.svg)

Federal employees can roll over Thrift Savings Plan funds into a self-directed silver IRA without triggering taxes or penalties — provided the transfer uses a direct, trustee-to-trustee method. The TSP does not hold physical precious metals directly; a self-directed IRA with an IRS-approved custodian is required. Silver must meet 99.9% IRS purity standards, and storage must occur at an IRS-approved depository. The primary risks in this process are not the metal itself, but rollover execution errors, dealer markup spreads, and the Rule of 55 exception that many federal employees forfeit by rolling funds out prematurely.

Last updated: May 2026

At a Glance

- Direct rollovers avoid the 20% mandatory federal withholding that applies to indirect TSP distributions

- Federal employees who separate at age 55 or older can access TSP funds penalty-free — a benefit that does not transfer to a rolled-over IRA

- Silver's lower per-ounce cost makes meaningful diversification accessible at smaller rollover amounts than gold typically requires

- Noble Gold Investments, Birch Gold Group, and Augusta Precious Metals each handle TSP rollovers under different minimums and fee structures

Who This Guide Is Designed For

This article is written for federal employees under FERS or CSRS who are evaluating a partial or full TSP rollover into a self-directed silver IRA — particularly those who are separated from service, approaching retirement, or considering diversification beyond the TSP's five core funds. It is not a guide for active-duty employees seeking in-service withdrawals without separation (though the TSP Modernization Act provisions are noted where relevant).

What Critics of TSP Rollovers to Precious Metals Often Say — and Why Federal Employees Still Evaluate Them

Financial advisors who champion the TSP's cost structure point to its extraordinary expense ratios — averaging 0.042% in 2024, among the lowest of any retirement plan available to American workers. For a $100,000 balance, that equals $42 annually. A silver IRA holding the same balance typically incurs $200–$500 in combined custodian and storage fees, representing a meaningful cost premium.

These objections deserve fair consideration. The case for adding physical silver to a retirement portfolio does not rest on returns competing with equities. It rests on structural non-correlation — silver has historically moved differently from both stocks and government bonds, which may reduce overall portfolio drawdown during periods of simultaneous market stress. For federal employees heavily concentrated in the TSP's C Fund and G Fund, a modest allocation to physical silver introduces an asset class not otherwise available within the TSP framework.

The decision is not binary. Many federal employees evaluate a partial rollover — moving 5–10% of TSP assets while preserving the majority of savings in the TSP's low-cost structure.

Why the Rule of 55 Changes the Math for Employees Near Retirement

This section addresses one of the most commonly misunderstood aspects of TSP-to-IRA rollovers — and one that can cost federal employees thousands of dollars if overlooked.

IRS regulations impose a 10% early withdrawal penalty on retirement distributions before age 59½. The TSP provides a significant exception: federal employees who separate from service during or after the calendar year they reach age 55 — and age 50 for public safety employees, including federal law enforcement and firefighters — may take penalty-free withdrawals directly from the TSP.

This exception applies only to funds that remain in the TSP. It does not transfer to a rolled-over IRA.

A federal employee who separates at age 57 and rolls their entire TSP into a silver IRA loses penalty-free access to those funds until age 59½. Any distributions taken before that age from the IRA face the standard 10% penalty plus ordinary income tax.

For federal employees separating between ages 55 and 59½, the strategic decision often involves keeping a portion of TSP funds in the plan to preserve the penalty-free access window, while rolling a separate portion into a silver IRA for long-term diversification purposes. Rolling TSP funds directly to a self-directed IRA custodian — rather than taking possession of the funds — preserves the tax-deferred status while avoiding the 60-day indirect rollover complications.

Federal employees in this age window benefit from reviewing this trade-off with a tax professional before initiating any rollover.

