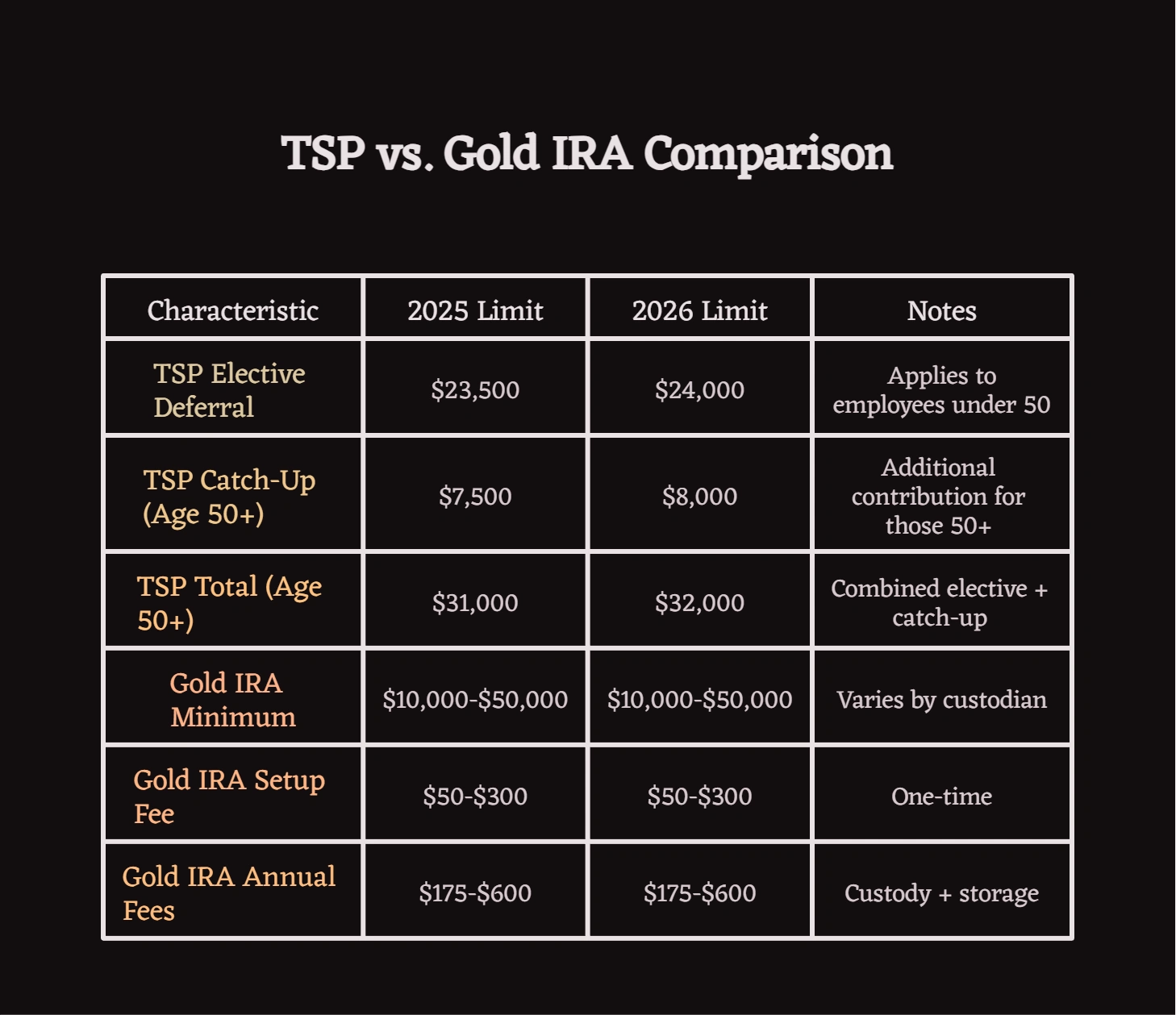

- 2025 TSP contribution limit: $23,500 (rising to $24,000 in 2026); gold IRA minimums typically $10,000-$50,000 depending on custodian

- The TSP Modernization Act permits in-service withdrawals enabling partial rollovers to self-directed IRAs without separation from federal employment

- Fee differential compounds substantially: $150,000 in TSP at 0.042% grows to approximately $430,000 in 25 years versus $295,000 in gold IRA at 1.5% fees

Understanding Early-Career TSP Diversification Questions

Federal employees in mid-career—typically with 5-20 years of service and growing TSP balances—face a specific diversification question that differs from both early-career savers and pre-retirees. They have accumulated sufficient capital that alternative assets become mathematically viable, yet they retain decades of compounding time where fee impacts multiply significantly.

