.svg)

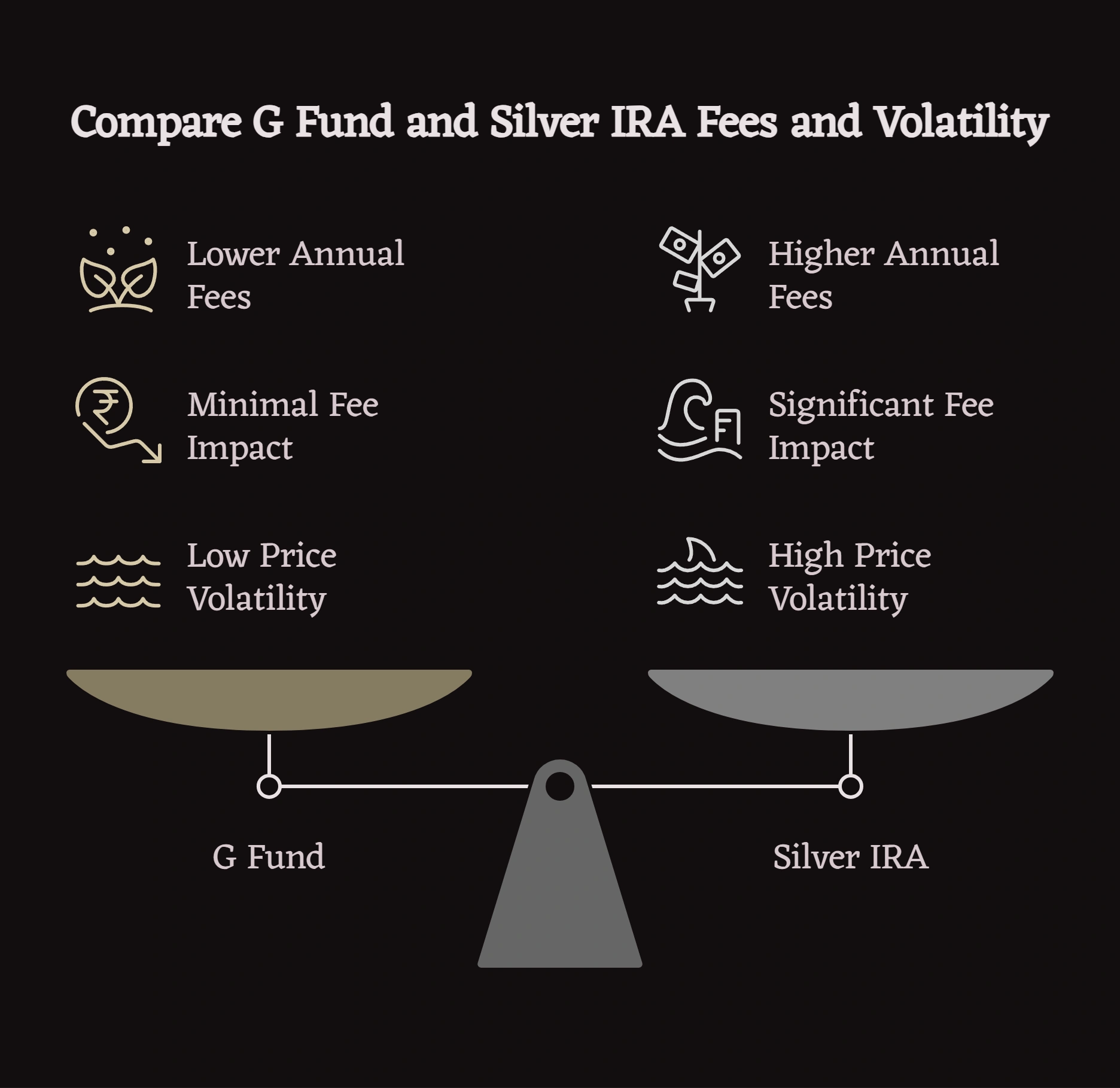

The TSP G Fund and silver IRA serve different retirement functions: the G Fund preserves nominal principal through government-backed securities at 0.042% annual cost, while a silver IRA introduces physical metal exposure with dual industrial and monetary demand characteristics at an estimated $525–$900 annual cost per $100,000. Silver differs from gold in one critical way relevant to federal employees nearing retirement — its industrial demand base creates a price floor independent of monetary sentiment, while its lower per-ounce entry cost makes partial diversification accessible at smaller rollover amounts. Neither instrument universally outperforms the other. The decision depends on whether purchasing power protection or principal certainty is the primary retirement objective.