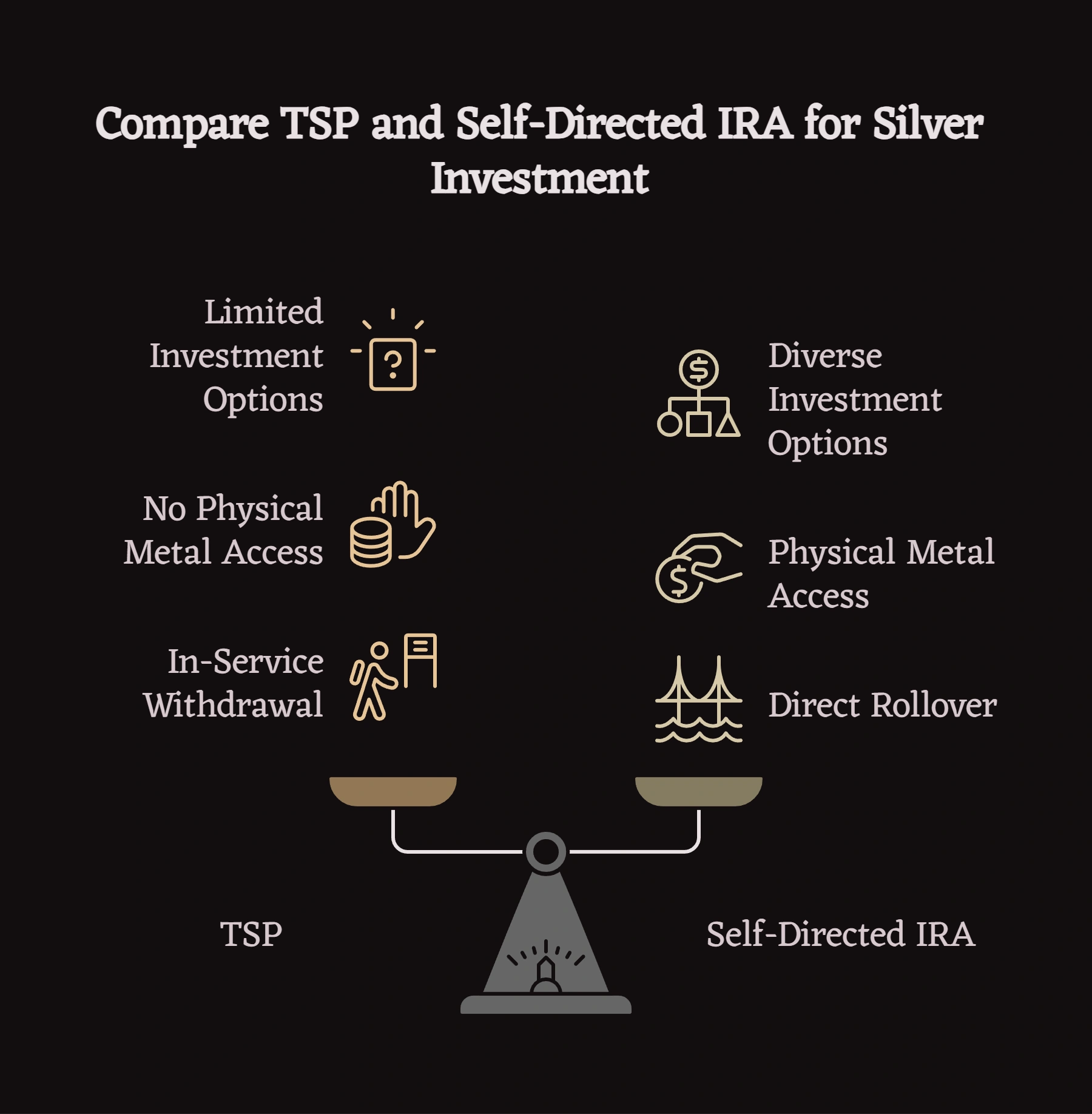

Does the TSP Allow Federal Employees to Hold Physical Silver?