This creates tension between two valid concerns: protecting purchasing power over 20-30 year horizons where inflation compounds relentlessly, and preserving maximum capital growth through ultra-low-cost index exposure during peak earning and contribution years.

The fundamental question of whether federal employees can hold physical gold in retirement accounts involves IRS compliance requirements, storage rules, and dealer pricing mechanics that apply regardless of age—the under-50 consideration adds fee impact analysis and time horizon evaluation to that foundation.

Why This Question Keeps Coming Up

Federal employees in technical and analytical roles—engineers, IT professionals, data analysts, cybersecurity specialists—increasingly encounter gold IRA marketing through professional networks, financial advisor outreach, and peer discussions about inflation protection. Many have studied the mathematics of compound interest closely enough to recognize both the power of low fees and the genuine risk of purchasing power erosion.

This creates a population of skeptical but intellectually curious savers who want analytical frameworks rather than promotional claims or fear-based marketing. They understand TSP's cost advantage but question whether it adequately addresses inflation scenarios where nominal preservation doesn't equal real wealth protection.

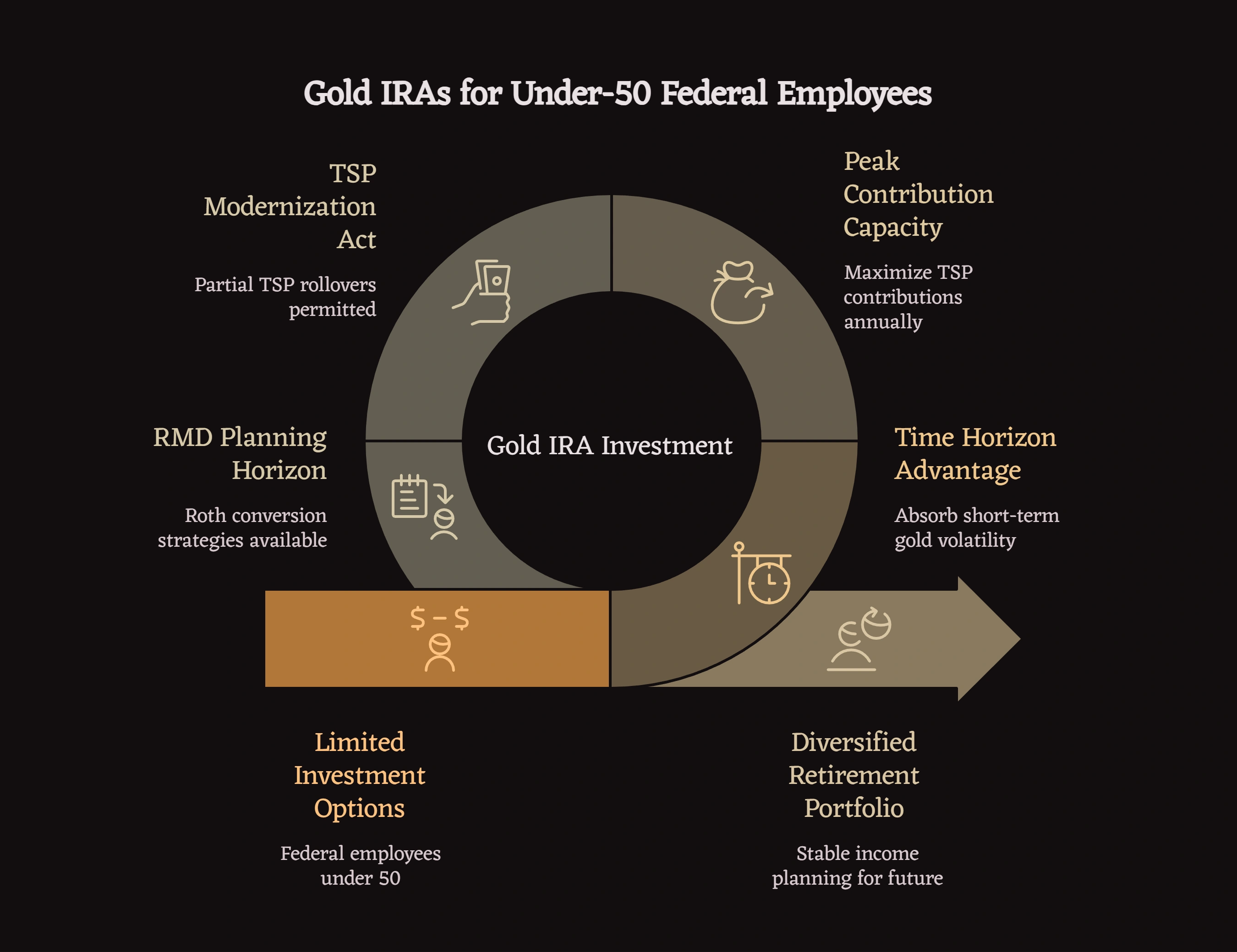

What Makes the Under-50 Federal Employee Situation Unique?

