.svg)

Federal employees rolling over Thrift Savings Plan funds into precious metals IRAs increasingly evaluate silver alongside — or instead of — gold. Three structural factors drive this shift: silver's lower per-ounce cost makes meaningful diversification accessible at smaller rollover amounts, its industrial demand from electric vehicles and solar manufacturing creates a non-monetary price floor gold does not share, and the current gold-to-silver ratio near historically elevated levels leads some investors to view silver as relatively undervalued on a long-term basis. This article examines each factor and the specific circumstances under which silver represents a more practical choice than gold for federal retirement diversification.

Last updated: May 2026

At a Glance

- Silver's ~$30–$35 per-ounce price (2026) allows federal employees with moderate TSP balances to build a tangible physical position at allocations that gold's $3,000+ price point makes impractical

- Industrial silver demand reached 654 million ounces in 2024 according to the Silver Institute — more than half of total annual demand — compared to gold's approximately 10% industrial usage

- The gold-to-silver ratio near 88:1 in early 2026 sits above its 50-year historical average of approximately 60:1, which some investors interpret as silver being relatively undervalued

- Silver is not a lower-risk choice than gold — its annual price volatility runs approximately 25–30% versus gold's 15%, and federal employees near retirement should factor this distinction into allocation sizing

Who This Article Is For

This article is written for federal employees who have already decided to add precious metals exposure to their retirement portfolio through a TSP rollover and are now evaluating whether silver or gold makes more sense for their specific situation. It is not an argument that silver is universally superior to gold, or that either metal is necessary for retirement diversification. It presents the specific factors that make silver a more practical fit for certain federal employees — and identifies where gold remains the stronger choice.

What Makes Silver Different From Gold as an IRA Asset?

Gold and silver share the same IRS regulatory framework for self-directed IRAs — identical custodian requirements, identical depository storage rules, identical purity standards framework, and identical prohibited transaction rules. From a compliance standpoint, choosing silver over gold does not simplify or complicate the IRA structure in any meaningful way.

The differences that matter for federal employees making this decision are economic, not regulatory.

Silver is consumed. Gold is stored. Gold's industrial consumption accounts for approximately 10% of annual demand — the other 90% is held as monetary reserves, investment holdings, or jewelry. Silver's industrial consumption accounts for over 50% of annual demand. Once silver is used in a solar panel, an electric vehicle battery management system, or a semiconductor wafer, it is effectively removed from available supply. Gold, by contrast, is almost entirely recyclable and returns to market supply through scrap recovery.

This difference has a practical implication for long-term supply and demand dynamics. Silver's above-ground stockpiles are being drawn down by industrial consumption in a way gold's are not.

Silver responds to different catalysts. Gold price movements are heavily influenced by central bank reserve decisions, U.S. dollar strength, and investor sentiment around monetary policy. Silver responds to those same monetary factors but adds an industrial overlay that causes it to move with global manufacturing activity, technology adoption curves, and energy infrastructure investment.

For federal employees whose retirement portfolios are already heavily exposed to equity market performance through TSP C Fund and S Fund holdings, silver's partial industrial/partial monetary demand profile may add a different correlation characteristic than gold's more purely monetary behavior.

Why Does Silver's Lower Price Point Matter for Federal Employees?

The practical significance of silver's lower per-ounce price is most apparent at the account sizes common among federal employees executing partial TSP rollovers.

A federal employee who decides to allocate $20,000 from a TSP rollover to precious metals faces a fundamentally different experience with silver versus gold at current prices:

- $20,000 in silver at $32 per ounce: approximately 625 troy ounces — a tangible, meaningful physical position

- $20,000 in gold at $3,100 per ounce: approximately 6.5 troy ounces — fewer than 7 coins or small bars

The psychological and practical significance of this difference is not trivial. Federal employees who view precious metals as a tangible hedge — physical metal they can account for and understand — often report that a position of fewer than 10 gold coins feels insubstantial relative to their retirement balance. The same dollar amount in silver produces a position that feels proportionate.