The Thrift Savings Plan does not offer physical precious metals as an investment option. The plan's five core funds — G, F, C, S, and I — consist of government securities, bond indices, and broad equity market indices. TSP participants cannot purchase physical silver, gold, or any other commodity directly within the plan.

Physical silver becomes accessible within a retirement account structure only through a self-directed IRA. This account type holds legal title to assets — including IRS-approved bullion — through an IRS-approved custodian, while the physical metals remain in segregated storage at an IRS-approved depository.

The TSP Modernization Act (Public Law 115-84, effective 2019) expanded in-service withdrawal options for active FERS participants, allowing partial rollovers to IRAs without requiring separation from federal employment. FERS participants may use Form TSP-77 to request a partial in-service withdrawal for direct rollover to a self-directed IRA custodian. This change permits active federal employees to establish a silver IRA position while continuing TSP contributions — though each participant's eligibility depends on their specific age and employment status.

How Does a Direct TSP Rollover to a Silver IRA Work?

A direct rollover — also called a trustee-to-trustee transfer — moves TSP funds straight to the receiving IRA custodian without the account holder taking possession at any point. This method avoids the 20% mandatory federal withholding that applies to indirect distributions and eliminates the 60-day redeposit deadline entirely.

The process typically follows this sequence:

Step 1 — Open the self-directed IRA account. The receiving custodian (such as Equity Trust or Kingdom Trust, which Noble Gold works with) opens a self-directed IRA before the transfer initiates. Account opening generally takes 3–5 business days.

Step 2 — Request rollover authorization from TSP. Federal employees initiate the outbound transfer through TSP.gov or by submitting Form TSP-70 (full withdrawal) or Form TSP-77 (partial withdrawal, for eligible in-service requests). The form requires the receiving custodian's name, address, and account details.

Step 3 — TSP processes the transfer. TSP transmits funds directly to the receiving custodian. Processing typically takes 2–4 weeks from approval. The TSP charges no fee for outbound direct rollovers.

Step 4 — Custodian receives funds and purchases silver. Once the custodian receives the funds, the account holder selects IRS-approved silver products. The custodian coordinates the purchase and directs the metals to an IRS-approved depository for segregated storage.

Step 5 — Confirm custodian-issued IRS Form 5498. The receiving custodian issues Form 5498 annually to report the rollover contribution and fair market value. This document protects against future IRS questions about the transfer's tax-deferred status.

Why Do Indirect Rollovers Create Risk for Federal Employees?

An indirect rollover distributes TSP funds directly to the account holder, who then has 60 days to deposit them into a qualifying IRA. The TSP withholds 20% for federal taxes on indirect distributions — meaning a $100,000 rollover produces an $80,000 check. To complete a tax-free rollover of the full $100,000, the account holder must deposit the entire amount from personal funds within 60 days, then reclaim the withheld $20,000 through their tax return.

Federal employees who miss the 60-day deadline convert the entire distribution into taxable income for that year. For those under age 59½, the 10% early withdrawal penalty also applies. Federal retirement specialists report that over 15% of indirect rollovers fail to meet the deadline, triggering unintended tax consequences averaging $8,000–$15,000 per incident.

Indirect rollovers are also limited to once per 12-month period across all IRAs. Direct rollovers carry no such restriction.

What IRS Rules Govern TSP Rollovers to Silver IRAs?

The IRS permits tax-deferred rollovers from traditional TSP accounts to traditional IRAs and from Roth TSP accounts to Roth IRAs. Mixing account types — rolling a traditional TSP into a Roth IRA — triggers a taxable conversion event in the year of transfer.

Key IRS rules for TSP-to-silver-IRA rollovers:

- Purity standards: Silver held in a self-directed IRA must meet 99.9% fineness. American Silver Eagles are exempt from this specific standard due to their government mint status and qualify regardless. Canadian Silver Maple Leafs and Austrian Silver Philharmonics both meet the 99.9% threshold.