Last updated: May 2026

At a Glance

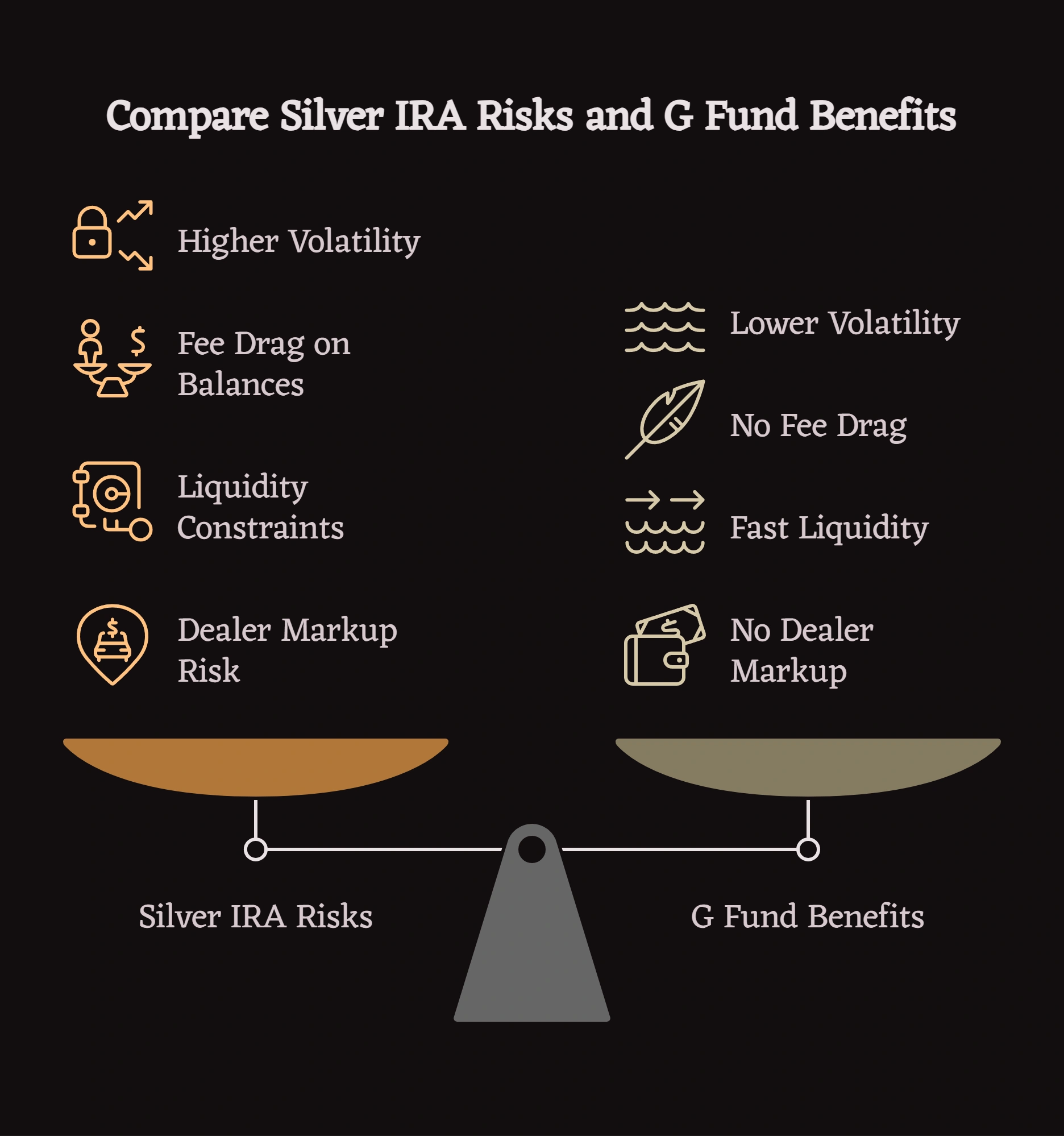

- The G Fund guarantees principal through government-backed securities — silver provides no principal guarantee and carries meaningful price volatility

- Silver's industrial demand from EVs, solar panels, and semiconductor manufacturing creates structural price support that gold's primarily monetary demand does not share

- Federal employees within 5 years of retirement face a specific liquidity trade-off: G Fund allows same-day interfund transfers; silver IRA liquidation takes 3–7 business days

- Silver's lower per-ounce cost (~$30–$35 in 2026) enables meaningful physical diversification at smaller allocation sizes than gold requires

Who This Comparison Is For

This article is written for federal employees within 10–15 years of retirement who already hold G Fund allocations and are evaluating whether a partial silver IRA position makes sense alongside — not instead of — their existing TSP structure. It is not an argument for wholesale TSP-to-silver conversion. It addresses a specific question: does silver add anything the G Fund cannot provide, and at what cost and risk?