More practically, silver's lower unit price allows for more flexible allocation sizing. A federal employee contributing to a silver IRA through annual IRA contributions ($7,000 for those under 50, $8,000 for those 50 and older in 2025) can build a meaningful silver position over time through consistent purchases. Building a comparable gold position through annual contributions is slower given gold's per-ounce cost.

This lower entry cost does not make silver safer or less volatile than gold. It makes meaningful diversification accessible at allocation sizes that federal employees with moderate TSP balances can practically achieve.

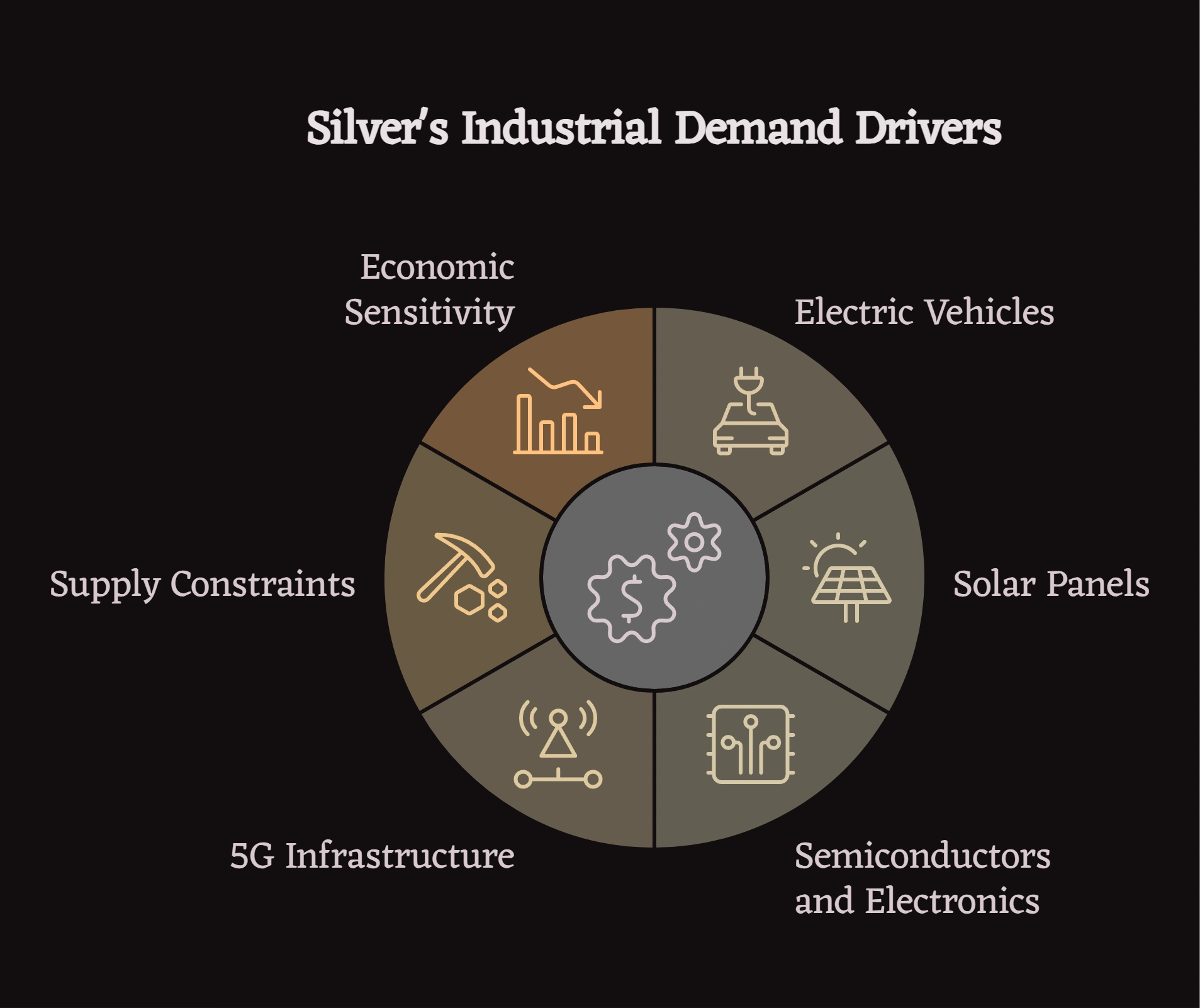

What Is the Industrial Demand Argument for Silver?