- Storage requirements: Physical silver cannot be stored at home or in a personal safe deposit box without triggering an immediate taxable distribution. IRS Publication 590 requires storage at an IRS-approved depository. Home storage promotions that claim IRA compliance have been consistently rejected in U.S. Tax Court — most recently affirmed in McNulty v. Commissioner.

- Prohibited transactions: The account holder cannot take personal possession of the silver at any point while it remains inside the IRA structure. Doing so constitutes a taxable distribution of the entire account value.

- RMD requirements: Self-directed silver IRAs are subject to Required Minimum Distributions beginning at age 73 (for those reaching age 72 after December 31, 2022, under SECURE 2.0). RMDs from a silver IRA must be calculated separately from any remaining TSP balance — the two cannot be aggregated.

- Roth TSP five-year rule: Roth TSP funds rolled into a Roth IRA must satisfy a five-year holding period before qualified tax-free distributions can be taken. If the Roth IRA is newly opened at the time of rollover, the five-year clock begins at the time of the rollover contribution, not the original TSP contribution date.

How Does a Silver IRA Differ from a Gold IRA for Federal Employees?

A silver IRA and a gold IRA operate under identical IRS frameworks — both are self-directed IRAs holding IRS-approved physical bullion through an approved custodian and depository. The distinction lies in the metal held, its price point, and the demand characteristics that influence long-term price behavior.

Silver's lower unit price allows federal employees to build a meaningful physical position at smaller rollover amounts. A $25,000 TSP allocation buys approximately 700–800 troy ounces of silver, compared to fewer than 9 ounces of gold at current prices. This difference matters for employees with moderate TSP balances who want tangible metal exposure without concentrating the allocation in a single high-priced asset.

What Is the Industrial Demand Argument for Silver?

Silver's industrial consumption accounts for over 50% of annual global demand — a structural characteristic gold does not share. The Silver Institute's 2024 data shows industrial demand at 654 million ounces, driven primarily by electrical conductivity applications in electric vehicle components, photovoltaic solar panels, 5G infrastructure, and semiconductor manufacturing.

Each electric vehicle requires approximately 25–50 grams of silver for electrical connections, battery management systems, and charging components. Solar panel installations account for roughly 12% of total annual silver demand. Both sectors are projected to grow through the 2030s under current energy transition trajectories.

This industrial demand floor creates a price behavior pattern distinct from gold. When monetary demand for silver weakens, industrial consumption partially absorbs supply. This dual-demand structure is why some investors evaluate silver as a non-correlated complement to both equities and gold within a diversified retirement portfolio.

Where the industrial demand argument has limits: Silver's industrial exposure also means its price responds to global manufacturing slowdowns and economic contractions. During the 2020 COVID-19 shock, silver fell sharply alongside industrial commodities before recovering strongly. Federal employees considering silver as a purely defensive asset should note this characteristic — silver is not a pure safe haven in the manner of U.S. Treasuries or the TSP G Fund.

What Are the Fees for a TSP to Silver IRA Rollover?

Direct TSP-to-silver-IRA rollovers incur no IRS penalties when executed correctly. The TSP charges no outbound fee for direct rollovers. The costs that do apply are on the receiving IRA side.

The bid-ask spread — the gap between the dealer's purchase price and the spot price — is often the largest single cost in the first year and is frequently underemphasized in promotional materials. On a $100,000 silver purchase at a 5% spread, the account begins $5,000 below spot value before any price movement occurs. Federal employees who request written fee schedules before committing, including explicit spread disclosures, are in a stronger position to compare providers accurately.

For context: TSP expense ratios averaged 0.042% in 2024, meaning a $100,000 TSP balance costs $42 annually. A $100,000 silver IRA position at the same balance incurs approximately $500–$900 in the first year — roughly 12–21 times the TSP's annual cost. This fee premium is the primary mathematical headwind silver IRAs face relative to TSP allocations, and federal employees should weigh it explicitly when determining what allocation percentage makes sense for their situation.

Which Precious Metals Companies Handle TSP Rollovers?