Federal employees under 50 evaluating gold IRAs face circumstances distinct from both private sector workers and federal employees approaching retirement.

Time horizon advantage: With 15-30 years until retirement, these employees can absorb short-term gold volatility that would devastate near-retirees who need stable income planning.

Peak contribution capacity: Mid-career federal employees typically earn GS-11 through GS-15 salaries supporting maximum TSP contributions—$23,500 in 2025, rising to $24,000 in 2026. This creates substantial annual inflows where even small percentage differences in fees compound dramatically.

TSP Modernization Act flexibility: Unlike pre-2019 rules, current FERS participants can execute in-service withdrawals permitting partial TSP rollovers to self-directed IRAs without separation from federal employment. This enables gold IRA funding without disrupting core TSP accumulation.

RMD planning horizon: Federal employees under 50 won't face Required Minimum Distributions for 20+ years. This extended timeline permits Roth conversion strategies and tax diversification approaches unavailable to employees approaching age 73.

The Fee Mathematics: When Do Gold IRAs Make Sense?

The central question for federal employees under 50 is whether gold IRA fees justify the inflation hedge and diversification benefits.

TSP Cost Structure

TSP funds carry a combined expense ratio of 0.042%—among the lowest of any retirement plan available to American workers. For a $100,000 balance, this equals $42 annually.

This cost structure compounds favorably over decades. A $100,000 TSP allocation growing at 7% annually reaches approximately $761,000 in 30 years. The same balance with 1.5% annual fees (reducing net return to 5.5%) reaches approximately $530,000—a $231,000 difference from fees alone.

Gold IRA Cost Structure

Self-directed IRAs holding physical precious metals typically incur:

- Setup fees: $50-$300 (one-time)

- Annual custodial fees: $75-$300

- Storage fees: $100-$300 annually

- Transaction costs: 4-8% spreads on purchases (legitimate dealers)

- Total annual ongoing costs: $780 average per $100,000

For a $50,000 balance, these same dollar-denominated fees represent 1.56% annually before any transaction costs. For a $200,000 balance, they represent 0.39% annually—still nearly 10x TSP's expense ratio but more manageable proportionally.

The Break-Even Analysis

Gold prices must outperform TSP allocations by approximately 0.74% annually just to offset the fee differential on $100,000 balances. Over 30-year horizons, this compounds to meaningful differences in terminal wealth.

When gold IRAs may make mathematical sense:

- TSP balances exceed $150,000 where fees become more manageable proportionally

- Investor accepts 15% annual volatility in exchange for inflation hedge characteristics

- Time horizon exceeds 15 years permitting recovery from gold bear markets

- Allocation represents 5-10% of total retirement assets, not wholesale conversion

When gold IRAs face mathematical headwinds:

- TSP balances below $75,000 where fixed fees create excessive drag

- Investor needs liquidity within 5-10 years where gold's volatility creates timing risk