Silver's industrial consumption creates a structural demand floor that gold lacks. Understanding the specific sectors driving this demand helps federal employees evaluate whether silver's industrial thesis is durable rather than speculative.

Electric vehicles: Each EV requires approximately 25–50 grams of silver for electrical connections, battery management systems, thermal regulation, and charging infrastructure. Global EV sales reached approximately 17 million units in 2024. At the midpoint of 37 grams per vehicle, that represents roughly 630 million grams — or approximately 20 million troy ounces — consumed by EV manufacturing alone annually. As EV adoption continues through 2030 and beyond, this demand source is projected to grow.

Solar panels: Photovoltaic solar cells use silver as a conductor on cell contacts. The Silver Institute estimated solar panel manufacturing consumed approximately 232 million ounces of silver in 2024 — roughly 28% of total industrial demand. The global solar installation pipeline represents a multi-decade demand source that does not depend on consumer sentiment or monetary policy.

Semiconductors and electronics: Silver's electrical conductivity — the highest of any element — makes it irreplaceable in printed circuit board contacts, semiconductor packaging, and high-frequency electronics. As AI infrastructure buildout accelerates demand for data center components, silver's role in semiconductor manufacturing represents a technology-driven demand source independent of precious metals investor sentiment.

5G infrastructure: Silver-bearing components are used extensively in 5G base stations and antenna arrays. Global 5G infrastructure deployment is ongoing through the late 2020s across major markets.

The supply constraint context: The Silver Institute's 2024 World Silver Survey reported total silver demand at approximately 1.2 billion ounces against mine production of approximately 823 million ounces. The deficit is partially offset by above-ground stock drawdowns and recycling, but structural production constraints — declining ore grades, limited new major mine development — mean supply cannot quickly respond to demand increases. This supply-demand dynamic is a fundamentals-based argument that does not require monetary policy or investor sentiment to sustain.

Where the industrial demand argument has limits: Silver's industrial exposure also means its price declines during global manufacturing recessions and economic contractions. During the 2015–2016 manufacturing slowdown, silver fell approximately 30% before recovering. Federal employees should treat the industrial demand thesis as a long-term structural argument, not a near-term price prediction.