Several companies maintain relationships with IRS-approved custodians and process TSP-to-silver-IRA rollovers. The three most commonly evaluated by federal employees are Noble Gold Investments, Birch Gold Group, and Augusta Precious Metals.

Noble Gold Investments

Noble Gold Investments works with Equity Trust and Kingdom Trust as IRA custodians and offers storage through the Texas Precious Metals Depository and the Delaware Depository. The company has developed TSP-specific rollover procedures for federal and military clients and positions silver as a primary offering alongside gold.

Noble Gold maintains allocated (segregated) storage for each client — meaning silver holdings are assigned specific serial numbers rather than pooled with other clients' metals. This approach provides clear ownership records and simplifies valuation for annual Form 5498 reporting.

Federal employees working with Noble Gold should obtain TSP withdrawal authorization documentation before initiating any metals purchase agreement. Custodian account setup and TSP transfer processing typically takes 3–5 weeks from initiation to completion.

Who Noble Gold tends to suit: Federal employees seeking TSP rollover support with a provider experienced in government retirement plan transfers, lower initial balance requirements, and Texas or Delaware depository options.

Birch Gold Group

Birch Gold Group works primarily through Equity Trust as its IRA custodian and offers storage at the Delaware Depository or Brink's Global Services. The company's minimum investment for a precious metals IRA is $10,000, making it accessible for employees with smaller TSP rollover amounts or those making partial allocations.

Who Birch Gold tends to suit: Federal employees with smaller TSP balances, those making a partial first allocation to test silver IRA positioning, or cost-sensitive investors evaluating entry-level options.

Augusta Precious Metals

Augusta Precious Metals requires a $50,000 minimum investment, positions itself as an education-first provider, and works with Equity Trust as its primary custodian. Augusta limits its metals offerings to gold and silver only — no platinum or palladium — which the company frames as a deliberate decision to reduce product complexity for long-term retirement investors.

Augusta's onboarding process includes a one-on-one education session with a Harvard-trained analyst, which distinguishes its service model from higher-volume providers. This structure suits investors who want guided onboarding and are comfortable with a longer decision-making process.

Who Augusta tends to suit: Federal employees with six-figure TSP rollover amounts who prioritize education depth, white-glove onboarding, and long-term silver or gold positioning.

Who should look elsewhere: Employees with balances below $50,000, those seeking platinum or palladium, or those wanting faster account setup.

Fee structures and minimums are subject to change. Federal employees should request current written fee schedules directly from each provider before making a decision.

Does Silver in an IRA Protect Against Inflation?

Silver held in a self-directed IRA has historically shown low correlation with broad equity markets and may serve as a portfolio diversifier during periods of sustained inflation or currency purchasing power erosion. Between 2000 and 2011, silver prices increased approximately 900%, substantially outpacing CPI inflation during that period. Between 2011 and 2015, silver declined approximately 70% from its peak — a drawdown that underscores its volatility relative to more stable inflation hedges like TIPS.

The inflation protection case for silver rests on two mechanisms. First, as a tangible asset with no counterparty risk, silver has historically held real value across inflationary cycles even when dollar-denominated savings eroded. Second, industrial demand creates a structural price floor that pure monetary assets like gold do not share.

Federal employees allocating silver for inflation protection purposes typically maintain 5–10% of total retirement assets in precious metals — a range that provides meaningful exposure without concentrating risk in a single volatile asset class. Allocations above 15% are generally considered outside the range of conventional diversification strategy for retirement-focused investors.

How Does Self-Directed IRA Custody Work for Physical Silver?

Self-directed IRA custody separates two distinct functions: the custodian holds legal title to the IRA account and maintains all IRS-required records, while the depository holds the physical metals in secure, insured storage.

The custodian — an IRS-approved trust company such as Equity Trust — issues annual Form 5498 reporting the account's fair market value and any rollover contributions. The depository — such as the Delaware Depository or Texas Precious Metals Depository — stores allocated silver bars and coins in individually assigned vault space, insures the holdings against theft and loss, and undergoes regular third-party audits.