- Allocation would exceed 15% of retirement assets, concentrating risk

- Investor prioritizes nominal preservation over purchasing power protection

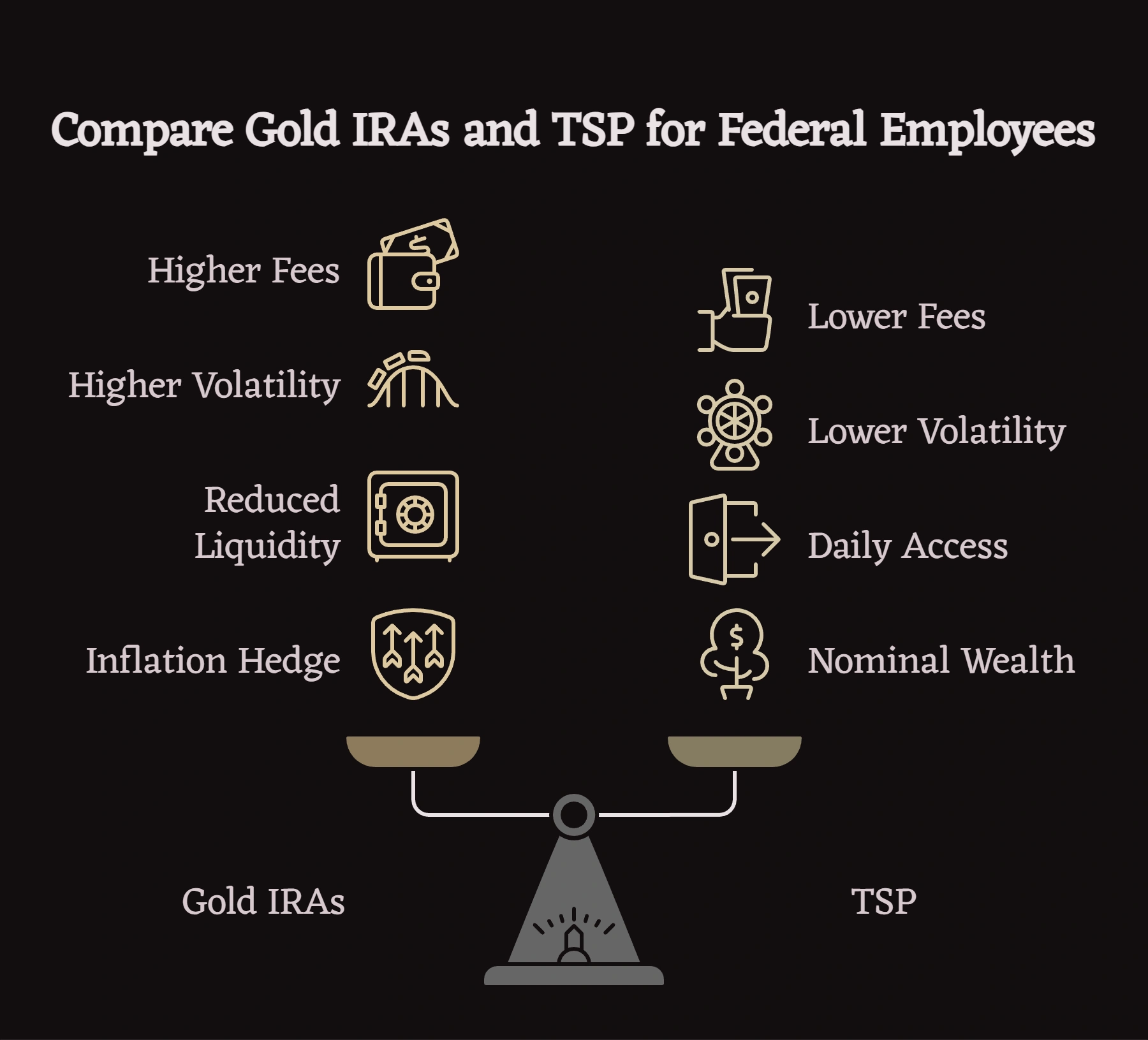

How Do Gold IRAs Actually Complement TSP Holdings?

Gold IRAs and TSP serve fundamentally different functions that can complement each other when properly structured.

TSP provides:

- Ultra-low-cost diversified stock and bond exposure

- Principal guarantee (G Fund) unavailable in private markets

- Daily liquidity through interfund transfers

- Payroll deduction discipline

- Employer matching (1% automatic, 4% additional with contributions)

Gold IRAs provide:

- Physical asset ownership uncorrelated to paper assets

- Inflation hedge during sustained purchasing power erosion

- Diversification beyond TSP's five core funds

- Potential crisis hedge during extreme market dislocations

The question isn't "which is better" but rather "does a modest gold IRA allocation alongside TSP holdings improve long-term inflation-adjusted outcomes enough to justify the fee premium and reduced liquidity?"

2025/2026 Contribution Limits and Gold IRA Minimums

Federal employees maximizing TSP contributions build substantial balances quickly. An employee contributing the maximum $23,500 annually with 5% matching for 10 years accumulates approximately $325,000 (assuming 7% returns)—a balance where gold IRA fees become proportionally more manageable.