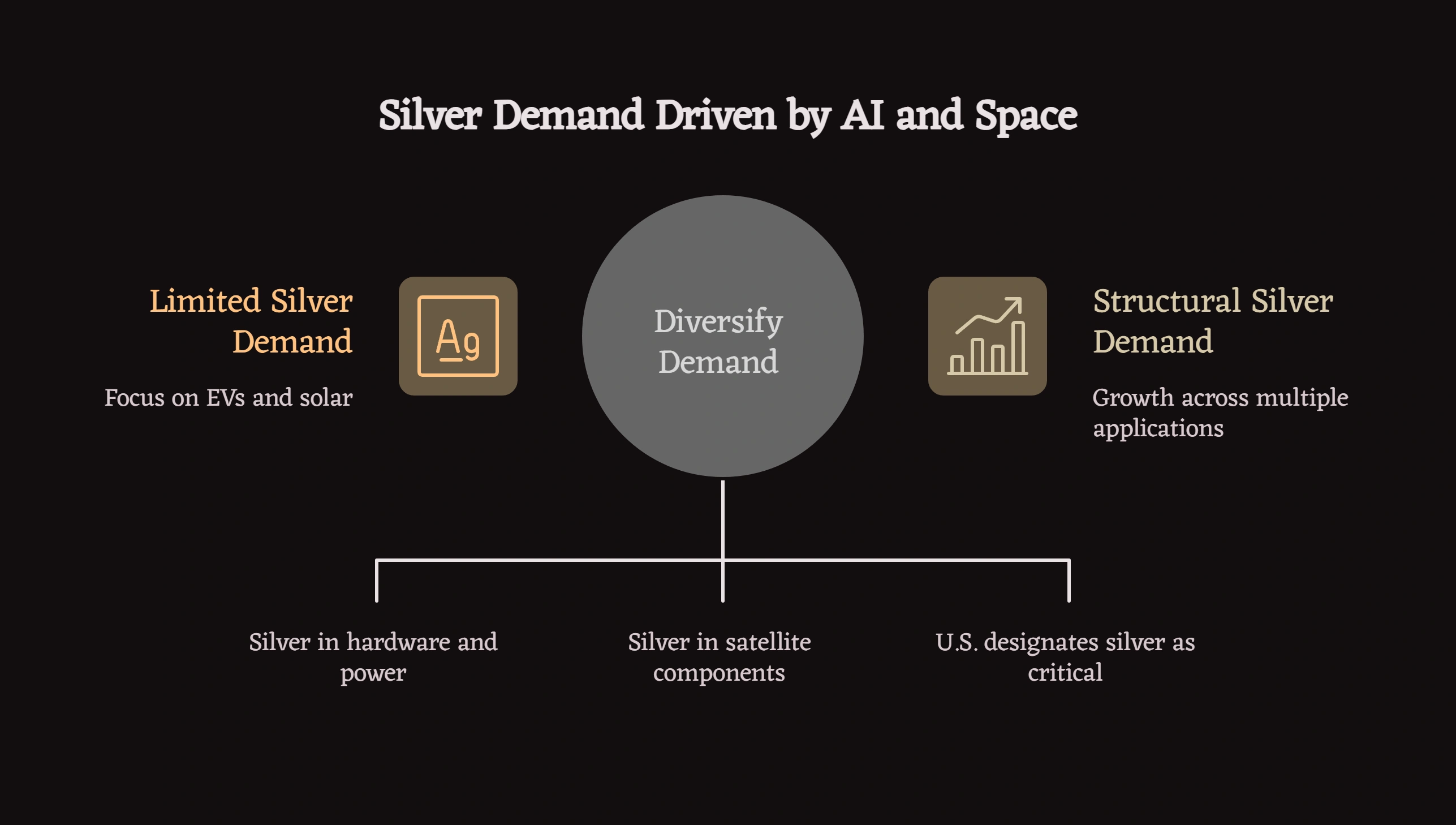

Why AI Data Centers and the Space Economy Are Adding a New Silver Demand Layer in 2026

The industrial demand argument for silver covered in gold IRA affiliate content typically stops at EVs and solar panels. Two demand vectors receiving substantially less coverage — but increasingly documented by institutional sources — are AI data center infrastructure and the commercial space economy.

The AI data center connection goes beyond solar power backup

The most commonly cited link between AI and silver is indirect: AI data centers consume massive amounts of electricity, requiring solar farm buildout to power them, which consumes silver. That connection is real. But the more direct — and less-discussed — link is the silver embedded in the data center hardware itself.

AI data centers are materials-intensive physical infrastructure. Silver appears in multiple layers of the hardware stack: high-current busbars that distribute power through server racks, silver-plated switchgear and relays in power distribution systems, advanced connectors handling 100+ Gbps data interconnects between GPU clusters, and thermal interface materials that manage heat dissipation in processors running at sustained extreme loads. Silver's 63 million siemens-per-meter electrical conductivity — the highest of any element — is not replicated by copper or aluminum at the tolerances AI hardware requires.

The architecture shift toward higher-voltage data centers compounds this demand. Nvidia-driven 800V high-voltage direct current designs, targeted for broad commercial deployment from 2027, use meaningfully more silver than conventional power architectures due to silver's superior thermal conductivity and oxidation resistance at high voltages. Goldman Sachs projects U.S. data center power demand to double by 2027 — a compressed timeline that is pulling silver-bearing components into servers, power distribution systems, and thermal management hardware at an accelerating rate..