How Does This Differ From the TSP G Fund vs Gold IRA Comparison?

Readers who have reviewed the TSP G Fund vs gold IRA comparison on this site will notice significant overlap in the structural analysis — both precious metals operate under identical self-directed IRA frameworks, identical IRS storage requirements, and similar fee structures. The meaningful differences are:

Silver's industrial demand accounts for over 50% of annual global consumption, compared to gold's roughly 10% industrial usage. This means silver's price responds to manufacturing output, technology adoption curves, and energy infrastructure buildout in ways gold does not.

Silver's lower per-ounce price (~$30–$35 vs. $3,000–$3,200 for gold in 2026) means federal employees with moderate TSP balances can establish a meaningful physical position without concentrating the allocation. A $25,000 partial rollover buys approximately 700–800 ounces of silver versus fewer than 9 ounces of gold.

Silver's volatility profile is meaningfully higher than gold's. Gold carries approximately 15% annual standard deviation. Silver's historical standard deviation runs 25–30% annually — approximately double. For federal employees nearing retirement, this distinction matters significantly when evaluating sequence-of-returns risk.

These three differences — industrial demand exposure, entry cost, and higher volatility — define why silver deserves a separate analysis from gold for this audience rather than a generic "precious metals" comparison.

How Does the G Fund Work — and What Does It Not Do?

The TSP G Fund invests exclusively in short-term U.S. Treasury securities issued specifically for the TSP. This structure provides principal guarantee — the G Fund cannot lose nominal value regardless of market conditions — combined with a long-term interest rate on short-term duration risk. No equivalent instrument exists in private markets.

G Fund yields tracked between 4.0–4.5% during 2024, reflecting the higher rate environment. Current 2026 projections sit in the 3.5–4.2% range depending on Federal Reserve policy trajectory. The 0.042% expense ratio translates to $42 annually per $100,000 — among the lowest costs of any retirement vehicle available to American workers.

The G Fund's primary structural limitation is purchasing power erosion during sustained inflation. If CPI runs at 4.5% and the G Fund returns 3.8%, real retirement wealth declines by approximately 0.7% annually despite nominal principal preservation. Over a 20-year retirement horizon, that erosion compounds meaningfully.

The G Fund provides no industrial exposure, no non-correlated diversification beyond Treasuries, and no response to the specific demand dynamics — energy transition, semiconductor manufacturing, electrification — that some investors cite as structural tailwinds for silver pricing.

How Does a Silver IRA Work for Federal Employees?

A silver IRA is a self-directed IRA holding IRS-approved physical silver bullion through an IRS-approved custodian, with metals stored at an IRS-approved depository. The structure is identical to a gold IRA in every regulatory sense — same purity requirements (99.9% fineness for silver, with American Silver Eagles exempt), same storage rules, same prohibited transaction framework, and same RMD requirements beginning at age 73.

Federal employees fund silver IRAs primarily through TSP rollovers executed as direct trustee-to-trustee transfers, avoiding mandatory 20% withholding. Partial rollovers are common — many federal employees move 5–10% of TSP assets while preserving the majority in the TSP's low-cost fund structure.

The custodian holds legal title and issues annual IRS Form 5498. The depository holds the physical silver in segregated, insured storage. The account holder cannot take personal possession of the metals while they remain inside the IRA structure without triggering a taxable distribution.

G Fund vs Silver IRA: Full Comparison

How Has Silver Performed During Historical Inflationary Periods?

Silver's inflation hedge record is more mixed than gold's, which is a distinction federal employees near retirement should evaluate carefully.

During the sustained inflation of the 1970s, silver rose from approximately $1.50 per ounce in 1971 to a peak of $49.45 in January 1980 — a gain of approximately 3,200%. However, this period included significant speculative activity from the Hunt Brothers' attempted market cornering, making it an imperfect benchmark for structural silver behavior.

During the 2020–2022 inflation cycle, silver rose from approximately $14 per ounce in March 2020 to approximately $29 per ounce by year-end 2020 — a 107% gain. By mid-2022, as rate hike expectations accelerated, silver had retreated to approximately $18 per ounce despite persistent consumer price inflation. This behavior illustrates a critical characteristic: silver can underperform as an inflation hedge when rising interest rates strengthen the dollar and reduce monetary demand, even if industrial demand remains strong.