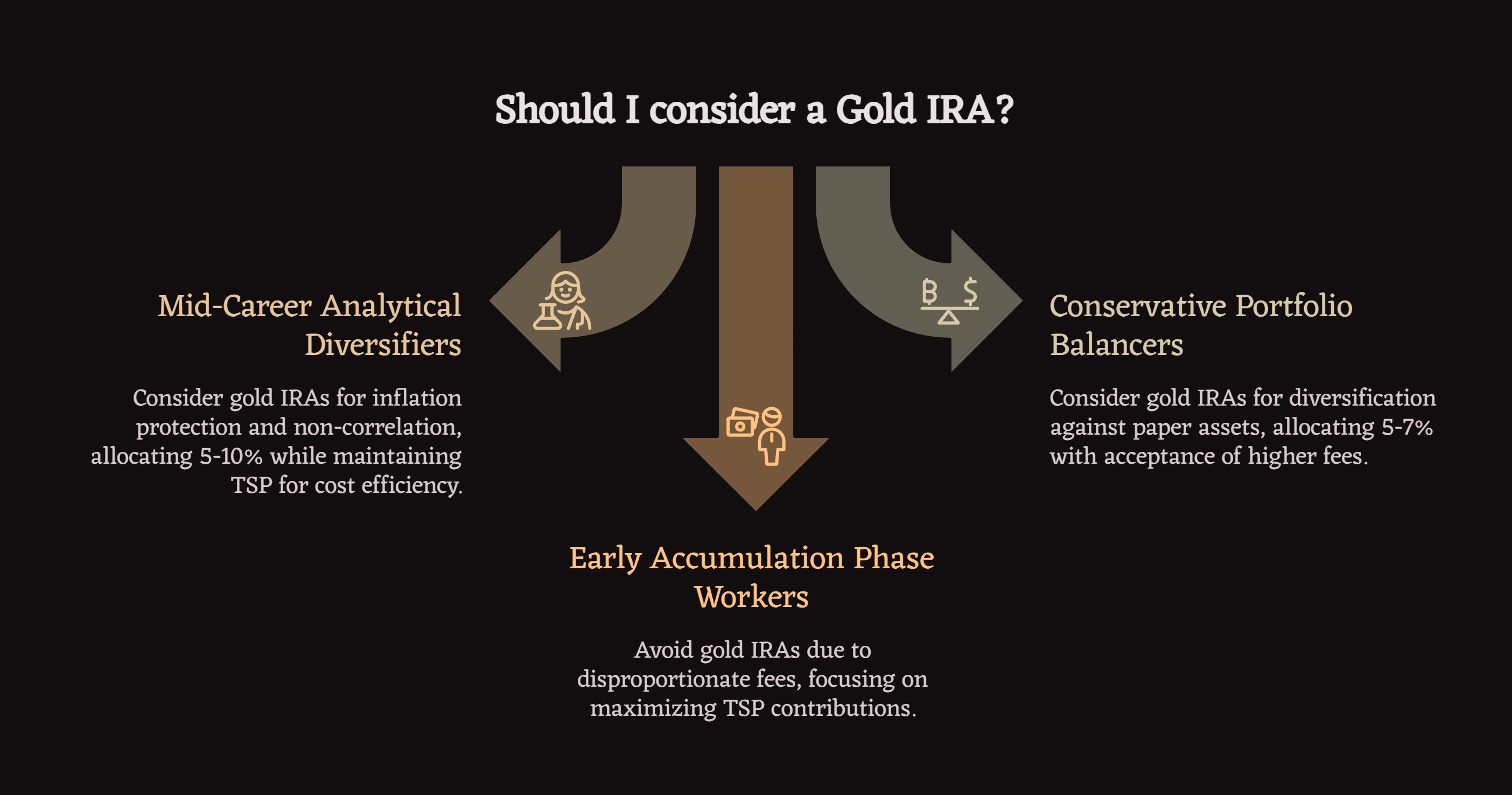

Who Should Actually Consider Gold IRAs?

Mid-Career Analytical Diversifiers

Federal employees in technical roles—engineers, IT specialists, data analysts—with TSP balances of $150,000+ who have studied inflation's compounding impact on purchasing power and understand the fee trade-off. These professionals typically allocate 5-10% to gold IRAs while maintaining 90-95% in TSP for cost efficiency.

Primary concern: Real purchasing power preservation over 20-30 year horizons where even modest inflation rates compound to significant wealth erosion.

Approach: Analytical modeling of multiple scenarios, preference for concrete data over promotional claims, comfort with volatility in exchange for non-correlation.

Conservative Portfolio Balancers

Federal employees approaching mid-to-late career with substantial TSP balances ($200,000+) who have maximized traditional diversification within TSP's five funds and seek exposure to physical assets as a modest portfolio complement.

Primary concern: Over-concentration in paper assets (stocks, bonds, government securities) without tangible alternative asset exposure.

Approach: Small gold IRA allocations (5-7% of total retirement assets) specifically for diversification, not speculation. Acceptance of higher fees as the cost of accessing an asset class unavailable within TSP.

Poor Fit: Early Accumulation Phase Workers

Federal employees with TSP balances below $75,000 face disproportionate fee impacts where gold IRA costs can consume 2-3% annually—enough to meaningfully reduce long-term wealth accumulation during crucial early compounding years.

Better approach: Maximize TSP contributions to reach $100,000+ threshold before considering alternative asset diversification. Use TSP's ultra-low costs during peak accumulation phase.