The Silver Institute's Oxford Economics report "Silver, The Next Generation Metal" explicitly identifies AI and data centers alongside solar and EVs as the three primary drivers of industrial silver demand growth through 2030 — a significant institutional acknowledgment that the AI demand vector is structural, not speculative.

The U.S. government's 2025 Critical Minerals designation

In 2025, the U.S. government formally added silver to its Critical Minerals List. This policy decision reflects what defense and industrial engineers have understood for years: silver's conductivity, signal integrity, and corrosion resistance make it irreplaceable in high-reliability electronics applications. The U.S. is currently net-import-reliant for silver at approximately 64–80% of domestic consumption according to USGS data, and no longer maintains a national silver stockpile following decades of inventory disposal. The Critical Minerals designation signals federal recognition that silver supply security is a strategic concern — a context that matters for long-term demand and price support arguments.

The commercial space economy as a compounding factor

The space demand angle is smaller and harder to quantify than AI data centers or solar, but it is directionally additive. Each satellite contains multiple ounces of silver in electrical contacts, conductive pastes, thermal shielding, and waveguide components. Silver-zinc batteries power spacecraft and missile systems. Silver electroplating is standard in satellite interior components for its anti-galling properties in threaded assemblies exposed to the vibration and vacuum conditions of space.

SpaceX's Falcon 9 reusable rocket program has fundamentally changed launch economics — and launch frequency. The commercial space launch market grew from approximately $4.8 billion in 2020 to an estimated $10.8 billion in 2026, and is projected to reach $78 billion by 2035 according to market research from Spherical Insights. Each incremental satellite deployment in that growth curve adds to cumulative silver consumption in aerospace-grade components.

Space demand is best framed as a compounding factor alongside AI, solar, and EVs rather than a standalone investment thesis. The practical significance is that silver faces simultaneous demand growth across multiple non-substitutable applications — AI hardware, renewable energy, electrified transportation, and aerospace — while mine supply growth remains structurally constrained.

Where this argument has limits

Federal employees evaluating these demand vectors should distinguish between structural long-term consumption trends and near-term price catalysts. The AI data center buildout, satellite deployment rates, and EV adoption curves are multi-year trajectories. Silver's price in any given quarter will still respond to monetary policy, dollar strength, and investor sentiment in ways that can temporarily override the industrial fundamentals. The demand thesis is a long-duration structural argument — it does not predict silver's price in 2026 or any specific year.

What Is the Gold-to-Silver Ratio and Why Do Some Federal Employees Reference It?

The gold-to-silver ratio measures how many ounces of silver are required to purchase one ounce of gold. At a gold price of $3,100 and silver at $32, the ratio is approximately 97:1.

The ratio's historical context: over the past 50 years, the gold-to-silver ratio has averaged approximately 60:1. Periods where the ratio has exceeded 80:1 have historically been followed — over varying timeframes — by silver outperforming gold as the ratio mean-reverted toward historical norms. The ratio reached approximately 125:1 during the COVID-19 market disruption in March 2020 before contracting to approximately 63:1 by August 2020 as silver recovered sharply.

Federal employees who reference the gold-to-silver ratio are essentially making a relative value argument: if gold and silver both serve similar monetary hedging functions, the current ratio suggests silver offers more upside per dollar invested than gold at current prices — not because silver is cheap in absolute terms, but because it is historically cheap relative to gold.

Important caveats on ratio-based reasoning:

The gold-to-silver ratio can remain elevated for extended periods without correcting. The ratio exceeded 80:1 for most of 2018–2020 before the COVID-driven spike. An investor who repositioned from gold to silver in early 2018 based on ratio analysis waited over two years before the ratio moved meaningfully in silver's favor.

The ratio is a relative value observation, not a timing signal. Federal employees evaluating silver on ratio grounds should treat it as one factor among several, not as a predictive indicator of near-term price movement.

When Does Gold Make More Sense Than Silver for a Federal Employee?