The G Fund, by contrast, actually benefits from rising rate environments — G Fund yields increase as Treasury rates rise, providing a natural tailwind during exactly the conditions that can pressure silver prices.

Pattern for federal employees to understand: Silver tends to outperform during sustained, prolonged inflationary periods with accommodative monetary policy. It tends to underperform during inflationary periods where the Federal Reserve responds aggressively with rate increases — the exact scenario that characterized 2022. The G Fund performs more predictably across interest rate environments.

How Do Fees Compound Over Time for Each Option?

The annual fee differential between the G Fund and a silver IRA is significant and compounds over long holding periods. The G Fund's $42 annual cost per $100,000 versus a silver IRA's estimated $525–$900 annual cost represents a $483–$858 annual gap on the same balance.

30-year fee impact on $100,000 (no additional contributions, no account growth):

- G Fund cumulative fees: approximately $1,260

- Silver IRA cumulative fees (midpoint estimate): approximately $21,250

- Fee differential: approximately $19,990

With account growth, this differential widens because silver IRA storage fees scale partially with account value. For silver to justify this fee premium over the G Fund, its price appreciation must exceed G Fund returns by approximately 0.50–0.90% annually just to break even on costs alone — before accounting for silver's considerably higher price volatility.

This breakeven threshold is meaningful but not insurmountable. During the 2000–2011 period, silver outperformed Treasury returns by substantial margins. The question for federal employees nearing retirement is whether their remaining accumulation horizon is long enough to absorb silver's volatility and recover from potential drawdowns while still realizing the return premium needed to overcome the fee differential.

What Are the Real Risks of Each Option?

G Fund Risks

Purchasing power erosion: The G Fund's primary vulnerability is sustained inflation exceeding its yield. An employee earning 3.8% in the G Fund while experiencing 5% CPI inflation loses real purchasing power at approximately 1.2% annually. Over a 20-year retirement, this compounding erosion can meaningfully reduce real retirement income.

Opportunity cost near retirement: Federal employees who maintain heavy G Fund allocations throughout their career may sacrifice meaningful long-term growth available through equity exposure (C Fund, S Fund, I Fund) during accumulation years. The G Fund is most appropriate as a capital preservation tool in the 3–5 years immediately preceding and following retirement, not as a decades-long primary accumulation vehicle.

Rate environment dependency: G Fund yields follow Treasury rates. In low-rate environments (2010–2021), G Fund yields averaged 1.5–2.5% — significantly below historical inflation benchmarks — meaning real purchasing power declined for G Fund-heavy allocations throughout that period.

Silver IRA Risks

Higher volatility than gold: Silver's 25–30% annual standard deviation is approximately double gold's. Federal employees within 5 years of retirement face meaningful sequence-of-returns risk from a sharp silver drawdown in the years immediately before planned retirement. The 2011–2015 silver bear market saw prices decline approximately 72% from peak to trough — a drawdown that would represent catastrophic loss for any investor with a concentrated silver position approaching retirement.

Fee drag on smaller balances: A $25,000 silver IRA position incurs approximately $300–$450 in annual fees — 1.2–1.8% annually. At this balance, the fee structure represents a significant return headwind before any price movement occurs.

Liquidity constraints at distribution: Silver IRA liquidations require custodian processing, depository release, and settlement — typically 3–7 business days. Federal employees who experience unexpected cash needs in retirement cannot access silver IRA funds with the same speed as TSP interfund transfers or G Fund distributions.

Dealer markup risk: The bid-ask spread on silver purchases ranges from 3–8% for reputable dealers. On a $50,000 allocation, a 5% spread means the account starts $2,500 below spot value before any price movement. Federal employees who do not request written spread disclosures before purchasing can face undisclosed entry costs that extend the breakeven period considerably.

Who Should Consider Adding Silver Alongside G Fund Holdings?

This combination may merit evaluation for federal employees who:

- Have G Fund allocations representing more than 40% of total retirement assets and are specifically concerned about purchasing power erosion over a 15–25 year retirement horizon

- Are at least 10 years from planned retirement, providing sufficient time horizon to absorb silver's volatility and recover from potential drawdowns

- Have TSP balances above $150,000, where silver IRA fee structures represent a manageable percentage of total retirement assets

- Want non-correlated industrial commodity exposure that responds to technology and energy infrastructure trends — characteristics the G Fund and TSP equity funds do not provide

- Are comfortable holding a 5–10% allocation in a volatile asset with 3–7 day liquidation timelines

This combination warrants additional caution for federal employees who:

- Are within 5 years of retirement, where silver's volatility creates meaningful sequence-of-returns risk

- Have G Fund allocations primarily for capital preservation purposes that would be undermined by silver's price swings

- Have total TSP balances below $75,000, where silver IRA fees create disproportionate annual cost drag

- Need near-term liquidity access that silver's 3–7 day settlement timeline cannot provide

- Have not yet consulted a tax professional on the Roth vs. traditional rollover distinction for their specific situation

Federal employees ready to act on a partial rollover can find the complete mechanics in our TSP to silver IRA rollover guide for federal employees.