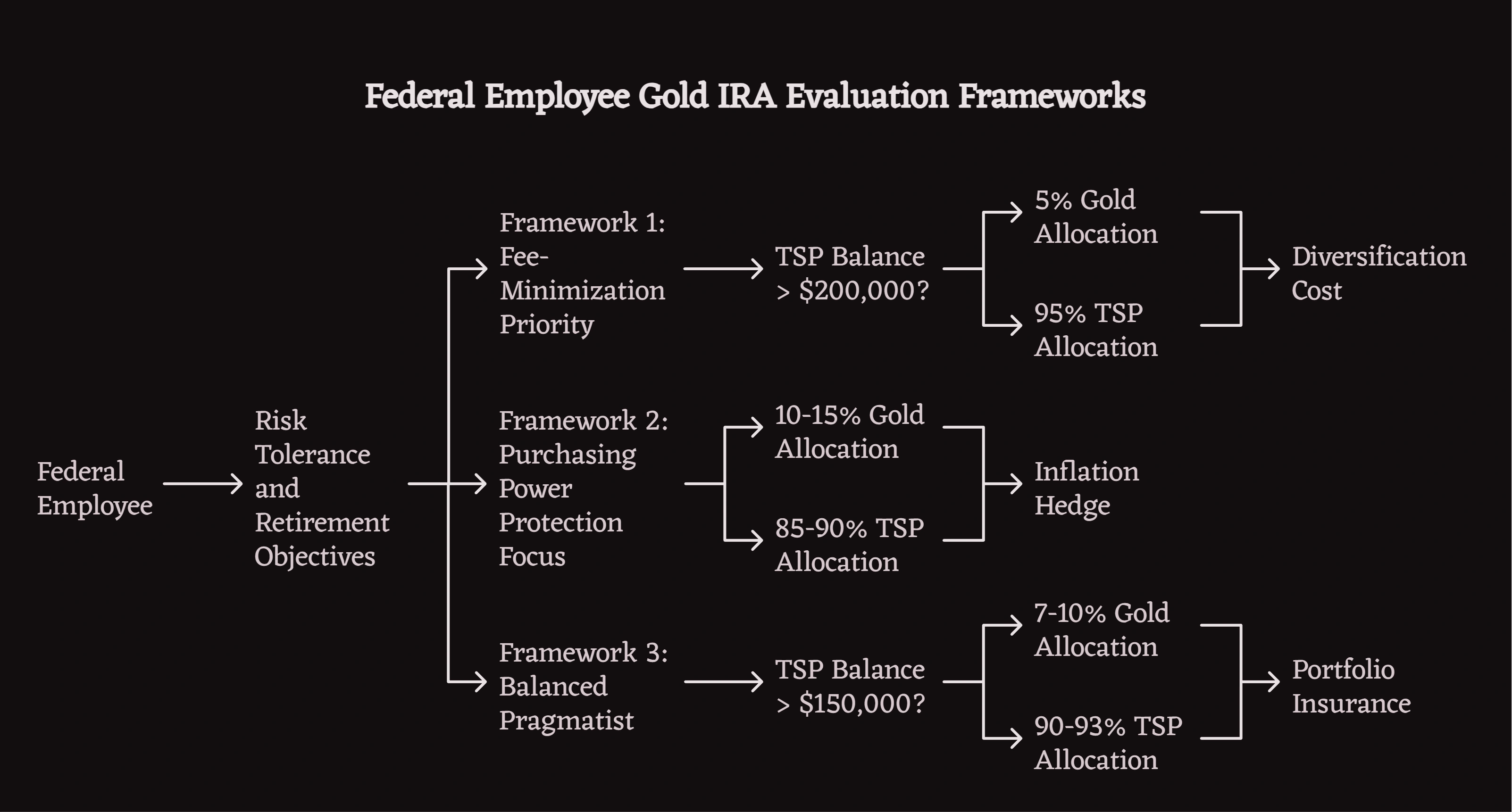

Three Analytical Frameworks for Evaluation

Federal employees approach this question through distinct analytical lenses based on their risk tolerance and retirement objectives.

Framework 1: Fee-Minimization Priority

Profile: Federal employee focused on maximizing compound growth through cost efficiency. Values TSP's 0.042% expense ratio as a meaningful competitive advantage over 20-30 year horizons.

Gold IRA consideration: Only after TSP balance exceeds $200,000 where a 5% gold allocation ($10,000) represents minimal account size but proportional diversification. Accepts higher fees on small gold position as diversification cost.

Typical allocation: 95% TSP (C, S, I, F, G Fund mix), 5% gold IRA

Framework 2: Purchasing Power Protection Focus

Profile: Federal employee concerned about inflation's compounding impact on retirement wealth. Studies historical examples of currency debasement and questions whether nominal preservation equals real preservation.

Gold IRA consideration: Willing to accept higher fees and volatility for inflation hedge characteristics. Targets 10-15% gold allocation as meaningful hedge without overconcentration.

Typical allocation: 85-90% TSP, 10-15% gold IRA

Framework 3: Balanced Pragmatist

Profile: Federal employee who recognizes both TSP's cost advantage and gold's inflation hedge characteristics. Seeks middle ground rather than maximizing either extreme.

Gold IRA consideration: Moderate 7-10% allocation once TSP exceeds $150,000. Views gold IRA as portfolio insurance—hopes it underperforms in stable environments, expects it to preserve value during crises.