A balanced analysis of this question requires honest acknowledgment of where gold remains the stronger choice.

Gold is less volatile. Gold's annual price standard deviation runs approximately 15%, compared to silver's 25–30%. For federal employees within 5–7 years of planned retirement, gold's lower volatility profile reduces sequence-of-returns risk — the risk that a significant drawdown in the years immediately before retirement permanently impairs retirement income capacity. Silver's higher volatility makes it a more appropriate choice for employees with longer accumulation horizons who can absorb potential drawdowns.

Gold's monetary demand is more predictable. Gold's primary use as monetary reserve and investment asset means its price behavior during financial crises and currency stress events is more historically consistent than silver's, which can sell off alongside industrial commodities during risk-off episodes. Federal employees seeking a crisis hedge above all other considerations may find gold's behavior more reliable for that specific purpose.

Gold's higher unit value simplifies some planning decisions. A $50,000 gold position holds fewer physical units — typically 15–16 one-ounce coins — which simplifies in-kind distribution at RMD time and may reduce storage costs proportionally given the lower physical volume.

Gold suits investors who find silver's industrial thesis speculative. Some federal employees are more comfortable with gold's centuries-long monetary heritage than with silver's emerging technology demand story. An investor who is not convinced that EV adoption or solar buildout will proceed as projected may find gold's monetary thesis more intuitive and verifiable.

How Do Noble Gold, Birch Gold Group, and Augusta Handle Silver vs Gold for TSP Rollovers?

All three primary precious metals IRA providers offer both silver and gold for TSP rollover clients. The practical differences in how they handle silver versus gold are primarily in product selection and dealer spread.

Noble Gold Investments offers American Silver Eagles, Canadian Silver Maple Leafs, and 100-oz silver bars alongside its gold product lineup. Noble Gold's experience with TSP-specific rollover procedures for federal and military clients applies equally to silver and gold accounts. Minimum investment is $2,000.

Birch Gold Group provides silver products including American Silver Eagles and bars through its Equity Trust custodian relationship. The $10,000 minimum makes it accessible for partial TSP allocations, and its silver product selection suits employees building initial positions. Silver coin spreads at Birch typically run in the 4–6% range.

Augusta Precious Metals deliberately limits its product offering to gold and silver only, positioning silver as the complement to gold in a two-metal diversification strategy. Augusta's $50,000 minimum and education-first onboarding model suits federal employees with larger TSP balances who want guided positioning across both metals.

For federal employees deciding between silver and gold with any of these providers, the practical recommendation is to request explicit written spread disclosures for both metals before committing. Silver coin spreads tend to run 1–2 percentage points higher than comparable gold coin spreads due to silver's higher physical volume per dollar and greater handling costs per ounce.

Who Should Consider Silver Over Gold for a TSP Rollover — and Who Should Not

Silver over gold may make more sense for federal employees who:

- Have TSP balances where $20,000–$75,000 allocations to precious metals are practical — silver's entry cost makes this range more meaningful than gold's

- Are 10 or more years from retirement and have sufficient time horizon to absorb silver's higher volatility

- Are specifically drawn to industrial demand diversification — exposure to energy transition, EV adoption, and technology manufacturing trends not available through TSP fund options

- View the current gold-to-silver ratio as evidence of relative undervaluation and want exposure to potential ratio mean-reversion over a multi-year horizon

- Want to build a precious metals position incrementally through annual IRA contributions — silver's lower price allows more consistent accumulation

Gold over silver may make more sense for federal employees who:

- Are within 5–7 years of retirement and prioritize lower volatility over potential upside

- Are allocating $100,000 or more to precious metals, where gold's higher unit value simplifies storage and distribution logistics

- Want a simpler monetary hedge without industrial demand exposure to global manufacturing cycles

- Are more comfortable with gold's established monetary role than with silver's industrial demand thesis

- Have experienced previous silver volatility cycles and prefer gold's historically more stable behavior during financial stress events

Federal employees ready to move forward with a silver IRA rollover can find a complete walkthrough of direct vs indirect transfer mechanics, IRS rules, and Noble Gold's TSP-specific process in our TSP to silver IRA rollover guide for federal employees.