Frequently Asked Questions

Does silver provide better inflation protection than the G Fund?

Silver has historically outperformed nominal Treasury returns during extended inflationary periods with accommodative monetary policy. However, during inflationary episodes where the Federal Reserve responds aggressively with rate increases — as in 2022 — silver prices can decline even as consumer prices rise. The G Fund's yield responds positively to rising rates, making it more predictable as a near-term inflation hedge than silver in rising rate environments.

Can a federal employee hold both G Fund and a silver IRA simultaneously?

Yes. Maintaining G Fund allocations within the TSP and holding a separate self-directed silver IRA are not mutually exclusive. Many federal employees maintain 90–95% of retirement assets in the TSP's low-cost structure while allocating a 5–10% satellite position to a silver IRA through a partial rollover. This approach preserves the G Fund's principal guarantee and cost efficiency for the majority of retirement savings while adding silver's industrial and monetary diversification characteristics at the margin.

How does silver's volatility compare to the TSP equity funds?

Silver's 25–30% annual standard deviation is higher than the TSP C Fund's approximately 17% historical standard deviation and meaningfully higher than the G Fund's 0%. For federal employees near retirement who are typically shifting from growth-oriented C and S Fund allocations toward capital preservation, adding silver introduces a volatility profile that runs counter to conventional pre-retirement asset allocation strategy. The case for silver near retirement rests on its non-correlation with equities rather than its absolute return potential.

What silver allocation percentage makes sense alongside G Fund holdings?

Most financial planning frameworks that include precious metals position them at 5–10% of total retirement assets. For federal employees with G Fund-heavy TSP allocations, a silver IRA representing 5–8% of total retirement assets would provide meaningful exposure to industrial and monetary demand dynamics without introducing volatility levels that threaten retirement income security. Allocations above 15% are generally considered outside conventional diversification parameters for retirement-stage investors.

How are RMDs handled differently for the G Fund and a silver IRA?

G Fund RMDs are calculated as part of the TSP's overall RMD calculation and can be satisfied through the TSP's automated distribution options. Silver IRA RMDs are calculated separately based on the silver IRA's December 31 fair market value and cannot be aggregated with TSP distributions — they must be satisfied independently, either through silver liquidation or in-kind metal distribution. Federal employees managing both accounts in retirement need to track and satisfy two separate RMD obligations beginning at age 73.

This article provides educational information comparing the TSP G Fund and self-directed silver IRA structures for federal retirement planning purposes. It does not constitute financial, tax, or investment advice. Federal employees should consult a qualified tax professional or fiduciary financial advisor familiar with government retirement plans before making any allocation or rollover decisions. TSP.gov and IRS.gov provide authoritative guidance on TSP fund mechanics and precious metals IRA requirements.

References

[1] Federal Retirement Thrift Investment Board. "G Fund: Government Securities Investment Fund." TSP.gov.

[2] Federal Retirement Thrift Investment Board. "TSP Expense Ratios and Administrative Costs." TSP.gov. 2024.

[3] Internal Revenue Service. "IRC Section 408(m): Treatment of Collectibles in IRAs." IRS.gov.

[4] Internal Revenue Service. "Publication 590-B: Distributions from Individual Retirement Arrangements." 2025 Edition. IRS.gov.

[5] Silver Institute. "World Silver Survey 2024." SilverInstitute.org.

[6] World Gold Council. "Gold as a Strategic Asset." Gold.org.

[7] Commodity Futures Trading Commission. "Precious Metals Fraud Enforcement Actions 2020–2024." CFTC.gov.

[8] Internal Revenue Service. "Retirement Topics — Required Minimum Distributions (RMDs)." IRS.gov.

[9] Employee Benefit Research Institute. "Retirement Savings Adequacy and Asset Allocation." EBRI.org.

[10] Federal Retirement Thrift Investment Board. "TSP Fund Performance History." TSP.gov.

[11] U.S. Bureau of Labor Statistics. "Consumer Price Index Historical Data." BLS.gov.

[12] Internal Revenue Service. "IRS Notice 2024-80: 2025 Retirement Plan Contribution Limits." IRS.gov.