Typical allocation: 90-93% TSP, 7-10% gold IRA

The TSP Modernization Act Advantage

The TSP Modernization Act (effective 2019) permits in-service withdrawals for current FERS employees, enabling partial TSP rollovers to self-directed IRAs without separation from federal employment.

Previous limitations: Pre-2019, federal employees could only roll over TSP funds to IRAs after separating from service or reaching age 59½.

Current flexibility: FERS participants can execute partial withdrawals for rollover to IRAs while maintaining federal employment and continuing TSP contributions.

Strategic implications: Federal employees under 50 can fund gold IRAs through partial TSP rollovers without disrupting ongoing accumulation. This permits testing gold IRA positions with modest allocations before committing larger amounts.

Process: Request withdrawal through TSP.gov using Form TSP-77 (Partial In-Service Withdrawal). Specify direct rollover to self-directed IRA custodian to avoid mandatory 20% withholding. Funds transfer within 2-3 weeks.

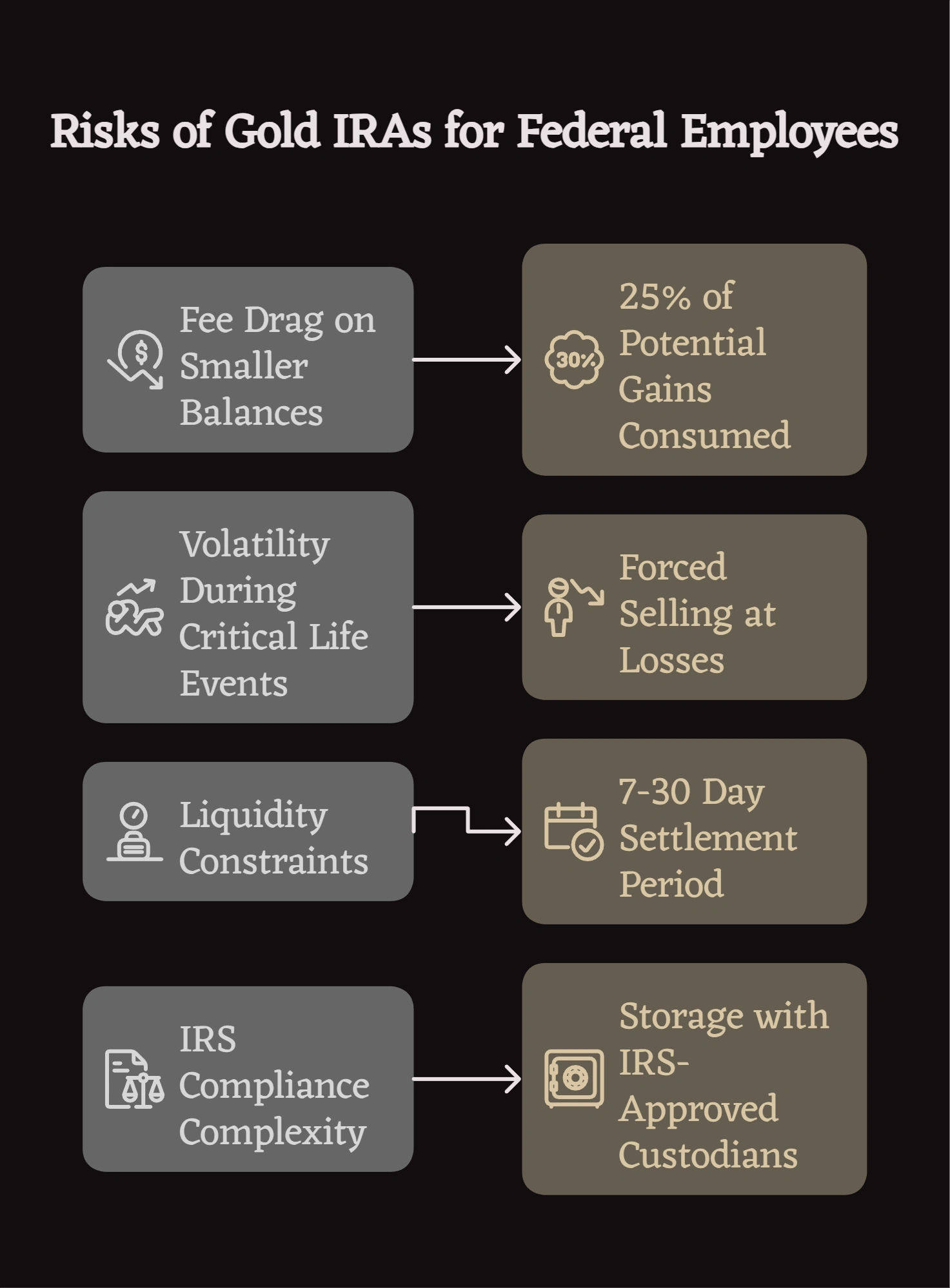

What Are the Real Risks?