Federal employees cannot hold IRA-owned silver personally at any point while it remains inside the IRA structure. Removing metals from the depository without first taking a formal IRA distribution triggers an immediate taxable event on the fair market value of the distributed metals, plus the 10% early withdrawal penalty for those under age 59½.

When federal employees reach age 73 and begin taking Required Minimum Distributions from a silver IRA, distributions can be taken in two ways: the custodian can liquidate a portion of the silver holding and distribute cash, or in some cases physical metals can be distributed in-kind — though the latter requires the account holder to assume storage and insurance responsibilities for the distributed portion.

What Are the Long-Term Retirement Planning Considerations?

Rolling a portion of TSP funds into a silver IRA introduces a non-correlated asset class that may reduce sequence-of-returns risk — the compounding impact of market losses in the years immediately before and after retirement. Federal employees with heavily equity-weighted TSP allocations approaching retirement may find that a modest silver allocation provides a second drawdown buffer alongside the TSP's G Fund.

Five practices support effective long-term management of a silver IRA alongside TSP holdings:

1. Set a target allocation percentage, not a dollar amount. Silver's price volatility means a fixed dollar allocation will drift significantly over time. A percentage target — typically 5–10% of total retirement assets — provides a rebalancing anchor.

2. Review custodian fees annually against account value. As a silver IRA grows, fixed annual fees (typically $200–$500) represent a declining percentage of account value. An account that begins at $25,000 faces a 1%+ annual fee drag. At $150,000, the same fixed costs represent 0.3% — more comparable to other alternative asset structures.

3. Rebalance when silver allocation drifts more than 5 percentage points from target. Silver's price movements can push its portfolio weight significantly above or below the target without active management.

4. Coordinate Required Minimum Distributions with silver liquidation strategy beginning at age 72. RMDs from a silver IRA are calculated separately from TSP RMDs and cannot be aggregated. Planning the liquidation sequence — silver vs. TSP vs. other IRAs — involves tax timing decisions worth reviewing with a qualified tax professional annually.

5. Retain all rollover documentation for seven years. IRS Form 1099-R (issued by TSP for the outbound distribution), Form 5498 (issued by the receiving custodian annually), and all transfer authorization forms constitute the paper trail that protects against IRS audit challenges on the rollover's tax-deferred status.

Who Should Consider a TSP to Silver IRA Rollover — and Who Should Not

This approach may merit evaluation for:

- Federal employees separated from service who have maximized diversification within the TSP's five funds and want exposure to a physical asset class not available within the plan

- FERS participants over age 59½ where the Rule of 55 penalty exception is no longer relevant to the rollover decision

- Employees with TSP balances above $100,000 where silver IRA fee structures represent a manageable percentage of account value (below 0.5% annually)

- Federal employees within 10–20 years of retirement who want to introduce a non-correlated asset before sequence-of-returns risk becomes acute

This approach warrants additional caution for:

- Federal employees who have separated between ages 55 and 59½ and would forfeit penalty-free TSP withdrawal access by rolling funds into an IRA

- Active employees with TSP balances below $50,000 where fixed silver IRA fees create disproportionate annual cost drag

- Employees within 3–5 years of retirement who may need near-term liquidity — silver IRA liquidation takes 3–7 business days versus TSP's same-day interfund transfer capability

- Employees who have not yet consulted a tax professional on the Roth vs. traditional rollover distinction for their specific tax situation

Frequently Asked Questions

Can a federal employee roll over a TSP into a silver IRA while still employed?

FERS participants may execute a partial in-service withdrawal to a self-directed IRA using Form TSP-77, provided they meet age and eligibility requirements under the TSP Modernization Act. Not all employees qualify — eligibility depends on age and the number of in-service withdrawals previously taken. Employees should confirm current eligibility through TSP.gov before initiating the process.