Frequently Asked Questions

Is silver a safer investment than gold for federal employees?

No. Silver carries meaningfully higher price volatility than gold — approximately 25–30% annual standard deviation versus gold's 15%. Silver's lower per-ounce price makes it more accessible for smaller allocations, but accessibility should not be confused with lower risk. Federal employees near retirement in particular should factor silver's higher volatility into allocation sizing decisions.

Can a federal employee hold both silver and gold in the same self-directed IRA?

Yes. A single self-directed IRA can hold both IRS-approved silver and gold products simultaneously. Some federal employees allocate across both metals to balance silver's industrial demand characteristics with gold's more purely monetary hedge profile. The custodian and depository handle both metals under the same account structure.

How does silver's IRS purity requirement differ from gold?

Silver held in a self-directed IRA must meet 99.9% fineness. American Silver Eagles are exempt from this specific purity standard due to their government mint status and qualify regardless of fineness. Gold must meet 99.5% fineness, with American Gold Eagles similarly exempt. Both metals must be stored at an IRS-approved depository — home storage of IRA metals triggers immediate taxable distribution.

What happens to silver demand if EV adoption slows?

Silver's industrial demand encompasses multiple sectors — solar panels, semiconductors, 5G infrastructure, medical devices, and consumer electronics — in addition to EVs. A slowdown in EV adoption would reduce one demand component but would not eliminate silver's broader industrial consumption base. The Silver Institute projects that even under conservative EV adoption scenarios, total industrial silver demand continues growing through the late 2020s driven by solar and semiconductor growth.

How do silver's RMD requirements work compared to gold?

Self-directed silver and gold IRAs are subject to identical RMD rules — distributions begin at age 73, calculated based on December 31 fair market value divided by the IRS life expectancy factor. RMDs from any precious metals IRA are calculated and satisfied separately from TSP RMDs. Multiple precious metals IRAs can aggregate their RMDs and satisfy them from a single account. Silver's lower per-ounce value means RMD distributions may require liquidating a larger number of physical units than a comparable gold position, which is worth discussing with the custodian when planning distribution strategy.

This article provides educational information about silver and gold IRA options for federal employees considering TSP rollovers. It does not constitute financial, tax, or investment advice. Federal employees should consult a qualified tax professional or fiduciary financial advisor before making rollover or allocation decisions. IRS.gov and TSP.gov provide authoritative guidance on precious metals IRA requirements and TSP rollover mechanics.

References

[1] Silver Institute. "World Silver Survey 2024." SilverInstitute.org.

[2] Federal Retirement Thrift Investment Board. "TSP Fund Options and Expense Ratios." TSP.gov. 2024.

[3] Internal Revenue Service. "IRC Section 408(m): Treatment of Collectibles in IRAs." IRS.gov.

[4] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[5] World Gold Council. "Gold Demand Trends Full Year 2024." Gold.org.

[6] International Energy Agency. "Global EV Outlook 2024." IEA.org.

[7] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020–2024." CFTC.gov.

[8] U.S. Geological Survey. "Silver: Mineral Commodity Summaries 2024." USGS.gov.

[9] Internal Revenue Service. "Retirement Topics — Required Minimum Distributions." IRS.gov.

[10] Federal Retirement Thrift Investment Board. "In-Service Withdrawal Basics." TSP.gov.

[11] Internal Revenue Service. "IRS Notice 2024-80: 2025 Retirement Plan Contribution Limits." IRS.gov.

[12] BloombergNEF. "Electric Vehicle Outlook 2024." BloombergNEF.com.

[13] U.S. Geological Survey. "USGS Releases 2025 List of Critical Minerals." USGS.gov. 2025.

[14] Goldman Sachs. "U.S. Data Center Power Demand Projected to Double by 2027." Goldman Sachs Insights. May 2026. GoldmanSachs.com.