Fee Drag on Smaller Balances

A $50,000 gold IRA incurring $780 annual fees (1.56%) plus 5% transaction costs on purchases faces meaningful headwinds. Over 20 years at 5% gross returns, fees consume approximately 25% of potential gains versus TSP's near-zero costs.

Volatility During Critical Life Events

Gold's 15% standard deviation means substantial short-term losses remain possible. Federal employees who need funds during gold bear markets (2011-2015 saw 45% decline) face forced selling at losses or must maintain separate emergency reserves.

Liquidity Constraints

Liquidating physical gold from IRAs requires custodian processing, potential shipping, and settlement periods of 7-30 days. TSP permits daily interfund transfers and withdrawal requests with significantly faster access.

IRS Compliance Complexity

Physical gold in IRAs must meet .995 fineness requirements (American Gold Eagles exempt at .9167). Storage must occur with IRS-approved custodians at qualified depositories—personal possession triggers immediate taxable distribution. These compliance requirements don't exist for TSP management.

Federal employees proceeding with partial TSP rollovers should familiarize themselves with common TSP rollover mistakes that trigger IRS penalties, including indirect rollover timing failures and account type mismatches that create unintended tax consequences.

When Should Federal Employees Actually Make This Move?

Appropriate timing indicators:

- TSP balance exceeds $150,000 where fees become proportionally manageable

- 15+ years until retirement providing recovery time from potential gold volatility

- Complete understanding of fee structures including all-in annual costs

- Allocation will represent 10% or less of total retirement assets

- Comfortable with reduced liquidity versus TSP daily access

- Have studied historical gold performance during various economic environments

Inappropriate timing indicators:

- TSP balance below $75,000 where fees create excessive drag

- Within 10 years of retirement where volatility creates income planning risk

- Considering wholesale TSP conversion rather than modest supplemental allocation

- Attracted primarily by promotional marketing rather than analytical cost-benefit analysis

- Lack of understanding regarding IRS compliance requirements

Federal employees evaluating whether gold IRAs fit within their broader TSP diversification strategy—including the specific pros, cons, and execution considerations of rolling TSP funds to precious metals accounts—may benefit from reviewing a comprehensive analysis of whether rolling a TSP into a gold IRA makes sense for federal workers, including detailed fee comparisons and common mistakes to avoid.

Making the Under-50 Decision

Federal employees under 50 evaluating investing in physical gold to hold in SDIRAs should frame the decision as: "Does a modest inflation hedge allocation justify accepting higher fees, increased volatility, and reduced liquidity for the next 15-30 years?"

For employees with TSP balances exceeding $150,000, risk tolerance for volatility, and genuine concern about purchasing power erosion over multi-decade horizons, gold IRAs may provide valuable diversification despite the fee premium.

For employees prioritizing maximum compound growth through cost minimization, TSP's 0.042% expense ratio represents a meaningful competitive advantage that gold IRAs struggle to overcome mathematically without sustained periods of high inflation.

No universal answer exists. The decision depends on individual circumstances: balance size, time horizon, inflation expectations, risk tolerance, and whether purchasing power protection or nominal wealth maximization represents the primary objective.

Disclaimer: This article provides educational information about TSP diversification and gold IRA considerations for federal employees and does not constitute financial, tax, or legal advice. Federal employees should consult qualified financial advisors, tax professionals, and legal counsel before making retirement allocation decisions. Past performance does not predict future results. TSP.gov and IRS.gov provide authoritative guidance on contribution limits and precious metals IRA requirements.

References

[1] Federal Retirement Thrift Investment Board. "TSP Modernization Act: In-Service Withdrawals." TSP.gov.

[2] Internal Revenue Service. "IRS Notice 2024-80: 2025 Retirement Plan Contribution Limits." IRS.gov.

[3] Internal Revenue Service. "IRC Section 408(m): Precious Metals in IRAs." IRS.gov.

[4] Federal Retirement Thrift Investment Board. "TSP Expense Ratios and Administrative Costs." TSP.gov.

[5] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[6] World Gold Council. "Gold Performance During Inflationary Periods: Historical Analysis." Gold.org.

[7] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020-2024." CFTC.gov.

[8] U.S. Tax Court. "McNulty v. Commissioner: IRA Precious Metals Storage Requirements." Tax Court Case Precedent.

[9] Morningstar. "Fee Impact Analysis: Retirement Account Cost Structures." Morningstar.com.

[10] Federal Retirement Thrift Investment Board. "Form TSP-77: Partial In-Service Withdrawal." TSP.gov.