What is the difference between direct and indirect TSP rollovers?

A direct rollover transfers funds trustee-to-trustee from TSP to the receiving IRA custodian, avoiding mandatory 20% federal withholding and the 60-day deadline. An indirect rollover distributes funds to the account holder first, with TSP withholding 20% for taxes. The account holder must deposit the full original amount — including the withheld 20% from personal funds — into a qualifying IRA within 60 days to complete a tax-free transfer.

What silver products qualify for an IRA?

IRS-eligible silver products include American Silver Eagles (any year), Canadian Silver Maple Leafs (.9999 fine), Austrian Silver Philharmonics (.999 fine), and silver bars and rounds of .999 fineness or higher from approved refiners such as PAMP Suisse, Valcambi, and the Royal Canadian Mint. 100-oz bars from approved refiners are commonly used in larger IRA positions due to their lower per-ounce spread relative to coins.

Does the Rule of 55 apply to silver IRAs?

No. The Rule of 55 applies only to employer-sponsored plans — including the TSP — and allows penalty-free withdrawals for employees who separate from service at age 55 or older (age 50 for qualifying public safety employees). Once TSP funds are rolled into an IRA of any type, the Rule of 55 exception no longer applies to those funds. Distributions before age 59½ from the IRA are subject to the standard 10% early withdrawal penalty.

How are Required Minimum Distributions handled for a silver IRA?

RMDs from a self-directed silver IRA begin at age 73 and are calculated based on the account's fair market value as of December 31 of the prior year, divided by the IRS life expectancy factor for the account holder's age. Distributions may be taken as cash (requiring silver liquidation) or, in some cases, as an in-kind distribution of physical metals. TSP RMDs and silver IRA RMDs are calculated and satisfied separately — they cannot be aggregated with each other, though multiple IRA RMDs can be aggregated and satisfied from a single IRA.

What happens to the silver IRA if the provider goes out of business?

The IRA account and its metal holdings belong to the account holder, not the dealer or custodian. The physical silver is held at a third-party depository independent of the dealer. If a dealer ceases operations, the custodian relationship and depository storage continue uninterrupted. If a custodian fails, FDIC and SIPC protections do not apply to IRA-held physical metals — however, the metals themselves remain the property of the IRA owner and are segregated from the custodian's own assets.

This article provides educational information about TSP rollover mechanics and self-directed IRA structures. It does not constitute financial, tax, or investment advice. Federal employees considering a TSP rollover are encouraged to consult a qualified tax professional or fiduciary financial advisor familiar with government retirement plans before making any transfer decisions. TSP.gov and IRS.gov provide authoritative guidance on contribution rules, rollover requirements, and precious metals IRA regulations.

References

[1] Federal Retirement Thrift Investment Board. "TSP Modernization Act: In-Service Withdrawals." TSP.gov.

[2] Internal Revenue Service. "Topic No. 413: Rollovers from Retirement Plans." IRS.gov.

[3] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[4] Internal Revenue Service. "IRC Section 408(m): Treatment of Collectibles in IRAs." IRS.gov.

[5] Federal Retirement Thrift Investment Board. "TSP Expense Ratios and Administrative Costs." TSP.gov. 2024.

[6] Silver Institute. "World Silver Survey 2024." SilverInstitute.org.

[7] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020–2024." CFTC.gov.

[8] U.S. Tax Court. "McNulty v. Commissioner." Tax Court Case Precedent. IRS home storage IRA ruling.

[9] Internal Revenue Service. "Retirement Topics — Required Minimum Distributions (RMDs)." IRS.gov.

[10] Federal Retirement Thrift Investment Board. "Form TSP-70: Request for Full Withdrawal." TSP.gov.

[11] Federal Retirement Thrift Investment Board. "Form TSP-77: Partial In-Service Withdrawal." TSP.gov.

[12] Internal Revenue Service. "IRS Notice 2024-80: 2025 Retirement Plan Contribution Limits." IRS.gov.